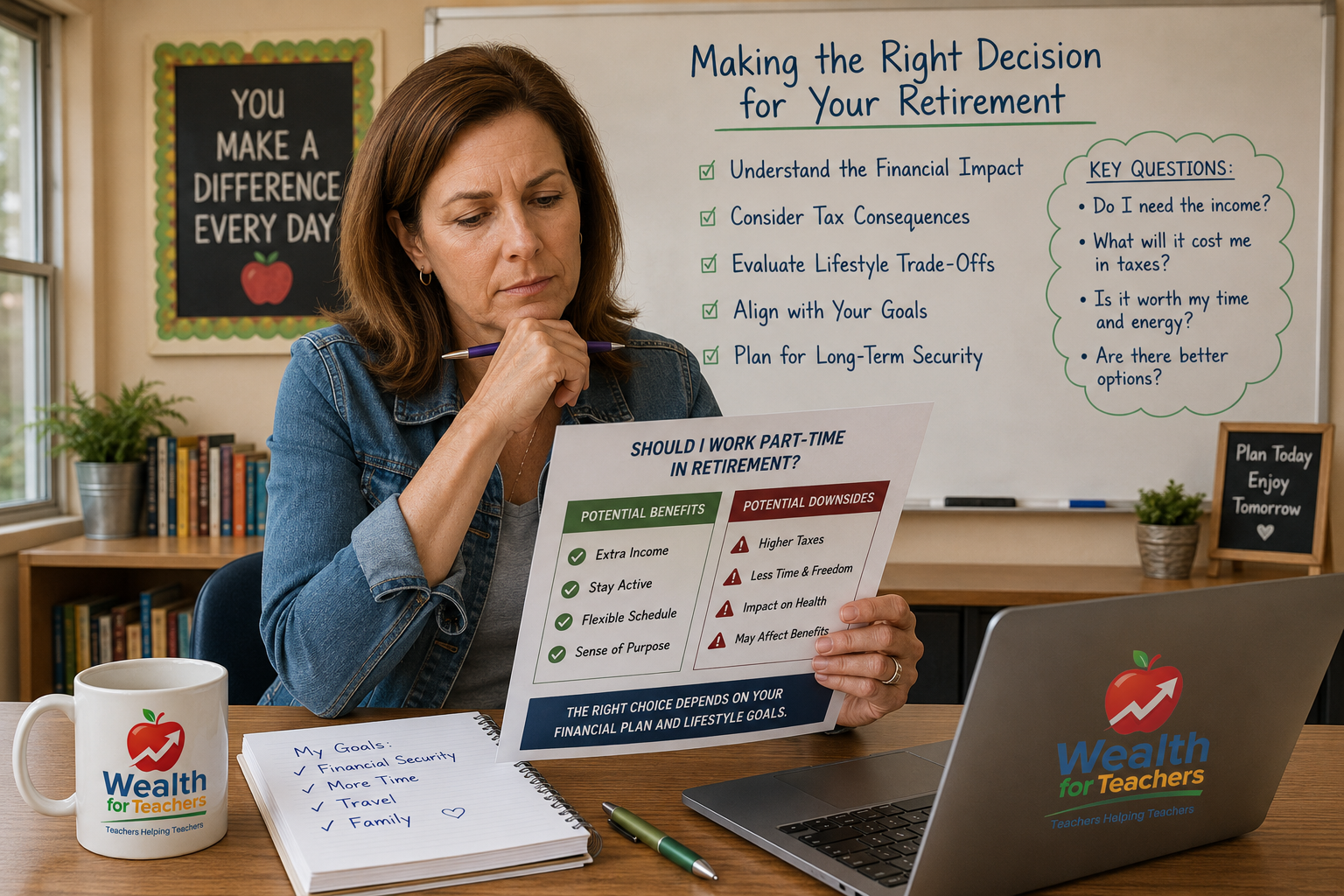

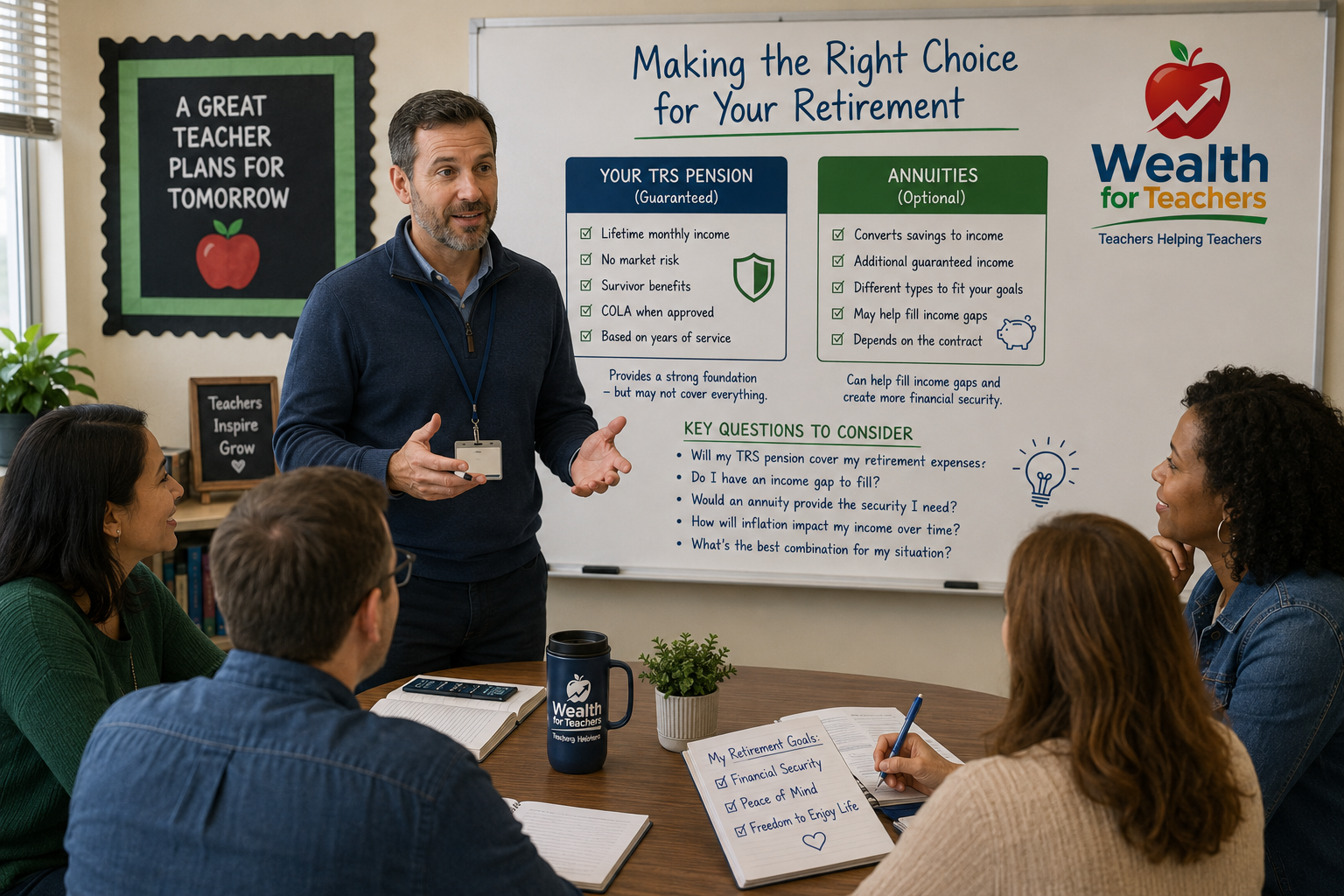

Should Teachers Use Annuities or Guaranteed Income Strategies?

Guaranteed income can reduce risk—but it’s not always right.

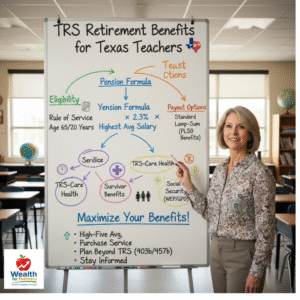

TRS Retirement Benefits for Texas Teachers: Your Complete Guide As a Texas teacher, understanding your TRS retirement benefits is crucial for securing your financial future. The Teacher Retirement System of Texas provides comprehensive retirement benefits that can serve as the foundation of your retirement income, but navigating the system’s complexities requires careful planning and knowledge. […]

As a Texas teacher, understanding your TRS retirement benefits is crucial for securing your financial future. The Teacher Retirement System of Texas provides comprehensive retirement benefits that can serve as the foundation of your retirement income, but navigating the system’s complexities requires careful planning and knowledge.

Your TRS benefits aren’t just about the monthly pension check you’ll receive after retirement. The system offers multiple components including health insurance, survivor benefits, and various payout options that can significantly impact your retirement lifestyle. Whether you’re a new teacher just starting your career or a veteran educator nearing retirement, understanding these benefits will help you make informed decisions about your financial future.

TRS retirement guide for Texas teachers

The Teacher Retirement System of Texas operates as a defined benefit pension plan, meaning your retirement benefits are predetermined based on a specific formula rather than dependent on investment performance. This provides predictable income in retirement, which is one of the key advantages of teaching in Texas.

Get Your Free TRS Calculator

TRS covers most Texas public school educators, including teachers, administrators, librarians, counselors, and support staff. The system manages retirement benefits for over 1.6 million current and former Texas educators, making it one of the largest teacher retirement systems in the nation.

Your TRS benefits are funded through three sources:

Unlike Social Security, TRS benefits are not portable between states. However, Texas has reciprocal agreements with some other teacher retirement systems that may allow you to combine service credit if you’ve taught in multiple states.

Your monthly TRS pension is calculated using a straightforward formula that considers three main factors: years of service credit, your highest average salary, and a multiplier based on your years of service.

The basic TRS pension formula is:

Years of Service Credit × Multiplier (2.3)x 5 or 3 Highest Average (Depending on your Tier) = Annual Pension

The multiplier is based on the State rate of: 2.3%

This means a teacher with 30 years of service and an average high-five salary of $60,000 would receive an annual pension of $41,400 (30 × 2.3% x $60,000 ).

TRS uses your five highest or 3 highest annual salaries (depending on your tier) to calculate your average. These don’t have to be consecutive years, and the system automatically selects the five years that result in the highest average. This includes your base salary plus any additional compensation like stipends, but excludes one-time payments or bonuses.

TRS offers several paths to retirement eligibility, each with different age and service requirements. Understanding these options helps you plan when you can retire with full benefits.

The most popular retirement option is the Rule of 80, where your age plus years of service credit must equal at least 80. You must also be at least 55 years old and have a minimum of five years of service credit. This allows for full retirement benefits without reduction.

You can retire at age 65 with just five years of service credit and receive full benefits. This option works well for teachers who started their careers later in life or took breaks from education.

Teachers can retire at age 60 with 20 years of service credit. This option provides full benefits and is often used by teachers who started their careers in their early twenties.

TRS also offers early retirement with reduced benefits. You can retire with 20 years of service credit regardless of age, but your benefits will be actuarially reduced. The reduction is permanent and typically ranges from 6% to 30% depending on how early you retire.

For detailed information about planning your retirement timeline, consider exploring comprehensive retirement planning strategies that can help you optimize your benefits.

TRS-Care provides health insurance coverage for eligible TRS retirees and their dependents. This benefit is separate from your pension and requires separate eligibility and premium payments.

To be eligible for TRS-Care, you must:

TRS-Care offers several coverage levels, from basic medical coverage to comprehensive plans that include prescription drugs. Premium costs vary based on your years of service credit, with longer-serving educators receiving lower premiums.

The health benefits landscape can be complex, and many teachers benefit from understanding TRS-Care health insurance options well before retirement to plan accordingly.

TRS provides survivor benefits to protect your beneficiaries if you pass away before or after retirement. These benefits can provide crucial financial security for your family.

If you die before retirement with at least one year of service credit, your beneficiaries may be eligible for:

When you retire, you can choose from several survivor benefit options that will continue payments to your beneficiary after your death. These options typically reduce your monthly pension but provide ongoing income security for your spouse or other beneficiaries.

It’s crucial to keep your beneficiary designations current with TRS. You can name primary and contingent beneficiaries, and you should review these designations regularly, especially after major life events like marriage, divorce, or the birth of children.

When you’re ready to retire, TRS offers several payout options for your benefits. The choice you make is permanent, so it’s important to understand each option thoroughly.

The standard annuity provides the highest monthly payment but stops when you die. This option works best if you don’t have dependents who need ongoing income or if you have other assets to leave as inheritance.

PLSO allows you to take a portion of your retirement benefit as a lump sum while receiving reduced monthly payments for life. This option can be useful for paying off debt, making large purchases, or investing for additional retirement income.

Several options provide ongoing benefits to your survivors:

Each survivor benefit option reduces your monthly payment while you’re alive but provides security for your beneficiaries.

Understanding the intricacies of TRS pension calculations can help you make informed decisions about which payout option best serves your needs.

Most Texas teachers don’t pay into Social Security through their teaching positions, which affects their Social Security benefits if they have other work history. The Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) can significantly reduce Social Security benefits for TRS retirees.

WEP affects your own Social Security benefits if you receive a pension from work where you didn’t pay Social Security taxes. It can reduce your Social Security benefit by up to $587 per month in 2024, though the reduction depends on your years of substantial Social Security earnings.

GPO affects spousal and survivor Social Security benefits. It reduces these benefits by two-thirds of your TRS pension amount. For many teachers, this can eliminate spousal Social Security benefits entirely.

Planning for these reductions is crucial for teachers who expect to receive both TRS and Social Security benefits. The Social Security Administration provides detailed information about how these provisions work.

Rather than simply accepting your TRS benefits as they come, you can take proactive steps to maximize your retirement security.

Since your pension is based on your five highest salaries, strategic career moves in your final years can significantly impact your retirement income. Consider pursuing:

You may be able to purchase additional service credit for:

Purchasing service credit can help you reach retirement eligibility sooner and increase your pension amount.

While TRS provides a solid foundation, it may not be sufficient for the retirement lifestyle you desire. Consider supplementing your TRS benefits with:

TRS benefits and rules can change due to legislative action or board decisions. Stay informed by:

For comprehensive guidance on building wealth beyond your TRS benefits, explore 403(b) vs 457(b) options for teachers to understand your supplemental retirement savings opportunities.

Don’t leave your retirement to chance. Get personalized guidance on optimizing your TRS benefits and building a comprehensive retirement strategy.

Yes, but your Social Security benefits may be reduced by the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO). If you worked in jobs where you paid Social Security taxes, you can still receive those benefits, though they’ll likely be reduced. The amount of reduction depends on your years of substantial Social Security earnings and the size of your TRS pension.

Your TRS service credit and benefits remain yours, but they’re not portable to other states’ retirement systems. You can leave your money in TRS and collect benefits when you’re eligible, or you may be able to withdraw your contributions. Texas has reciprocal agreements with some states that might allow you to combine service credit, but this varies by state.

If you return to work for a TRS-covered employer after retirement, your pension payments will stop, and you’ll begin earning service credit again. However, there are specific rules about when you can return to work and how it affects your benefits. Generally, you must wait until the September following your retirement before returning to TRS-covered employment.

No, your survivor benefit selection is permanent and cannot be changed after retirement begins. This is why it’s crucial to carefully consider your options before retiring. However, if your beneficiary dies before you do, your monthly payment may be increased to the standard annuity amount.

Years of service refers to the actual time you’ve worked in TRS-covered positions, while years of service credit includes purchased credit for things like military service, out-of-state teaching, or other qualifying periods. Service credit is what’s used to calculate your benefits and determine retirement eligibility.

TRS cost-of-living adjustments (COLAs) are not automatic and must be approved by the Texas Legislature. Historically, COLAs have been provided periodically, but they’re not guaranteed. The amount and frequency depend on the system’s funding status and legislative priorities. This is one reason why supplemental retirement savings beyond TRS are important.

TRS is required by the Texas Constitution to pay benefits, and the state has ultimate responsibility for the system. While TRS faces funding challenges like many pension systems, benefits are legally protected. However, future benefit improvements may be limited, and contribution rates might increase to ensure the system’s long-term stability.

The PLSO can be beneficial in certain situations, such as paying off high-interest debt, funding major expenses, or investing for additional retirement income. However, it permanently reduces your monthly pension, so you need to carefully consider whether the lump sum will provide greater long-term value than the reduced monthly payments. Consider consulting with a financial advisor who understands TRS benefits before making this decision.

About the Author: LG Canales spent 16 years as a Texas public school teacher before transitioning to financial services. He specializes in helping educators maximize their TRS benefits and build comprehensive retirement strategies. As founder of Outside The Box Financial Group and the Wealth for Teachers division, LG combines his teaching experience with financial expertise to serve the unique needs of Texas educators.