What Is a Safe Withdrawal Rate for Teachers in Retirement?

Withdrawal strategy determines how long your money lasts. Learn the right approach.

TRS Pension Mistakes That Could Cost Texas Teachers Thousands Teaching is already challenging enough without having to worry about costly retirement mistakes. Unfortunately, many Texas educators make critical errors with their Teacher Retirement System (TRS) pension that can cost them thousands of dollars over their lifetime. The good news? Most of these mistakes are completely […]

Teaching is already challenging enough without having to worry about costly retirement mistakes. Unfortunately, many Texas educators make critical errors with their Teacher Retirement System (TRS) pension that can cost them thousands of dollars over their lifetime.

The good news? Most of these mistakes are completely preventable once you understand what to watch for. This guide walks you through the most common TRS pension pitfalls and shows you exactly how to avoid them.

Texas Teacher Retirement Guide

The Rule of 80 is perhaps the most important concept in TRS planning, yet many teachers don’t fully grasp how it works. This rule allows you to retire without penalty when your age plus years of service credit equal 80.

Get Your Free Guide TRS Calculations

Here’s where teachers commonly go wrong:

For example, a teacher who starts at age 22 could potentially retire at 51 with 29 years of service (22 + 29 = 51). However, if they wait until 55 with only 25 years of service, they’ll face a penalty reduction in their monthly benefit.

Retiring before meeting the Rule of 80 can reduce your monthly pension by up to 6% per year. For a teacher with a projected monthly benefit of $3,000, retiring three years early could cost them $540 per month for life – that’s $6,480 annually or over $129,600 over a 20-year retirement.

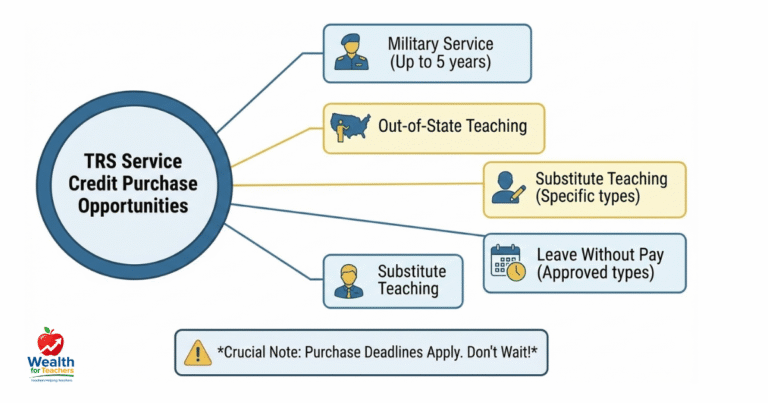

TRS offers several ways to earn or purchase additional service credit, but many teachers miss these opportunities entirely. This mistake can delay your retirement or reduce your final benefits significantly.

The window for purchasing some types of service credit has deadlines. For military credit, you typically have until age 65 or retirement, whichever comes first. Missing these deadlines means losing the opportunity forever.

Sarah taught in California for three years before moving to Texas. She never investigated purchasing that out-of-state credit. When she retires after 27 years in Texas, she’ll receive benefits based on 27 years instead of the potential 30 years. Those three missing years could cost her approximately $300-400 per month in retirement benefits.

Your TRS beneficiary designations determine who receives your retirement benefits if you pass away before or after retirement. Many teachers make critical errors in this area that can leave their families financially vulnerable.

Texas law requires specific procedures for changing beneficiaries after divorce. If you don’t follow these procedures correctly, your ex-spouse may still be entitled to your TRS benefits even if you’ve remarried.

Life changes constantly, and your beneficiary designations should reflect your current wishes. Review and update your beneficiaries:

Financial emergencies can tempt teachers to withdraw from their TRS accounts early, but this decision often proves costly in the long run. Early withdrawals not only reduce your retirement security but also come with immediate penalties and tax consequences.

TRS offers several withdrawal options, each with different implications:

The most costly mistake is taking a refund of contributions when leaving education temporarily. Teachers who return to TRS-covered employment must repay the refund with interest to restore their service credit.

Consider Maria, who took a $15,000 refund after five years of teaching. When she returns to education 10 years later, she must repay approximately $25,000 to restore those five years of service credit. Additionally, she lost out on potential investment growth on the state’s contributions during her absence.

Healthcare costs represent one of the largest expenses in retirement, yet many Texas teachers fail to plan adequately for these costs. TRS-Care, the retiree health insurance program, has specific eligibility requirements and limitations that catch many teachers off guard.

To be eligible for TRS-Care, you must:

Teachers who retire before meeting these requirements face a coverage gap that can be expensive to bridge with private insurance.

Even with TRS-Care coverage, retirees face significant out-of-pocket costs. The program requires monthly premiums, and coverage levels vary based on your years of service and retirement timing.

Smart healthcare planning includes:

Most Texas teachers don’t pay into Social Security during their teaching careers, but many have Social Security credits from other employment. Failing to coordinate these benefits properly can cost you money or create unexpected tax situations.

If you receive both a TRS pension and Social Security benefits, the Windfall Elimination Provision may reduce your Social Security benefits. This federal rule affects teachers who:

The reduction can be substantial – up to $587 per month in 2024 – depending on your years of substantial earnings under Social Security.

The GPO affects spousal and survivor Social Security benefits. If you receive a TRS pension, your spousal Social Security benefits may be reduced by two-thirds of your TRS pension amount. This can completely eliminate spousal benefits for many teachers.

Understanding these rules helps you make better decisions about how the Texas Teacher Retirement System really works and how to optimize your overall retirement income.

Avoiding these costly TRS pension mistakes requires proactive planning and regular attention to your retirement benefits. Here’s your action plan:

Start planning early and revisit your strategy regularly:

Don’t navigate TRS planning alone. Build a team that includes:

TRS rules and benefits can change. Stay current by:

Keep detailed records of:

While TRS provides a solid foundation, most teachers need additional retirement savings. Consider:

The best time to start optimizing your TRS benefits was when you first started teaching. The second-best time is right now. Even small improvements in your retirement strategy can compound into significant benefits over time.

Don’t let these common mistakes derail your retirement security. With proper planning and attention to detail, you can maximize your TRS benefits and build the retirement you deserve after a career dedicated to educating Texas students.

Ready to take control of your retirement planning? Our comprehensive retirement planning resources can help you avoid these costly mistakes and build a secure financial future.

Visit the official Retirement Planning Guide for the most current information about your benefits and planning options.

Some mistakes can be corrected, but others have permanent consequences. Service credit purchases often have deadlines, but you may still be able to buy military credit or out-of-state service. Beneficiary designations can usually be updated at any time. Contact TRS directly to discuss your specific situation and available options.

You can restore your service credit by repaying the refund amount plus interest. The interest rate varies based on when you took the refund. You typically have until retirement or age 65 to make this repayment. The longer you wait, the more expensive it becomes due to compound interest.

TRS pensions are not reduced by Social Security benefits. However, if you’re eligible for Social Security from other employment, your Social Security benefits may be reduced by the Windfall Elimination Provision (WEP). Check your Social Security statement and consult with a financial advisor familiar with both systems.

Purchasing service credit can be valuable if it helps you reach the Rule of 80 sooner or increases your years of service for benefit calculations. The cost varies by type of credit and your current age. Generally, if you plan to work long enough for the credit to count toward your retirement formula, it’s often worthwhile.

The biggest mistake is not understanding the eligibility requirements and assuming TRS-Care will be available regardless of when you retire. If you retire before meeting the Rule of 80 and you’re under 65, you won’t be eligible for TRS-Care. This can leave you without affordable health insurance options during a critical period.

The partial lump sum option reduces your monthly pension payments in exchange for a lump sum at retirement. Whether this makes sense depends on your financial situation, life expectancy, investment skills, and other income sources. Many financial experts recommend the monthly pension for its guaranteed income, but individual circumstances vary.

Review your TRS statement annually and reassess your overall retirement strategy every 3-5 years or after major life events. This includes marriages, divorces, births, deaths in the family, career changes, or significant changes in TRS rules or benefits. Regular reviews help ensure your strategy stays aligned with your goals and circumstances.

Don’t panic – many issues can still be addressed even close to retirement. Contact TRS immediately to understand your options. You may be able to purchase service credit, update beneficiaries, or adjust your retirement timing. Consider postponing retirement briefly if it allows you to correct a costly mistake or qualify for better benefits.

Don’t let costly mistakes derail your retirement security. Get personalized guidance to maximize your Teacher Retirement System benefits and build the retirement you deserve.