Is DIY Retirement Planning Risky for Texas Teachers?

DIY retirement planning can lead to costly mistakes. Here’s what Texas teachers should consider.

Taxes on TRS Pension: What Texas Teachers Need to Know Understanding taxes on TRS pension benefits is crucial for Texas teachers planning their retirement. While your Teacher Retirement System of Texas pension provides a foundation for your retirement income, knowing how it’s taxed can help you make better financial decisions and avoid surprises come tax […]

Understanding taxes on TRS pension benefits is crucial for Texas teachers planning their retirement. While your Teacher Retirement System of Texas pension provides a foundation for your retirement income, knowing how it’s taxed can help you make better financial decisions and avoid surprises come tax season.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

The good news is that Texas TRS pension benefits receive favorable tax treatment compared to many other retirement income sources. However, the tax implications can vary significantly depending on your specific situation, other income sources, and where you live during retirement.

Your TRS pension is subject to federal income tax, but understanding exactly how much depends on several factors. Unlike Social Security benefits, which may be partially tax-free for some retirees, your TRS pension is generally fully taxable at the federal level.

Use the TRS calculator to estimate your pension and identify potential income gaps.

The reason your TRS pension faces federal taxation comes down to how it was funded. During your teaching career, you contributed to TRS with pre-tax dollars taken directly from your paycheck. Your employer also made contributions on your behalf. Since neither you nor your employer paid federal income tax on these contributions, the IRS considers your pension payments as taxable income when you receive them.

This tax treatment is similar to traditional 401(k) or IRA withdrawals. You received a tax break when the money went in, so you pay taxes when it comes out.

Your TRS pension income is taxed as ordinary income using the same federal tax brackets that apply to wages. For most retired teachers, this means your pension will be taxed at rates ranging from 10% to 22%, depending on your total income and filing status.

The key factor is your total taxable income, which includes your TRS pension plus any other income sources like Social Security, part-time work, investment income, or withdrawals from retirement accounts.

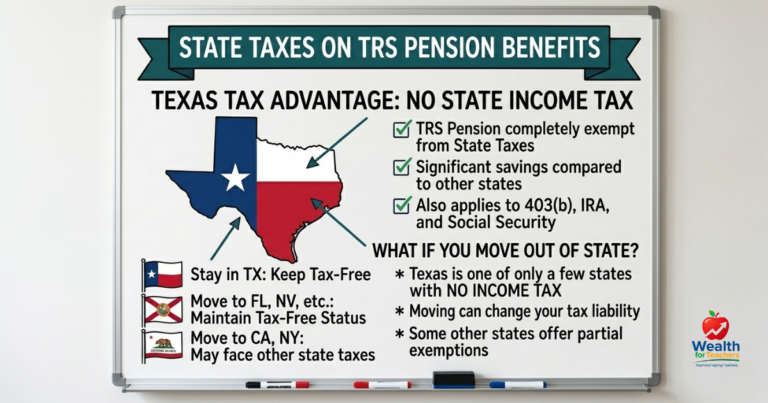

One of the biggest advantages for Texas teachers is that Texas has no state income tax. This means your TRS pension income is completely exempt from state taxes, regardless of how much you receive.

Living in Texas during retirement provides a significant tax advantage. While teachers in states like California, New York, or Minnesota might pay 5% to 13% in state taxes on their pension income, Texas teachers keep more of their retirement benefits.

This tax-free treatment extends to all forms of retirement income in Texas, including TRS pensions, 403(b) withdrawals, IRA distributions, and Social Security benefits.

If you move to another state after retiring from Texas, your TRS pension may become subject to that state’s income tax laws. However, some states provide favorable treatment for government pension income, including teacher pensions from other states.

States with no income tax include Florida, Nevada, South Dakota, Tennessee, Washington, Wyoming, and Alaska. Moving to any of these states would maintain your tax-free status on TRS pension income.

Understanding the exact amount of your TRS pension subject to federal taxes requires looking at the source of your pension benefits and any after-tax contributions you may have made.

For most Texas teachers, the vast majority of your TRS pension will be fully taxable at the federal level. This includes benefits earned from:

A small portion of your TRS pension might be tax-free if you made after-tax contributions. This could happen if you:

TRS will provide you with tax documentation showing the taxable and non-taxable portions of your pension when you begin receiving benefits.

Let’s look at a realistic example for a Texas teacher:

Example assumptions:

TRS Pension Calculation:

Federal Tax Impact:

Also make sure you understand your TRS Tier 1 vs Tier 2 vs Tier 3 explained simply.

Smart tax planning can help you minimize the impact of taxes on your TRS pension and maximize your retirement income.

Since your federal tax rate depends on total income, consider timing other income sources strategically. If you have traditional IRAs or 403(b) accounts, you might want to manage withdrawals to stay in lower tax brackets.

For example, if taking a large IRA withdrawal would push you into a higher tax bracket, consider spreading withdrawals across multiple years.

If you have traditional retirement accounts alongside your TRS pension, converting some funds to Roth IRAs during lower-income years could reduce future tax obligations. This strategy works best when your current tax rate is lower than expected future rates.

If you plan to make charitable contributions, consider strategies that can offset pension income taxes:

If you’re considering moving during retirement, factor in state tax treatment of pension income. Some states that tax regular income may still exempt pension income, while others tax everything.

TRS allows you to have federal taxes withheld from your monthly pension payments, which can help you avoid owing taxes when you file your return.

You can elect federal tax withholding when you apply for retirement benefits or change it later through your TRS online account. Withholding options typically include fixed dollar amounts or percentages.

Consider withholding at a rate that covers your expected tax liability. A good starting point is 10-15% for most retirees, but your situation may require more or less.

If you don’t elect withholding or it’s not sufficient to cover your total tax liability, you may need to make quarterly estimated tax payments to avoid penalties.

This is particularly important if you have other income sources like part-time work, investment income, or retirement account withdrawals that don’t have taxes withheld.

Many Texas teachers consider relocating during retirement, and understanding the tax implications is crucial for financial planning.

Several states provide favorable treatment for pension income:

Some popular retirement destinations have higher tax rates on pension income:

The timing of your move can impact your tax liability. Generally, you’ll owe taxes to the state where you’re a resident when you receive the pension income, not necessarily where you earned it.

While understanding taxes on your TRS pension is important, don’t let tax concerns overshadow sound retirement planning principles.

Rather than fixating solely on taxes, consider your complete retirement financial picture. Your TRS pension provides a guaranteed income stream that many private sector workers wish they had. Even after taxes, this reliable income is valuable.

Create a retirement income strategy that includes different types of accounts:

This diversification gives you flexibility to manage your tax bracket in retirement by choosing which accounts to withdraw from each year.

Consider working with tax professionals and financial advisors who understand teacher retirement benefits. They can help you develop strategies specific to your situation and ensure you’re taking advantage of all available tax benefits.

Tax laws change over time, and what applies today might be different when you retire. Stay informed about proposed changes to tax laws and how they might affect your retirement planning.

No, your TRS pension is taxed as ordinary income at federal tax rates, just like traditional IRA or 401(k) withdrawals. The main advantage is that it’s not subject to state income tax in Texas, while other retirement accounts may be taxed by states you move to.

Moving to most other states would likely increase your taxes, not reduce them, since Texas has no state income tax. However, moving to other no-tax states like Florida or Nevada would maintain your tax-free status. Some states offer partial exemptions for government pension income.

No, TRS pension benefits are not subject to Social Security or Medicare payroll taxes. These taxes only apply to earned income from employment, not pension income. However, if you work part-time during retirement, those earnings would be subject to payroll taxes.

If you don’t have enough taxes withheld and owe $1,000 or more when you file your return, you may face underpayment penalties. You can avoid this by making quarterly estimated tax payments or increasing your withholding amount through TRS.

Yes, TRS disability retirement benefits are generally taxed the same as regular pension benefits. They’re subject to federal income tax but not Texas state tax. However, if you’re under minimum retirement age, you might be eligible for some tax breaks on disability income.

No, you cannot roll over your monthly TRS pension payments to another retirement account. Once you begin receiving pension payments, they must be taken as income and are subject to applicable taxes. However, you can roll over any lump-sum distributions from TRS supplemental accounts.

If you elect the Partial Lump Sum Option (PLSO), the lump sum portion is subject to federal income tax in the year you receive it. This could potentially push you into a higher tax bracket for that year. The remaining monthly pension payments are then taxed as regular income when received.

Yes, your TRS pension income is included when determining if your Social Security benefits are taxable. If your combined income (including TRS pension, Social Security, and other income) exceeds certain thresholds, up to 85% of your Social Security benefits may become taxable at the federal level.

Use the TRS calculator to estimate your pension and identify potential income gaps.

DIY retirement planning can lead to costly mistakes. Here’s what Texas teachers should consider.

Market swings can impact your retirement income more than you think. Here’s how teachers are affected.