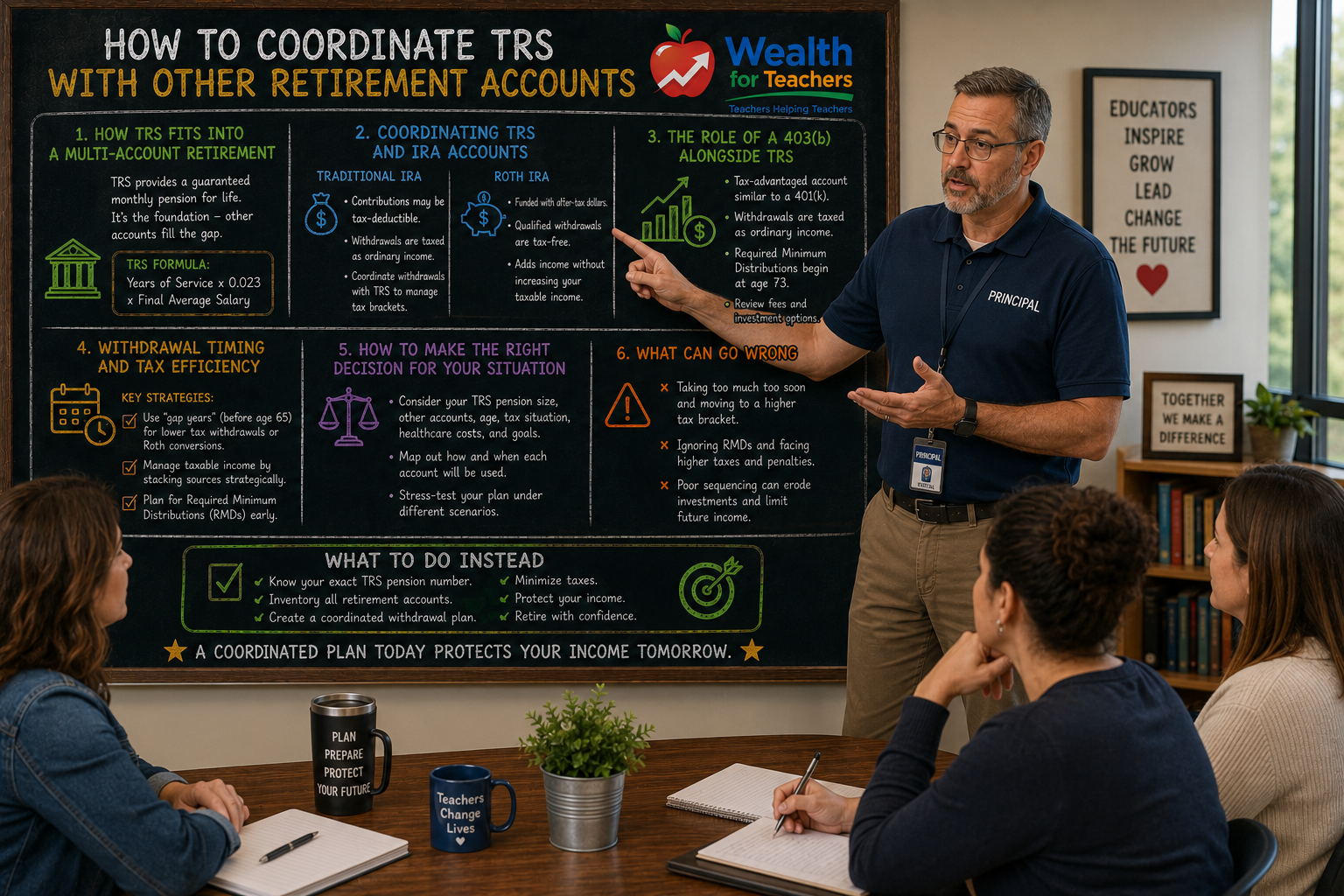

How to Coordinate TRS With IRAs, 403(b)s, and Other Accounts

TRS is only one piece of the puzzle. Learn how to align it with your other accounts.

WEP GPO Texas Teachers: How These Federal Rules Impact Your TRS Benefits If you’re a Texas teacher who has worked in other jobs covered by Social Security, you need to understand how the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) could affect your retirement income. These federal rules can significantly reduce your Social […]

If you’re a Texas teacher who has worked in other jobs covered by Social Security, you need to understand how the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) could affect your retirement income. These federal rules can significantly reduce your Social Security benefits, creating unexpected gaps in your retirement planning.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

The WEP can reduce your own Social Security benefits if you receive a pension from TRS (Teacher Retirement System of Texas), while the GPO can eliminate spousal or survivor Social Security benefits. For Texas educators who’ve had diverse career paths, these provisions often come as an unwelcome surprise during retirement planning.

The Windfall Elimination Provision and Government Pension Offset are federal laws designed to prevent what Congress viewed as “double-dipping” – receiving full Social Security benefits alongside pensions from jobs that didn’t pay into Social Security.

Use the TRS calculator to estimate your pension and identify potential income gaps.

Texas teachers fall under these rules because TRS is a separate retirement system. Unlike private sector employees who pay Social Security taxes on all their earnings, Texas teachers contribute to TRS instead of Social Security during their teaching years.

Social Security benefits are calculated using a progressive formula that provides higher replacement rates for lower lifetime earnings. The theory behind WEP and GPO is that people who worked in non-Social Security jobs appear to have lower Social Security-covered earnings than they actually earned throughout their careers.

However, this logic creates harsh realities for teachers who may have worked multiple jobs or changed careers, often penalizing those who dedicated their lives to public service.

The Windfall Elimination Provision reduces your own Social Security benefits if you receive a pension from work where you didn’t pay Social Security taxes – like your TRS pension.

WEP affects you if:

The reduction can be substantial. For 2024, WEP can reduce your Social Security benefits by up to $557 per month, though the actual reduction depends on your years of substantial Social Security earnings.

Social Security defines “substantial earnings” as earnings above certain thresholds that change annually. For 2024, substantial earnings means earning at least $31,275 in Social Security-covered employment during a calendar year.

If you have 30 or more years of substantial earnings, WEP doesn’t apply to you at all. The reduction decreases as your years of substantial earnings increase:

The Government Pension Offset is often more devastating than WEP because it can completely eliminate spousal or survivor Social Security benefits.

GPO reduces spousal or survivor Social Security benefits by two-thirds of your TRS pension amount. This affects:

For example, if your monthly TRS pension is $3,000, GPO reduces your spousal Social Security benefits by $2,000 (two-thirds of $3,000). If your spousal benefit would have been $1,800, GPO eliminates it entirely.

Many Texas teachers discover GPO’s impact too late in their planning process. A teacher expecting to receive $1,500 monthly in spousal Social Security benefits might find these benefits completely eliminated due to their TRS pension.

This particularly affects teachers who:

Understanding your potential reductions requires gathering specific information about your work history and projected benefits.

To estimate WEP’s impact:

The Social Security Administration provides detailed tables showing WEP reductions based on your years of coverage and when you become eligible for benefits.

For GPO calculations, you need:

The GPO reduction equals two-thirds of your TRS pension. If this amount exceeds your spousal/survivor benefit, those benefits disappear entirely.

Since GPO is based on your TRS pension, let’s look at how Texas calculates retirement benefits:

Example only (with stated assumptions):

Teacher with 25 years of service and $65,000 final average salary

Benefit % = 25 years × 2.3% = 57.5%

Annual Pension = $65,000 × 57.5% = $37,375

Monthly Pension = $3,115

GPO reduction = $3,115 × 2/3 = $2,077 per month

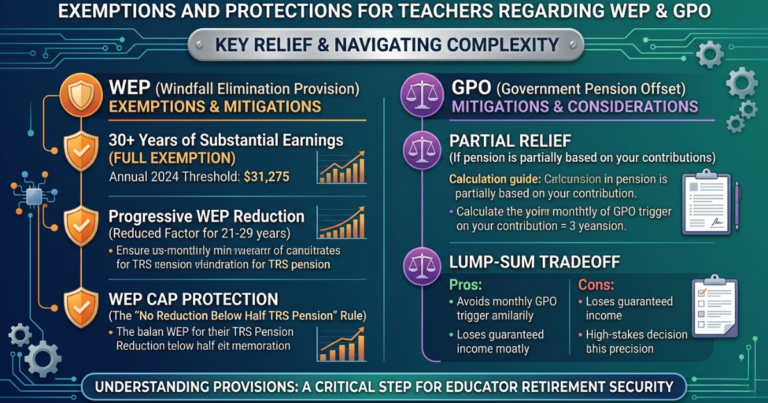

While WEP and GPO affect most Texas teachers with Social Security benefits, some exemptions and protections exist.

WEP cannot reduce your Social Security benefits below what they would be under an alternative calculation method. Additionally, WEP cannot reduce your Social Security benefit by more than half of your TRS pension amount.

Teachers with 30 or more years of substantial Social Security earnings are completely exempt from WEP.

GPO has fewer protections than WEP. However, if your TRS pension is based partly on contributions you made (rather than employer contributions), you might qualify for partial relief.

Some teachers also explore strategies like taking lump-sum distributions from TRS to avoid the monthly pension that triggers GPO, though this approach has significant tradeoffs.

While you can’t avoid WEP and GPO entirely, strategic planning can minimize their impact.

If you’re early in your teaching career and haven’t reached 30 years of substantial Social Security earnings, consider:

The timing of when you claim different benefits can affect your overall retirement income:

Diversifying retirement income beyond TRS and Social Security becomes crucial:

Rather than hoping WEP and GPO won’t affect you, take proactive steps to understand and plan around these reductions.

Visit the Social Security Administration website to create a my Social Security account. Review your earnings record and get benefit estimates that account for WEP if applicable.

For TRS projections, use the TRS online calculator or contact TRS directly for personalized benefit estimates.

Keep detailed records of all employment, especially jobs where you paid Social Security taxes. This documentation proves crucial when determining your years of substantial earnings.

Given the complexity of WEP and GPO calculations, many teachers benefit from professional retirement planning assistance. Look for advisors familiar with teacher-specific retirement challenges.

Stay informed about legislative efforts to reform or repeal WEP and GPO. Contact your representatives to share how these provisions affect your retirement security.

Since WEP and GPO reduce expected benefits, building additional retirement savings becomes even more important. Focus on:

If you receive any monthly TRS pension and are eligible for Social Security benefits, WEP will likely apply unless you have 30+ years of substantial Social Security earnings. GPO applies to spousal/survivor benefits regardless of your years of Social Security coverage.

Some teachers consider lump-sum distributions to avoid monthly pensions that trigger GPO. However, this strategy has significant risks, including losing guaranteed income and potential tax consequences. Consult with a financial advisor before pursuing this approach.

Only if you pay Social Security taxes on those earnings. In Texas, substitute teachers typically contribute to TRS, not Social Security, so these earnings wouldn’t count toward substantial earnings for WEP purposes.

WEP only affects your own Social Security benefits, not benefits based on an ex-spouse’s record. However, if you’re the teacher receiving TRS benefits, GPO could affect any spousal benefits you might claim on your ex-spouse’s Social Security record.

Yes, if you work in Social Security-covered employment after retiring from teaching. Each additional year of substantial earnings reduces WEP’s impact, and reaching 30 years eliminates WEP entirely.

Various bills have been introduced in Congress to modify or repeal WEP and GPO, but none have been enacted. Texas teachers should stay informed about legislative developments but shouldn’t base retirement planning on potential changes.

Check your Social Security earnings record through your my Social Security account. All Social Security-covered employment should appear there with the corresponding earnings amounts.

No, your TRS pension doesn’t affect your spouse’s own Social Security benefits. However, GPO could eliminate any spousal benefits your spouse might claim on your Social Security record, and it would affect any survivor benefits they might receive after you pass away.

Use the TRS calculator to estimate your pension and identify potential income gaps.