The Biggest Retirement Regrets Teachers Don’t Realize Until It’s Too Late

Many teachers regret key retirement decisions. Learn what to avoid before it’s too late.

Market swings can impact your retirement income more than you think. Here’s how teachers are affected.

Market risk teacher retirement planning goes far beyond simply having enough money saved. When markets drop just as you retire or early in retirement, the sequence of returns can permanently damage your financial security—even if your portfolio recovers later.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

Texas teachers face unique challenges when market volatility hits during retirement. Unlike private sector workers who might rely entirely on 401(k) accounts, teachers have both TRS pensions and personal savings to coordinate. This complexity creates specific risks that many teachers overlook until it’s too late.

The timing of market downturns matters more than the downturn itself. A teacher who retires into a bear market faces dramatically different outcomes than one who experiences the same market decline ten years into retirement.

Most teachers assume their Texas Teacher Retirement Planning Guide ends when they accumulate enough assets. In reality, managing market risk during the withdrawal phase requires completely different strategies than building wealth during your working years.

Most retirement plans fail because they are never tested under real-world market conditions. Teachers often create plans based on average returns and smooth projections, but markets don’t deliver average returns in any predictable sequence.

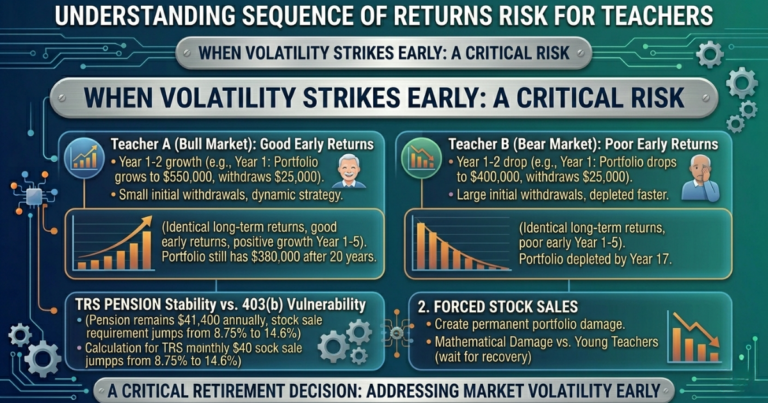

Sequence of returns risk occurs when poor market performance happens early in retirement, forcing you to withdraw money from declining portfolio values. This creates a mathematical spiral that good returns later cannot fix.

Use the TRS calculator to estimate your pension and identify potential income gaps.

Consider two Texas teachers, both retiring with identical $500,000 403(b) accounts and identical long-term returns. Teacher A retires into a bull market, while Teacher B retires into a bear market:

Teacher A (Good Early Returns):

Teacher B (Poor Early Returns):

Both teachers experienced identical average returns over time. The only difference was timing. Teacher B’s portfolio never recovered because early withdrawals during market declines locked in permanent losses.

Texas teachers cannot control market timing, but they can control withdrawal strategies and asset allocation decisions that either amplify or reduce sequence risk.

Texas teachers typically retire with three income sources, each affected differently by market volatility:

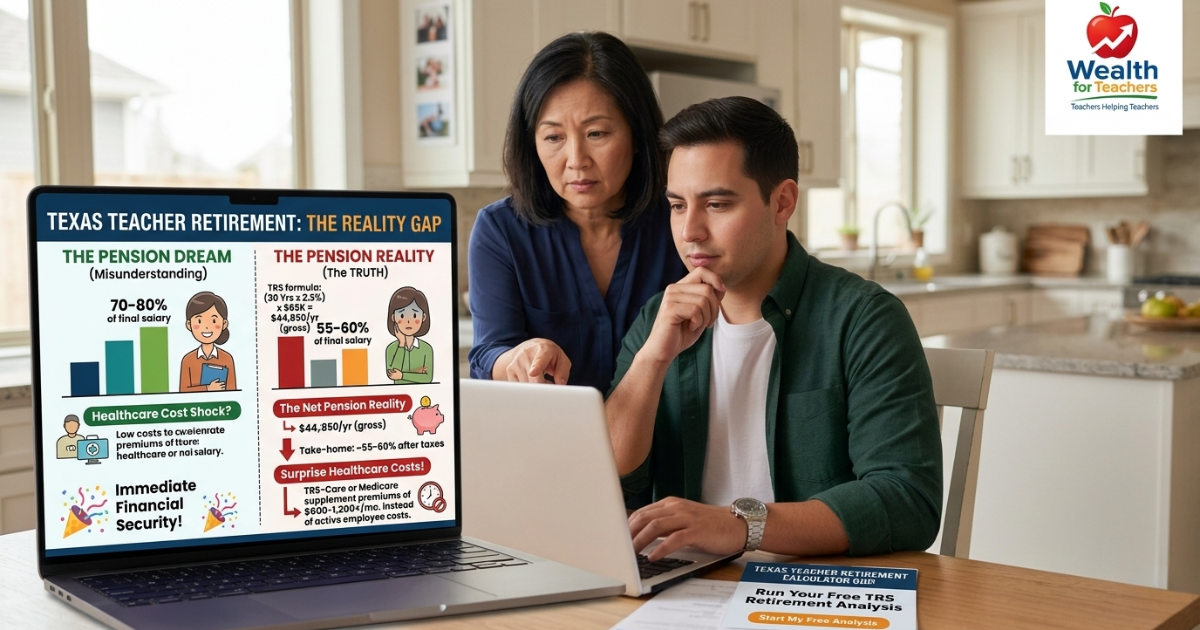

Your Texas TRS pension provides reliable income regardless of market conditions. The formula remains consistent: Annual Pension = (Years of Service × 0.023) × Final Average Salary. A teacher with 30 years of service and $60,000 final average salary receives $41,400 annually whether markets soar or crash.

This stability becomes crucial during market volatility. Your TRS pension acts as a foundation, allowing you to adjust withdrawals from volatile accounts without compromising basic living expenses.

Your 403(b) accounts and personal investments bear the full impact of market volatility. When you need to withdraw $30,000 during a market crash, you’re forced to sell more shares to generate the same dollar amount.

This forced selling during downturns creates permanent portfolio damage. Unlike younger teachers who can wait for recovery, retirees must continue withdrawals regardless of market conditions.

Market volatility doesn’t directly affect Social Security benefits, but it can influence your claiming strategy. The WEP and GPO Explained for Texas Teachers shows how these provisions might reduce your Social Security benefits, making you more dependent on volatile investment accounts.

Many Texas teachers plan early retirement around age 55-60, believing their accumulated savings will bridge the gap until full Social Security eligibility. Market crashes during this bridge period create devastating consequences.

Early retirees often withdraw from investment accounts for 5-10 years before accessing full benefits. A market crash during this period forces higher withdrawal rates from declining portfolios.

Consider a teacher retiring at 58 with a $400,000 portfolio, planning to withdraw $35,000 annually until Social Security begins. A 40% market crash in year one reduces the portfolio to $240,000, but withdrawal needs remain unchanged. The required withdrawal rate jumps from 8.75% to 14.6%—an unsustainable level.

Young investors can wait decades for market recovery. Retirees have limited time horizons and ongoing withdrawal needs that prevent full recovery participation.

Even when markets recover, portfolios depleted by early withdrawals during downturns never catch up to their original trajectory. The mathematical damage becomes permanent.

Creating a cash buffer covering 2-3 years of expenses allows you to avoid stock sales during market downturns. This buffer gives your equity portfolio time to recover without forced selling pressure.

A bond ladder provides predictable income streams that mature regardless of market conditions. While yields may be lower, the certainty helps protect against sequence risk during early retirement years.

Fixed withdrawal strategies ignore market conditions. Dynamic approaches adjust spending based on portfolio performance and market valuations.

The guardrails approach increases spending after good market years and reduces spending after poor years. While this requires lifestyle flexibility, it significantly reduces the probability of portfolio depletion.

Where you hold different asset types affects tax efficiency and withdrawal flexibility. Holding bonds in tax-deferred accounts and stocks in taxable accounts provides better withdrawal options during market volatility.

How Taxes Impact Teacher Retirement Income explains how tax-efficient withdrawals can preserve more of your retirement income during volatile markets.

Q: Should I delay retirement if markets are volatile?

Not necessarily. Your TRS pension provides stability regardless of market conditions. The key is ensuring your personal savings can handle volatility without jeopardizing your lifestyle. One additional year of service increases your annual pension by 2.3% of your final average salary permanently.

Q: How much should I keep in conservative investments during retirement?

Many financial planners suggest keeping 3-5 years of expenses in conservative investments (cash and bonds) to avoid selling stocks during market downturns. This buffer allows your equity investments time to recover.

Q: Can I adjust my TRS pension payments if markets crash?

No. TRS pension payments remain fixed once you retire. This stability is valuable during market volatility, but you cannot increase payments if your other income sources decline.

Q: Should I take the lump sum option instead of monthly TRS payments?

The lump sum option exposes you to full market risk on your entire TRS benefit. Monthly payments provide guaranteed income regardless of market conditions. Most teachers benefit more from the stability of monthly payments, especially during market volatility.

Q: How do I know if my retirement plan can handle a market crash?

Stress-testing involves running your retirement plan through historical market scenarios, including the 2008 financial crisis and early 2000s bear market. How to Stress-Test a Teacher Retirement Plan provides specific methods for testing your plan’s resilience.

Rather than hoping for favorable market timing, build a retirement plan that functions under various market conditions.

Create Multiple Income Layers: Your TRS pension provides the foundation. Add conservative income sources (bonds, CDs) for predictable cash flow. Use growth investments for long-term purchasing power protection.

Implement Flexible Withdrawal Strategies: Instead of fixed withdrawal amounts, create spending categories with different priorities. Essential expenses get covered by guaranteed income sources. Discretionary spending adjusts based on portfolio performance.

Build Market Volatility Buffers: Maintain 3-5 years of expenses in conservative investments. This buffer prevents forced stock sales during market downturns and provides peace of mind during volatile periods.

Stress-Test Before Retiring: Run your retirement plan through historical market scenarios. Understanding how your plan performs during actual market crashes helps identify potential problems before they become permanent damage.

Use the TRS calculator to estimate your pension and identify potential income gaps.

Many teachers regret key retirement decisions. Learn what to avoid before it’s too late.

DIY retirement planning can lead to costly mistakes. Here’s what Texas teachers should consider.