The Biggest Retirement Regrets Teachers Don’t Realize Until It’s Too Late

Many teachers regret key retirement decisions. Learn what to avoid before it’s too late.

Teacher Retirement System Benefits for Texas Educators The Teacher Retirement System of Texas (TRS) provides comprehensive retirement benefits that form the foundation of financial security for Texas educators. With over 1.6 million active and retired members, TRS stands as one of the largest public retirement systems in the United States, specifically designed to support teachers, […]

The Teacher Retirement System of Texas (TRS) provides comprehensive retirement benefits that form the foundation of financial security for Texas educators. With over 1.6 million active and retired members, TRS stands as one of the largest public retirement systems in the United States, specifically designed to support teachers, administrators, and other education professionals throughout their careers and into retirement.

Understanding your TRS benefits is crucial for making informed decisions about your financial future. From monthly pension payments to healthcare coverage, these benefits represent decades of service and dedication to Texas education. Many educators don’t fully grasp the value of what they’re earning through their years of service, which can lead to costly mistakes in retirement planning.

Texas Teacher Retirement Guide

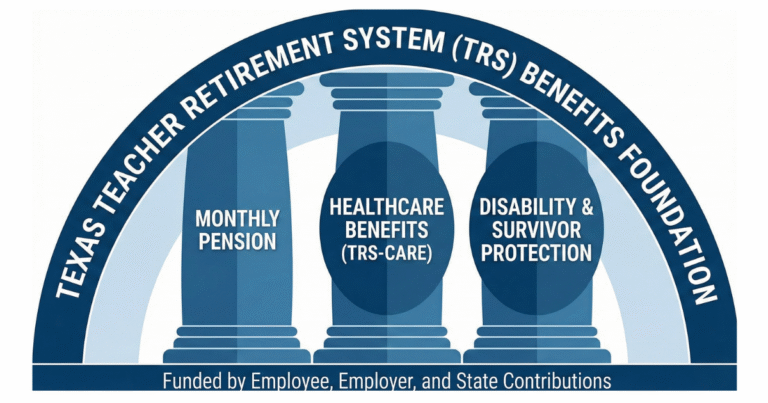

Texas teachers earn multiple types of benefits through TRS membership that extend far beyond a simple retirement check. The system operates as a defined benefit pension plan, meaning your retirement income is calculated based on a specific formula rather than market performance.

The core benefits package includes:

These benefits are funded through a combination of employee contributions (currently 8.25% of salary), employer contributions from school districts, and state funding. The strength of this three-legged funding structure helps ensure the long-term stability of your benefits.

Your TRS pension represents the cornerstone of your retirement income. The monthly benefit amount is calculated using a formula that considers three key factors: your years of service credit, your highest average salary, and a multiplier that increases with additional years of service.

You earn service credit for each year you work as a TRS-covered employee. Part-time employees earn proportional credit based on their percentage of full-time employment. Some educators can also purchase additional service credit for previous teaching experience in other states or for military service.

The highest average salary calculation uses your five highest-paid consecutive years of TRS-covered employment. This typically occurs during your final years of service when salary increases and administrative roles may boost your earning potential.

TRS offers several retirement options:

Healthcare benefits through TRS-Care provide essential medical coverage for retirees and their eligible dependents. This benefit often proves more valuable than the monthly pension itself, given the high cost of healthcare for seniors.

TRS-Care operates as a comprehensive health plan offering medical, prescription drug, and mental health coverage. The plan includes multiple coverage options to meet different needs and budgets, from basic medical coverage to more comprehensive plans with lower out-of-pocket costs.

Eligibility for TRS-Care requires retirement from TRS with at least 10 years of service credit. The premium costs are subsidized based on your years of service, with longer-serving retirees paying significantly less for their coverage.

When you become eligible for Medicare at age 65, TRS-Care coordinates with Medicare as a secondary payer. This coordination often provides superior coverage compared to Medicare alone, while keeping your out-of-pocket costs manageable.

Understanding how TRS-Care works with Medicare is crucial for planning your healthcare costs in retirement. Many retirees find that maintaining both coverages provides the best protection against unexpected medical expenses.

TRS provides financial protection if you become disabled or if death occurs before retirement. These benefits ensure that your years of service aren’t lost if unforeseen circumstances prevent you from completing your career.

If you become unable to perform your duties due to a physical or mental condition, you may qualify for disability retirement benefits. The monthly benefit is calculated the same as a standard retirement, but you can qualify regardless of your age or years of service if the disability is job-related.

For non-job-related disabilities, you need at least 10 years of service credit and must be unable to engage in any substantial gainful activity. The application process requires extensive medical documentation and can take several months to complete.

If you die while actively employed by TRS, your beneficiaries may be eligible for monthly survivor benefits or a lump-sum death benefit. The amount depends on your years of service and salary at the time of death.

Active employees with at least 10 years of service credit can provide lifetime monthly benefits to an eligible surviving spouse. This benefit provides crucial financial security for families who depend on a teacher’s income.

Active TRS members have access to health insurance through TRS-ActiveCare, which provides comprehensive medical coverage at competitive rates. This program leverages the purchasing power of the entire TRS membership to negotiate favorable rates with healthcare providers.

TRS-ActiveCare offers multiple plan options, from high-deductible health savings account-compatible plans to traditional HMO and PPO options. The variety ensures that teachers can find coverage that matches their healthcare needs and budget constraints.

Many teachers don’t realize that their participation in TRS-ActiveCare during their working years can influence their retiree healthcare options. Continuous coverage history may affect premium calculations and eligibility for certain TRS-Care plans.

Becoming eligible for TRS benefits requires meeting specific service and employment criteria. Understanding these requirements helps you plan your career path and retirement timing effectively.

TRS membership is mandatory for most Texas public school employees, including:

Substitute teachers can also earn TRS service credit if they work sufficient days during the school year. The exact requirements vary by district and employment classification.

You become vested in TRS benefits after completing five years of service credit. Vesting means you have a guaranteed right to future benefits, even if you leave Texas public education before retirement.

Non-vested members who leave TRS employment can withdraw their contributions plus limited interest, but they forfeit any employer contributions and future benefit rights. This makes understanding why most teachers underestimate their TRS Pension value critical for career planning decisions.

Maximizing your TRS benefits requires strategic career planning and understanding how different decisions impact your future retirement security. Small choices made throughout your career can result in significantly different retirement outcomes.

Since your pension is based on your five highest consecutive years of salary, timing salary increases and career advancement can significantly impact your retirement income. Consider pursuing administrative roles, advanced degrees, or additional certifications during your final years of service when they’ll have the most impact on your benefit calculation.

However, avoid artificial salary spikes that might trigger TRS scrutiny. Legitimate career advancement and professional development provide sustainable paths to higher retirement benefits.

Every year of service credit matters for both eligibility and benefit calculation. If you have previous teaching experience in other states or military service, investigate whether you can purchase that time as TRS service credit.

The cost of purchasing service credit is typically less than the increased lifetime benefit value, making it one of the best investments many teachers can make. However, the rules are complex, and timing matters, so research your options early in your career.

The Rule of 80 often provides the most advantageous retirement timing for Texas teachers. By retiring when your age plus service years equals 80, you can avoid early retirement penalties while potentially enjoying many years of retirement benefits.

Planning your career timeline around the Rule of 80 might influence decisions about when to start teaching, whether to take breaks from education, and how long to continue working.

Many Texas teachers make costly mistakes regarding their TRS benefits simply because they don’t understand the system. Here are better approaches to common pitfalls:

Rather than putting off learning about TRS until near retirement, start understanding your benefits early in your career. Log into your TRS online account regularly to track your service credit and salary history. Attend TRS workshops when available, and read the annual member statements carefully.

If you leave education before vesting, avoid the temptation to withdraw your TRS contributions unless absolutely necessary. Leaving your money in the system preserves your service credit, and you might return to education later. If you do return, you’ll be grateful you kept your TRS account active.

Don’t assume Medicare will handle all your healthcare needs in retirement. Start planning for TRS-Care eligibility and costs well before you retire. Healthcare represents one of the largest expenses for retirees, and proper planning can save thousands of dollars annually.

Rather than making retirement decisions based solely on TRS benefits, consider your complete financial picture. This includes Social Security benefits, personal savings, and other income sources. Many teachers benefit from consulting with retirement specialists who understand the unique aspects of educator retirement planning.

The Texas Teacher Retirement System website provides official information and calculators to help you model different retirement scenarios and their financial implications.

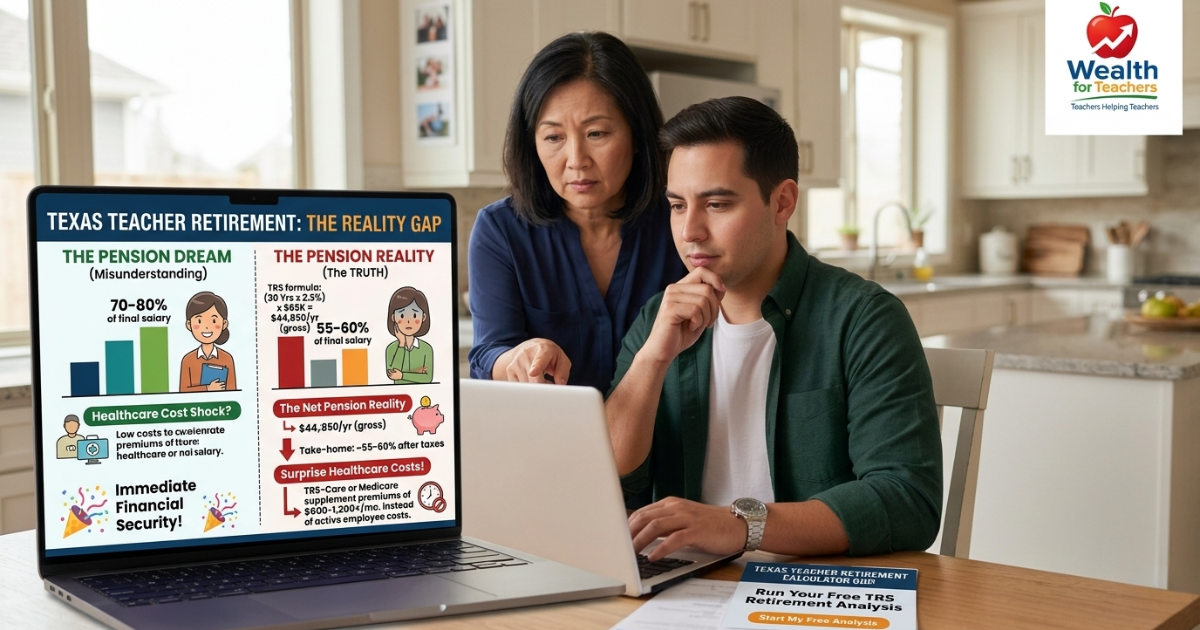

Your pension amount depends on your years of service, highest average salary, and the TRS multiplier. For example, a teacher with 25 years of service and a $60,000 highest average salary would receive approximately $34,500 annually (25 × $60,000 × 2.3% average multiplier). Use the TRS website calculator for personalized estimates.

Yes, you can collect both TRS pension benefits and Social Security if you’ve earned sufficient credits in Social Security-covered employment. However, be aware of potential Social Security reductions due to the Windfall Elimination Provision if you have significant non-Social Security covered earnings.

Your TRS benefits follow you anywhere you live in retirement. You’ll continue receiving your monthly pension and can maintain TRS-Care health coverage regardless of your state of residence. However, you cannot earn additional TRS service credit by teaching in other states.

You’re eligible for TRS-Care if you retire from TRS with at least 10 years of service credit. The premium you pay depends on your years of service, with longer service resulting in lower premiums. You can also cover eligible dependents under your TRS-Care plan.

Yes, but there are restrictions. You can return to work for a TRS-covered employer without affecting your benefits if you meet certain criteria, including a waiting period after retirement. However, there are limits on the positions you can hold and compensation you can receive.

If you’re vested (5+ years of service), you can leave your contributions in TRS and claim benefits when you reach retirement age. If you’re not vested, you can withdraw your contributions but will lose any employer contributions and future benefit rights.

Divorce can impact your TRS benefits if your spouse is awarded a portion in the divorce settlement. TRS can divide benefits through a Qualified Domestic Relations Order (QDRO). It’s important to understand these implications during divorce proceedings and work with attorneys familiar with TRS rules.

TRS benefits are backed by the State of Texas and have strong legal protections. However, like all pension systems, TRS faces long-term funding challenges. The Texas Legislature periodically makes adjustments to ensure system sustainability, which may affect future benefit levels or contribution requirements.

Understanding your Teacher Retirement System benefits is just the first step toward a secure retirement. Get personalized guidance on maximizing your TRS benefits and creating a comprehensive retirement plan tailored to your specific situation.

Many teachers regret key retirement decisions. Learn what to avoid before it’s too late.

DIY retirement planning can lead to costly mistakes. Here’s what Texas teachers should consider.