Why Some Teachers Run Out of Money in Retirement (And How to Avoid It)

Running out of money is more common than teachers think. Learn why.

Stable income is the foundation of retirement security. Learn how to build it.

Most Texas teachers discover too late that their TRS pension alone won’t provide the financial security they expected. Even with 30 years of service and a solid final salary, TRS replaces only a portion of your working income. The gap between what you earned and what TRS pays creates a dangerous financial cliff that can derail your entire retirement.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

Building an income floor retirement teachers can rely on requires more than hoping TRS will be enough. It demands a strategic layering approach that combines your guaranteed pension with additional income sources that work together to create true financial security.

The solution isn’t complicated, but it requires understanding how TRS fits into a broader retirement income strategy and taking action while you still have time to build the additional layers you’ll need. Our comprehensive Texas Teacher Retirement Planning Guide covers all the essential components, but this article focuses specifically on creating an income foundation you can count on.

Most retirement plans fail not because teachers don’t save enough, but because they’re never stress-tested against real-world conditions like inflation, market volatility, or unexpected health costs. A proper income floor strategy protects against these risks by creating multiple guaranteed income streams that work independently of market performance.

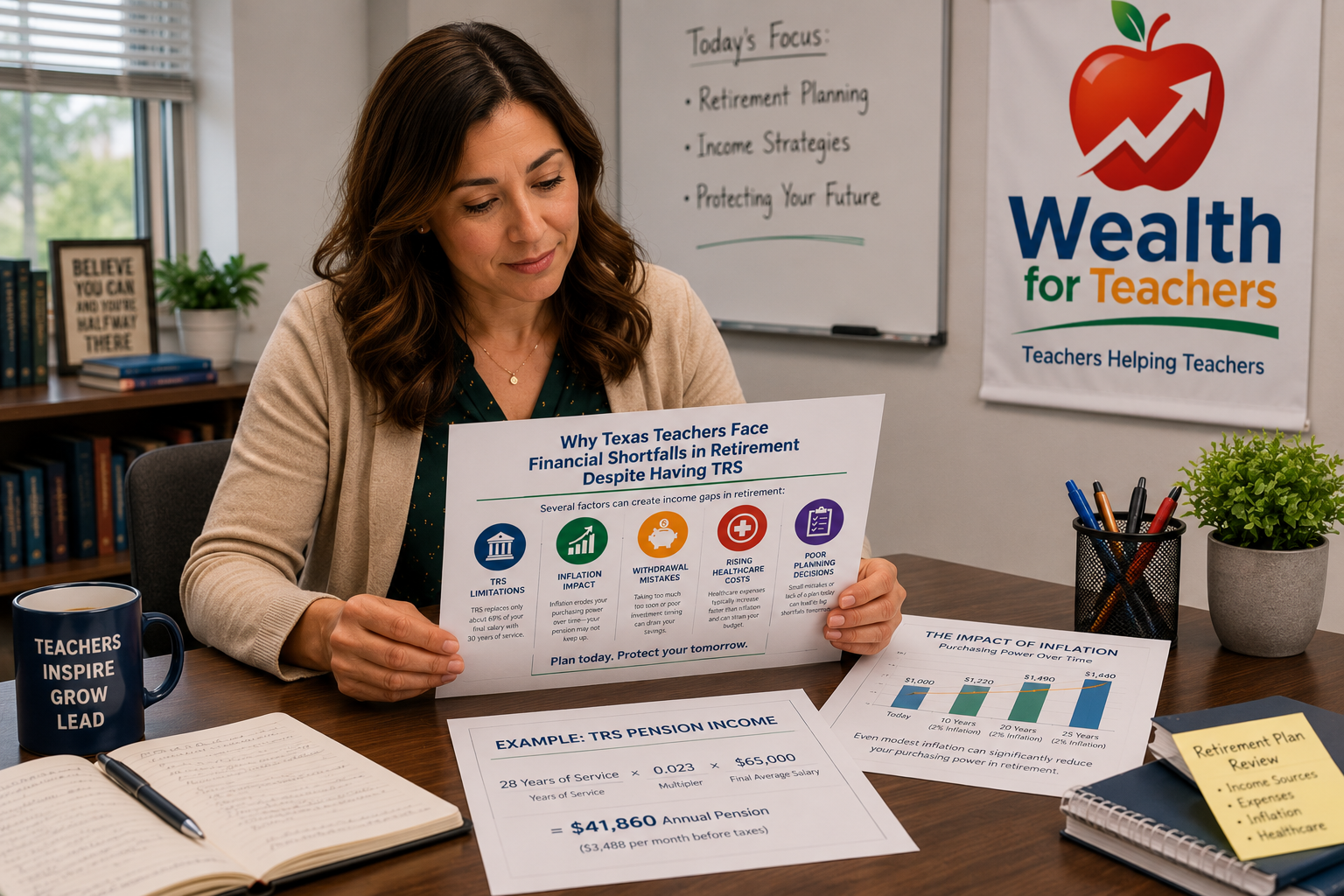

Your TRS pension forms the base of your income floor, but understanding its limitations is crucial for proper retirement planning. Texas TRS uses a straightforward formula: Annual Pension = (Years of Service × 0.023) × Final Average Salary.

Use the TRS calculator to estimate your pension and identify potential income gaps.

A teacher with 30 years of service and a final average salary of $65,000 would receive an annual TRS pension of $44,850. While this provides a solid foundation, it represents only about 69% of their working income, creating a significant gap that must be filled by other sources.

TRS provides several advantages as part of your income floor:

However, TRS alone rarely provides enough income to maintain your pre-retirement lifestyle. The gap between your TRS pension and your actual income needs must be filled through strategic planning with additional guaranteed income sources.

Building a reliable income floor retirement teachers can depend on requires three distinct layers that work together to eliminate financial uncertainty.

Your TRS pension serves as the foundation because it’s guaranteed and requires no investment decisions on your part. This layer handles your basic living expenses and provides the security that allows you to be more strategic with additional income sources.

This layer fills the gap between your TRS pension and your total income needs. The most reliable options include immediate annuities, deferred income annuities, or other guaranteed income products that provide predictable monthly payments regardless of market conditions.

The third layer provides flexibility and growth potential through systematic withdrawals from retirement accounts, part-time work, or other variable income sources. This layer can adjust based on your needs and market conditions while the first two layers provide stability.

Each layer serves a specific purpose, and together they create an income system that’s both stable and adaptable. The key is sizing each layer appropriately based on your specific situation and income replacement needs.

Many teachers wonder whether they need additional guaranteed income when they already have a pension. The answer depends on whether your TRS pension alone meets your income replacement goals and provides adequate protection against inflation over a 20-30 year retirement.

Guaranteed income strategies through annuities work particularly well alongside TRS because they operate independently of your pension. If TRS faces future funding challenges or reduces cost-of-living adjustments, your annuity income continues unaffected.

Consider a teacher who needs $5,000 monthly in retirement but expects only $3,500 from TRS. A deferred income annuity purchased during their working years could provide the additional $1,500 monthly, creating a complete guaranteed income floor of $5,000.

The timing of annuity purchases matters significantly. Starting earlier allows for smaller contributions that grow over time, while waiting until retirement requires larger lump-sum purchases. Teachers who begin building their income floor strategy in their 40s or 50s have more options and better outcomes than those who wait until retirement approaches.

Not all annuities are appropriate for teachers with TRS pensions. The most effective options focus on income certainty rather than complex features:

Variable and indexed annuities may seem attractive due to growth potential, but they add complexity and market risk that undermines the purpose of building a guaranteed income floor.

Creating an effective income floor requires understanding when each income source begins and how they coordinate throughout your retirement. Your TRS pension starts when you retire and meet eligibility requirements, but other income sources can be timed to optimize your overall strategy.

Consider this timeline approach:

Strategic use of annuities can fill gaps in this timeline or provide additional income when your expenses are highest. For example, a deferred annuity could provide extra income from age 60-67 to bridge the gap until full Social Security benefits begin.

Teachers who understand this timeline can make better decisions about when to retire from TRS and how to structure their additional guaranteed income sources. The goal is ensuring adequate income throughout every phase of retirement, not just the early years.

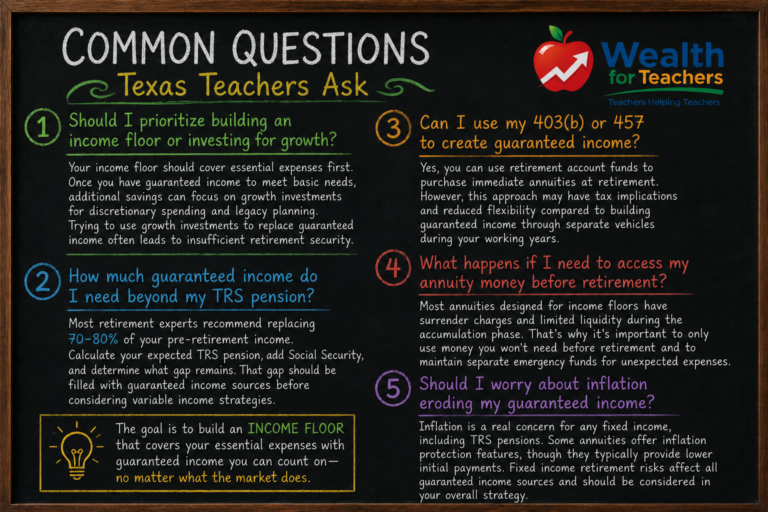

Your income floor should cover essential expenses first. Once you have guaranteed income to meet basic needs, additional savings can focus on growth investments for discretionary spending and legacy planning. Trying to use growth investments to replace guaranteed income often leads to insufficient retirement security.

Most retirement experts recommend replacing 70-80% of your pre-retirement income. Calculate your expected TRS pension, add Social Security, and determine what gap remains. That gap should be filled with guaranteed income sources before considering variable income strategies.

Yes, you can use retirement account funds to purchase immediate annuities at retirement. However, this approach may have tax implications and reduced flexibility compared to building guaranteed income through separate vehicles during your working years.

Most annuities designed for income floors have surrender charges and limited liquidity during the accumulation phase. That’s why it’s important to only use money you won’t need before retirement and to maintain separate emergency funds for unexpected expenses.

Inflation is a real concern for any fixed income, including TRS pensions. Some annuities offer inflation protection features, though they typically provide lower initial payments. Fixed income retirement risks affect all guaranteed income sources and should be considered in your overall strategy.

Rather than hoping your TRS pension will be sufficient or trying to replace guaranteed income with investment returns, build your retirement security systematically through a layered approach.

Start by calculating your actual income replacement needs. Determine what your TRS pension will provide using the formula: (Years of Service × 0.023) × Final Average Salary. Add your expected Social Security benefits. The remaining gap represents your guaranteed income need that must be filled through additional sources.

Focus on building your income floor first before pursuing growth investments. Multiple retirement income streams provide security, but they should complement rather than replace guaranteed income for your essential expenses.

Consider starting your income floor strategy early in your career when time allows for smaller contributions to grow into larger income streams. Teachers who wait until their 50s or later face higher costs and fewer options for building adequate guaranteed income.

Work with professionals who understand both TRS benefits and guaranteed income products. The coordination between these different income sources requires expertise that general financial advisors may not possess.

Every teacher’s situation is different, but most fall into one of these decision paths:

You have maximum time to build guaranteed income through deferred annuities or other long-term strategies. Focus on small, consistent contributions that will grow into significant income streams. Consider this path if you’re confident in your teaching career trajectory and want to lock in future income at today’s rates.

What could go wrong: Starting too aggressive with contributions that strain your current budget or choosing products with excessive fees that erode long-term returns.

You need to balance current financial obligations with retirement preparation. Calculate your projected TRS pension and determine whether additional guaranteed income is necessary. This often involves moderate annuity contributions or other guaranteed income products.

What could go wrong: Underestimating your income replacement needs or assuming TRS and Social Security will be sufficient without running actual numbers.

Time is limited, so efficiency matters. Focus on immediate or short-term deferred annuities that begin providing income soon after retirement. You may need larger contributions to achieve adequate income replacement.

What could go wrong: Panicking and making rushed decisions, or conversely, assuming it’s too late to build additional guaranteed income and giving up on proper planning.

If you have substantial savings beyond TRS, you might use systematic withdrawal strategies rather than guaranteed income products. However, consider whether market volatility could affect your essential expenses and whether some guaranteed income provides peace of mind.

What could go wrong: Overestimating your risk tolerance in retirement or failing to protect essential expenses from market downturns through appropriate withdrawal strategies.

If you plan to work after retirement, your guaranteed income needs may be lower initially. However, consider what happens if health issues or other factors prevent continued work. Part-time work strategies should complement rather than replace guaranteed income planning.

What could go wrong: Overestimating your ability or desire to continue working, or failing to plan for the transition when work income eventually ends.

Use these diagnostic questions to identify potential gaps in your retirement income planning:

If you answered “no” or “I’m not sure” to any of these questions, your retirement income strategy needs additional development before you make final retirement decisions.

Most teachers discover significant gaps in their retirement planning only after it’s too late to make meaningful changes. TRS provides excellent benefits, but it’s designed as part of a three-legged stool that includes Social Security and personal savings. Without proper coordination between all income sources, even long-term teachers can face financial uncertainty in retirement.

The key is testing your assumptions and running real numbers before making irreversible retirement decisions. Required minimum distribution planning and other advanced strategies become much more important when you don’t have adequate guaranteed income to cover your basic needs.

Building an effective income floor retirement teachers can depend on requires understanding both the strengths and limitations of your TRS pension, then strategically adding guaranteed income sources to create true financial security. The earlier you start this process, the more options you’ll have and the better your outcomes will be.

Don’t wait until retirement approaches to discover whether your income plan actually works. Start building your guaranteed income floor now while you still have time to make adjustments and create the financial security you deserve.

Get Your TRS Analysis

Use the TRS calculator to estimate your pension and identify potential income gaps.

Running out of money is more common than teachers think. Learn why.

TRS is only one income source. Learn how teachers can build multiple retirement income streams.