How to Build a Guaranteed Income Floor as a Teacher

Stable income is the foundation of retirement security. Learn how to build it.

TRS Benefits Texas Teachers – Your Complete Guide to Retirement Security As a Texas teacher, your retirement security depends on understanding and maximizing the Teacher Retirement System of Texas benefits available to you. TRS benefits Texas teachers through a comprehensive retirement package that includes pension benefits, healthcare options, and additional financial protections that can provide […]

As a Texas teacher, your retirement security depends on understanding and maximizing the Teacher Retirement System of Texas benefits available to you. TRS benefits Texas teachers through a comprehensive retirement package that includes pension benefits, healthcare options, and additional financial protections that can provide decades of financial stability after your teaching career ends.

The TRS system serves over 1.6 million active and retired educators across Texas, making it one of the largest public retirement systems in the United States. Your years of dedication to educating Texas students have earned you access to these valuable benefits, but knowing how to optimize them requires careful planning and understanding.

Whether you’re a new teacher just starting your career or a veteran educator approaching retirement, understanding your TRS benefits is crucial for making informed decisions about your financial future. This guide will walk you through everything you need to know about maximizing your retirement security through the Texas TRS system.

Teacher Retirement System Texas

The foundation of TRS benefits for Texas teachers is the defined benefit pension plan, which provides a guaranteed monthly income for life after retirement. Unlike 401(k) plans where your retirement income depends on market performance, your TRS pension benefit is calculated using a formula based on your years of service, state rate, and average 5 or 3 years highest salary.

Get Your Free TRS Calculations

Your pension benefit is funded through contributions from you, your employer (school district), and the state of Texas. As an active teacher, you contribute 8.2% of your annual salary to TRS, while your employer contributes on your behalf. These contributions, combined with investment returns on the TRS trust fund, ensure your future pension payments.

The TRS pension system operates as a trust fund, meaning your contributions and those made on your behalf are invested professionally to generate returns that help fund current and future retiree benefits. This pooled investment approach provides stability and professional management that individual teachers couldn’t achieve on their own.

Healthcare coverage represents one of the most valuable TRS benefits Texas teachers receive. TRS-Care provides comprehensive medical, prescription drug, and mental health coverage for eligible retirees and their dependents. This benefit can be worth hundreds of thousands of dollars over your retirement years.

TRS-Care eligibility requires you to meet specific service and age requirements. Generally, you must be eligible for a TRS retirement benefit and have at least 10 years of TRS service credit. The program offers several coverage options, including individual coverage, coverage for you and your spouse, or family coverage that includes dependent children.

The value of TRS-Care becomes especially apparent when you compare it to individual health insurance costs in retirement. Private insurance for retirees can cost $1,000-$2,000 per month or more, making TRS-Care a significant financial benefit that supports your overall retirement security.

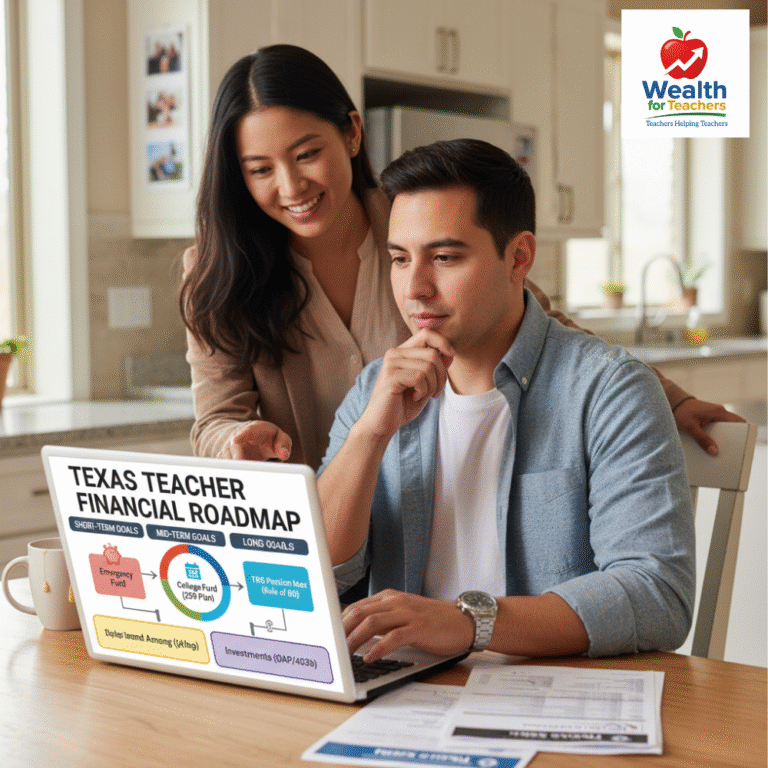

The Optional Annuity Program allows Texas teachers to supplement their TRS pension with additional tax-deferred retirement savings. Through OAP, you can contribute pre-tax dollars to various investment options, similar to a 403(b) plan offered by many school districts.

OAP contributions reduce your current taxable income while building additional retirement wealth. You have control over investment choices within the program, allowing you to customize your portfolio based on your risk tolerance and retirement timeline. This flexibility makes OAP an excellent complement to your guaranteed TRS pension benefits.

Many financial experts recommend contributing to OAP if you can afford to do so, especially early in your career when you have more time for potential growth. Even modest contributions can grow significantly over a 20-30 year teaching career, providing valuable additional income in retirement.

TRS provides important protection for teachers who become disabled or for families of teachers who pass away. These benefits ensure that your service as a Texas educator provides security even in difficult circumstances.

Disability retirement benefits are available to teachers who become unable to perform their job duties due to mental or physical incapacity. The benefit amount depends on your years of service and salary, but provides crucial income protection when you can no longer teach.

Survivor benefits provide monthly income to eligible spouses and dependent children of deceased TRS members. This protection ensures your family maintains financial stability even if tragedy strikes. The benefit amount depends on your service credit and salary at the time of death.

Understanding vesting and service credit rules is crucial for maximizing your TRS benefits. Vesting refers to your right to receive pension benefits, while service credit determines the amount of those benefits.

Texas teachers become vested in TRS after completing five years of service credit. Once vested, you have earned the right to receive a pension benefit when you reach retirement age, even if you leave teaching before retiring. However, the amount of your benefit depends on your total years of service credit.

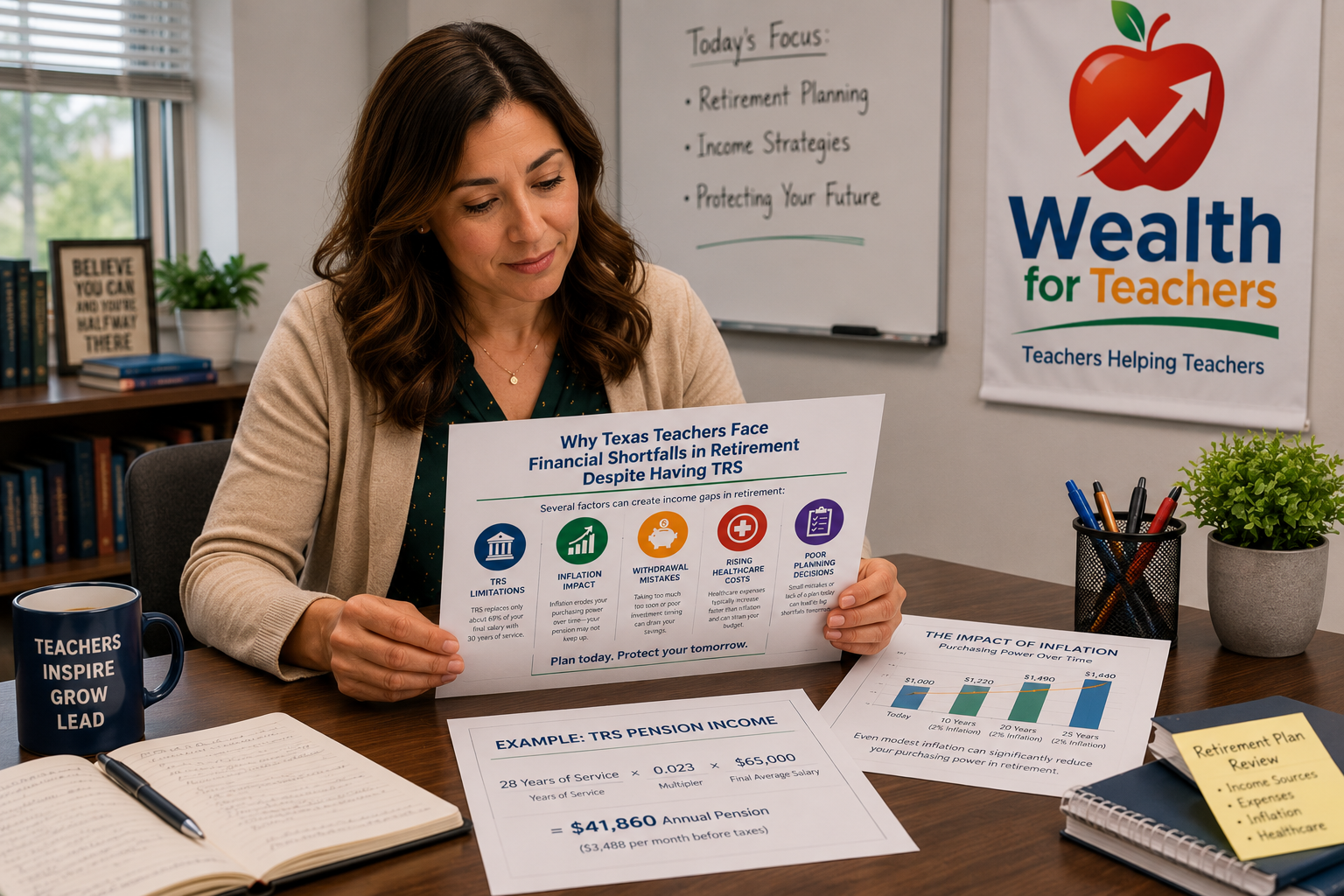

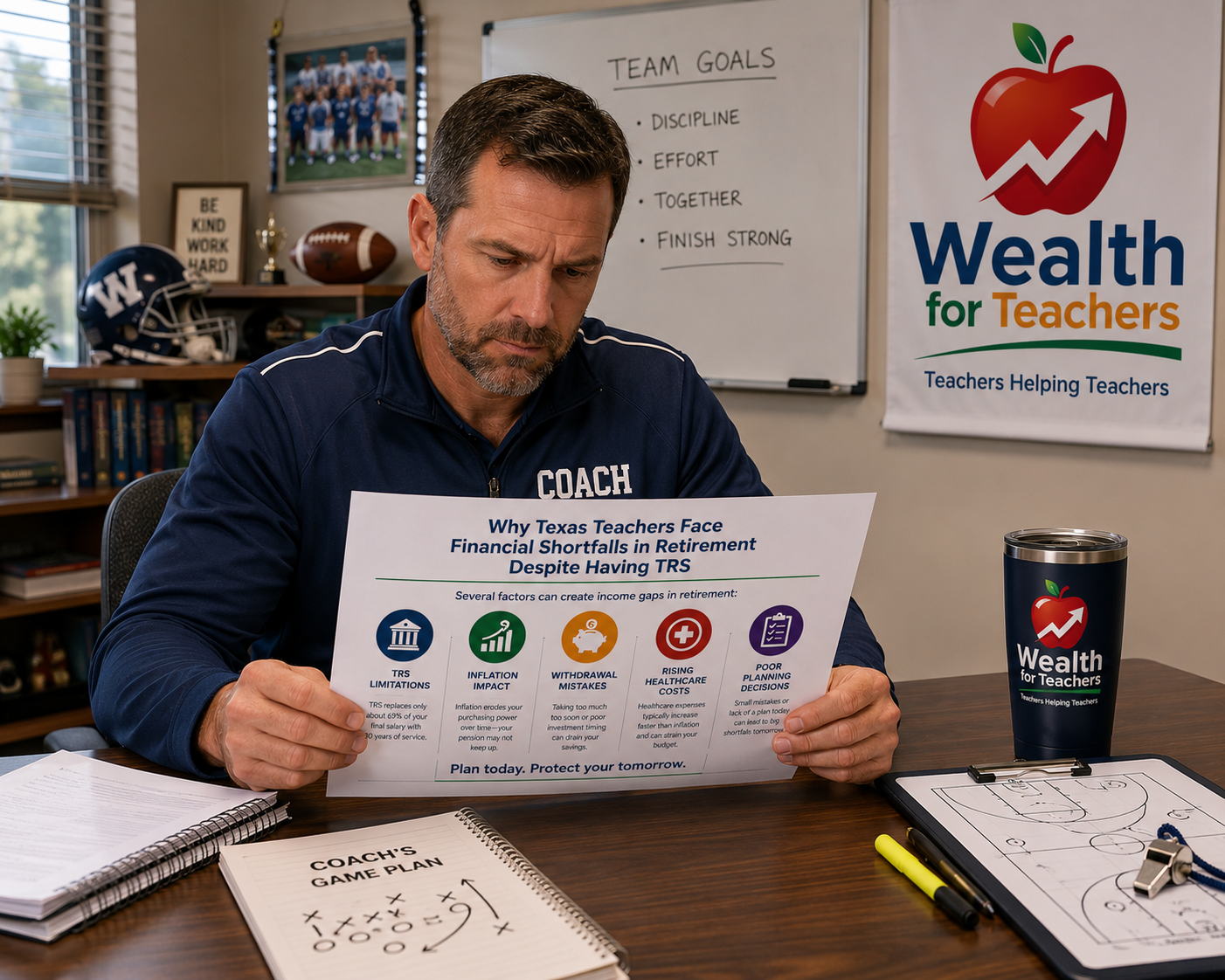

Service credit determines not only your benefit amount but also your eligibility for certain benefits like TRS-Care. Most teachers need at least 20-25 years of service credit to maximize their retirement benefits, though you can retire with full benefits after 30 years of service at any age.

Your TRS retirement benefit is calculated using a formula that considers three main factors: your years of service credit, your final average salary, and a multiplier that varies based on your retirement age and service years.

The basic formula multiplies your service credit years by your final average salary (typically the highest three or five consecutive years) by the applicable multiplier percentage. This calculation ensures that teachers with longer service and higher salaries receive proportionally higher benefits.

The TRS website provides detailed information about benefit calculations and offers online calculators to help you estimate your future retirement benefits based on different scenarios.

Understanding how your benefit is calculated helps you make strategic decisions about when to retire and how to maximize your final average salary through professional development, advanced degrees, or additional responsibilities that increase your compensation.

Smart planning throughout your teaching career can significantly increase your total TRS benefits. Start by understanding how each decision affects your long-term retirement security and develop strategies to optimize your benefits over time.

One key strategy involves timing your highest-earning years to coincide with the period used to calculate your final average salary. Consider pursuing advanced degrees, additional certifications, or leadership roles during the years that will count toward your benefit calculation.

Don’t overlook the importance of keeping your TRS records updated and ensuring you receive credit for all eligible service. This includes military service, out-of-state teaching, and any other qualifying experience that could increase your service credit.

Consider contributing to the Optional Annuity Program to supplement your TRS pension. Even modest contributions can grow significantly over a teaching career, providing additional retirement income beyond your guaranteed pension benefits.

Many teachers make costly mistakes with their TRS benefits due to lack of information or misunderstanding of the rules. Learning what to do instead of these common errors can save you thousands of dollars and ensure optimal retirement security.

Never withdraw your TRS contributions when leaving Texas education unless absolutely necessary. Instead, leave your contributions invested in TRS to maintain your vested benefits and continue earning service credit if you return to teaching. Cashing out early means losing employer contributions and giving up valuable future benefits.

Don’t wait until close to retirement to understand your benefits. Instead, review your annual benefit statements and use TRS online calculators to project your future benefits. Early planning allows you to make strategic decisions about your career and retirement timing.

Don’t underestimate the value of TRS-Care healthcare benefits. Instead of focusing only on your pension amount, consider the total value of your retirement package, including healthcare coverage that could be worth hundreds of thousands of dollars over your retirement years.

Don’t assume you automatically receive credit for all eligible service. Instead, proactively ensure TRS has records of your military service, out-of-state teaching, or other qualifying experience. Missing service credit can significantly reduce your benefits.

Don’t make retirement decisions based on emotions or peer pressure. Instead, carefully analyze your financial situation, benefit projections, and personal goals before deciding when to retire. Consider consulting with financial professionals who understand TRS benefits.

Your TRS pension depends on your years of service credit, final average salary, and age at retirement. The basic formula multiplies your service years by your final average salary by a percentage factor (typically 2.3% per year for most retirees). For example, a teacher with 30 years of service and a $60,000 final average salary would receive approximately $41,400 annually ($60,000 × 30 × 2.3% = $41,400).

You can retire with unreduced TRS benefits when you reach the “Rule of 80” (your age plus service credit years equals 80), have 30 years of service at any age, or reach age 60 with at least 5 years of service. Early retirement before meeting these criteria may result in reduced monthly benefits.

If you’re vested (5+ years of service), you maintain the right to receive TRS benefits at retirement age, even if you leave teaching. Your benefit will be based on your service credit and salary when you left. You can also leave your contributions in TRS and potentially return to teaching later to continue building benefits.

Most Texas teachers don’t pay into Social Security, so they don’t earn Social Security benefits from their teaching service. However, if you worked in other jobs where you paid Social Security taxes, you may be eligible for Social Security benefits alongside your TRS pension. Be aware of potential reductions due to the Windfall Elimination Provision (WEP).

When you become eligible for Medicare at age 65, TRS-Care coordinates with Medicare to provide comprehensive coverage. TRS-Care becomes your secondary coverage, helping pay costs that Medicare doesn’t cover. This coordination ensures you maintain excellent healthcare coverage throughout retirement.

Contributing to OAP can provide valuable additional retirement income to supplement your TRS pension. If you can afford the contributions without financial hardship, OAP offers tax advantages and investment growth potential. Many financial advisors recommend contributing at least enough to maximize any available employer matching, if offered by your district.

TRS provides survivor benefits to protect your family. If you die while actively employed, your designated beneficiaries may receive a lump-sum death benefit and potentially ongoing monthly survivor benefits. The specific benefits depend on your years of service, whether you’re vested, and your family situation.

Yes, TRS allows eligible members to purchase additional service credit for certain types of service, such as military service, out-of-state teaching, or leave of absence periods. Purchasing service credit can increase both your pension benefits and help you reach retirement eligibility sooner, but the cost and benefit should be carefully evaluated.

Understanding your TRS benefits is just the first step. Take control of your retirement planning today by reviewing your current benefit projections and developing a comprehensive strategy for your financial future.

Your years of dedicated service as a Texas educator have earned you valuable TRS benefits that can provide decades of financial security in retirement. By understanding these benefits and making informed decisions throughout your career, you can maximize your retirement income and enjoy the peace of mind that comes from comprehensive retirement planning.

Remember that TRS benefits work best as part of a comprehensive retirement strategy. Consider how your pension, healthcare benefits, and any additional savings work together to support your retirement lifestyle goals. With proper planning and understanding, your TRS benefits can provide the foundation for a secure and comfortable retirement after your rewarding teaching career.

Get Your Free Teacher TRS Calculations

About the Author: LG Canales spent 16 years as a Texas public school teacher before transitioning to financial services. He specializes in helping educators maximize their TRS benefits and build comprehensive retirement strategies. As founder of Outside The Box Financial Group and the Wealth for Teachers division, LG combines his teaching experience with financial expertise to serve the unique needs of Texas educators.