Is DIY Retirement Planning Risky for Texas Teachers?

DIY retirement planning can lead to costly mistakes. Here’s what Texas teachers should consider.

Many teachers regret key retirement decisions. Learn what to avoid before it’s too late.

Every month, Texas teachers retire with what they believe is a solid plan, only to face harsh financial realities within the first year. The teacher retirement regrets that surface are often preventable but devastating: insufficient income to maintain their lifestyle, unexpected healthcare costs, and the painful realization that their TRS pension alone won’t cover basic expenses.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

These regrets don’t emerge from poor intentions or lack of intelligence. They stem from widespread misunderstandings about how retirement actually works for Texas educators.

The most damaging misconception? Believing that 30 years of service automatically equals financial security. Many teachers assume their TRS pension will replace enough income to maintain their pre-retirement lifestyle, but the math tells a different story.

For comprehensive guidance on avoiding these costly mistakes, review our Texas Teacher Retirement Planning Guide before making any final retirement decisions.

Most retirement plans fail because they are never tested under real-world conditions. Teachers often base their retirement timeline on best-case scenarios without accounting for inflation, healthcare premiums, or unexpected expenses that can derail even well-intentioned plans.

The most common teacher retirement regret involves income replacement assumptions that don’t match reality. Many Texas teachers expect their TRS pension to replace 70-80% of their working income, but the actual percentage is often much lower.

Use the TRS calculator to estimate your pension and identify potential income gaps.

Texas TRS calculates pensions using a flat 2.3% multiplier per year of service. The formula is straightforward: Annual Pension = (Years of Service × 0.023) × Final Average Salary.

Consider Sarah, a Texas teacher with 30 years of service and a final average salary of $65,000. Her annual TRS pension would be: (30 × 0.023) × $65,000 = $44,850 per year, or about $3,738 per month before taxes.

This represents only 69% of her final salary. After taxes and the loss of active teacher benefits, Sarah’s actual take-home income drops to roughly 55-60% of her working income. For many teachers, this income reduction creates immediate financial stress.

The regret intensifies when teachers realize they could have supplemented their TRS pension more effectively through systematic 403(b) contributions or other investment strategies during their working years.

Three factors contribute to unrealistic income expectations:

Many teachers also forget that their TRS pension, while guaranteed, doesn’t include automatic cost-of-living adjustments. A $3,738 monthly pension today will have less purchasing power in 10 or 15 years.

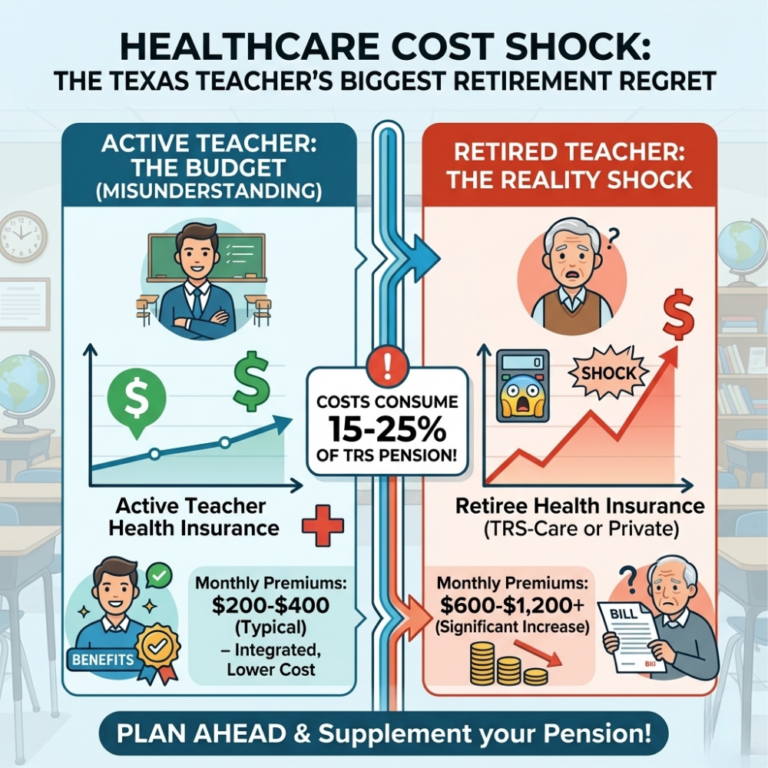

Healthcare expenses represent the fastest-growing category of teacher retirement regrets. The transition from active teacher health insurance to TRS-Care or Medicare creates significant cost increases that catch many retirees unprepared.

Active Texas teachers typically pay $200-400 per month for comprehensive health insurance. Retired teachers often face monthly premiums of $600-1,200 or more, depending on their coverage choices and Medicare supplement needs.

This cost shock is particularly painful for teachers who retire before Medicare eligibility at age 65. Early retirees must bridge their healthcare coverage through TRS-Care or private insurance, both of which cost significantly more than active teacher plans.

Even Medicare-eligible retirees face unexpected costs. Standard Medicare doesn’t cover everything, and many teachers discover they need Medicare supplement insurance to maintain adequate healthcare protection.

A teacher couple retiring at age 65 might pay $400-600 per month combined for Medicare supplement insurance, plus additional costs for prescription drug coverage and dental insurance. These expenses weren’t part of their working budget and can consume 15-25% of their TRS pension income.

Texas teachers become eligible for unreduced TRS benefits with 30 years of service, regardless of age. This creates a powerful incentive to retire early, but early retirement often leads to significant regrets.

The primary issues with early retirement include:

Consider Maria, who retires at age 52 with 30 years of service. She’ll need her retirement savings to last potentially 40+ years, but she has only accumulated modest 403(b) savings. Her TRS pension covers basic expenses, but she lacks the supplemental income needed for travel, home maintenance, or unexpected costs.

For guidance on optimal retirement timing, review our article on the best time of year for Texas teachers to retire.

Beyond financial regrets, many teachers who retire early experience unexpected emotional challenges. The loss of professional identity, social connections, and daily structure can create depression and anxiety that compound financial stress.

Teachers who thought retirement would provide freedom often find themselves financially constrained and socially isolated, leading to regrets about their timing decision.

Texas teachers participate in Social Security, but many make costly timing mistakes that reduce their lifetime benefits. The most common regret involves claiming Social Security too early or failing to coordinate Social Security timing with TRS pension income.

Teachers can claim reduced Social Security benefits as early as age 62, but this permanently reduces their monthly payments by 25-30%. For a teacher entitled to $2,000 per month at full retirement age, early claiming at 62 reduces benefits to approximately $1,400 per month for life.

The regret becomes acute when teachers realize they could have delayed Social Security to age 70 and received delayed retirement credits worth 8% per year. A $2,000 benefit at full retirement age grows to $2,640 per month if claimed at age 70.

Many teachers claim Social Security early because they need the income, not realizing they could have better coordinated their TRS pension with Social Security timing to maximize lifetime benefits.

A strategic approach might involve living primarily on TRS pension income from ages 62-70 while allowing Social Security benefits to grow, then adding larger Social Security payments at age 70 for a more comfortable later retirement period.

Teachers with 403(b) or IRA accounts often regret their withdrawal strategies once retirement begins. The most damaging mistakes involve withdrawing too much too early or failing to understand how market volatility affects retirement income.

Many teachers assume they can safely withdraw 4-5% annually from their investment accounts without depleting them. However, this rule doesn’t account for sequence of returns risk, where early market downturns can permanently damage portfolio longevity.

For detailed strategies on managing retirement account withdrawals, see our guide on how teachers can create retirement income without selling assets.

Teachers often need large withdrawals for home repairs, vehicles, or family emergencies during their early retirement years. Taking these withdrawals during market downturns can force teachers to sell investments at losses, reducing their account values permanently.

The regret compounds when teachers realize they could have structured their accounts differently or maintained cash reserves specifically for large expenses during retirement.

Understanding how market volatility impacts retired teachers’ income is crucial for avoiding these withdrawal timing mistakes.

Texas doesn’t tax retirement income, but federal taxes apply to TRS pension payments. Most teachers keep 85-90% of their gross pension after federal taxes, depending on their total retirement income and tax planning strategies.

Yes, but TRS has strict rules about post-retirement employment. You can work up to 8 hours per day or 80 hours per month without affecting your pension, but exceeding these limits can suspend your TRS payments.

Generally yes, especially if your district provides matching contributions. Even short-term 403(b) growth can provide valuable supplemental income during retirement.

This depends on the survivor benefit option you select at retirement. Joint and survivor options provide ongoing payments to your spouse but reduce your monthly pension during your lifetime.

No, survivor benefit elections are permanent once you retire. This is why careful planning before retirement is crucial.

Use the TRS calculator to estimate your pension and identify potential income gaps.

DIY retirement planning can lead to costly mistakes. Here’s what Texas teachers should consider.

Market swings can impact your retirement income more than you think. Here’s how teachers are affected.