Why Some Teachers Run Out of Money in Retirement (And How to Avoid It)

Running out of money is more common than teachers think. Learn why.

TRS is only one income source. Learn how teachers can build multiple retirement income streams.

Your TRS pension forms the foundation of your retirement, but depending solely on it creates dangerous income shortfalls that compound over decades. Smart retirement income streams teachers build involve layering multiple sources to protect against inflation, market changes, and unexpected expenses that a fixed pension cannot handle alone.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

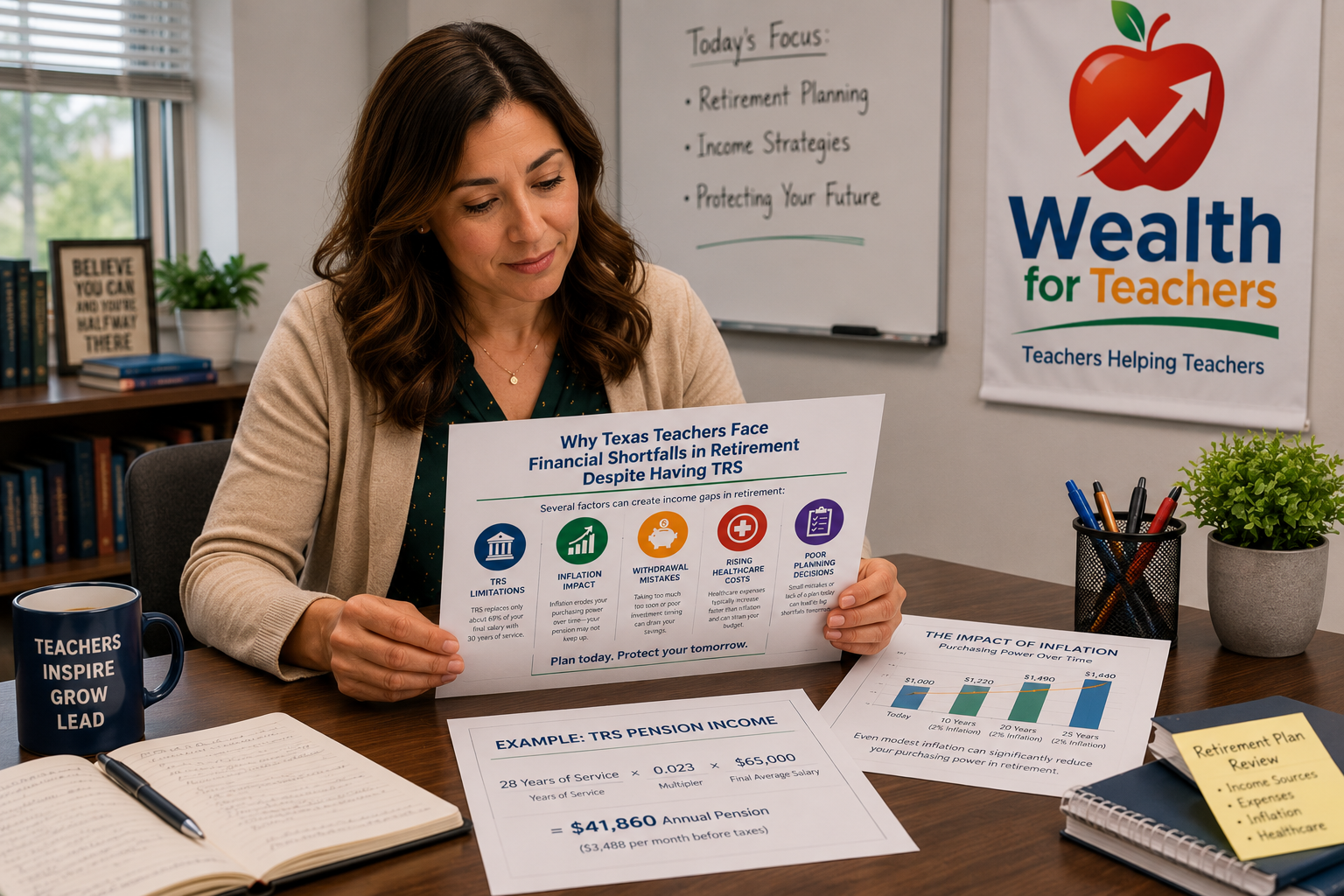

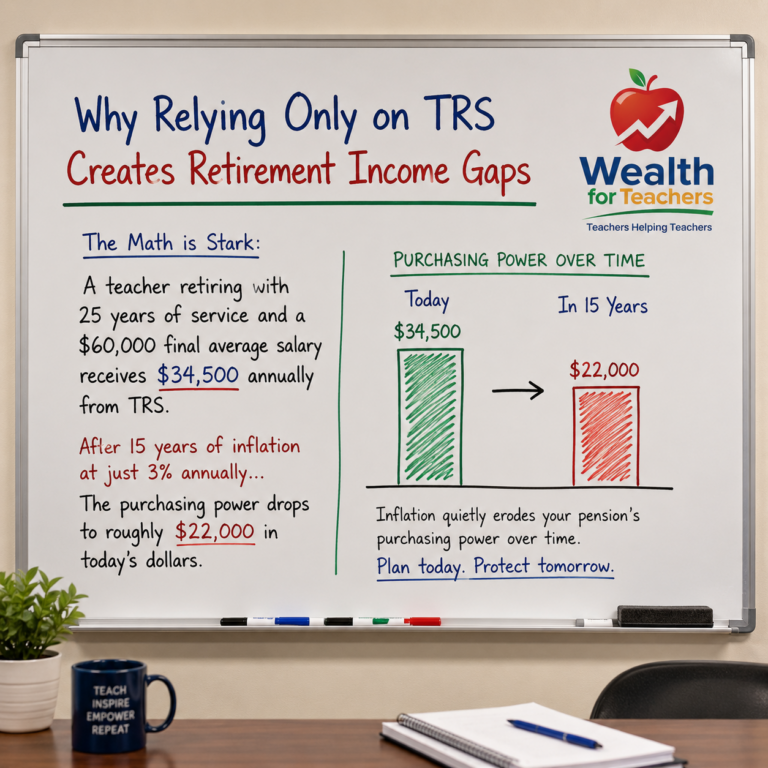

The math is stark. A teacher retiring with 25 years of service and a $60,000 final average salary receives $34,500 annually from TRS (25 × 0.023 × $60,000). That may sound adequate today, but after 15 years of inflation at just 3% annually, the purchasing power drops to roughly $22,000 in today’s dollars.

Building retirement income streams beyond TRS is not about getting rich—it is about maintaining your standard of living and protecting against risks that your pension alone cannot address. The key lies in understanding how different income sources work together, when to use each one, and how to coordinate withdrawals for maximum efficiency. Our comprehensive Texas Teacher Retirement Planning Guide breaks down these strategies in detail.

Most retirement plans fail because they rely on assumptions that sound reasonable on paper but crumble under real-world pressures like medical emergencies, family obligations, or economic downturns. Testing your income strategy before you need it reveals gaps that are fixable today but catastrophic tomorrow.

Effective retirement income streams teachers can build rest on four distinct pillars, each serving a specific purpose in your overall strategy. Understanding their roles prevents over-reliance on any single source.

Use the TRS calculator to estimate your pension and identify potential income gaps.

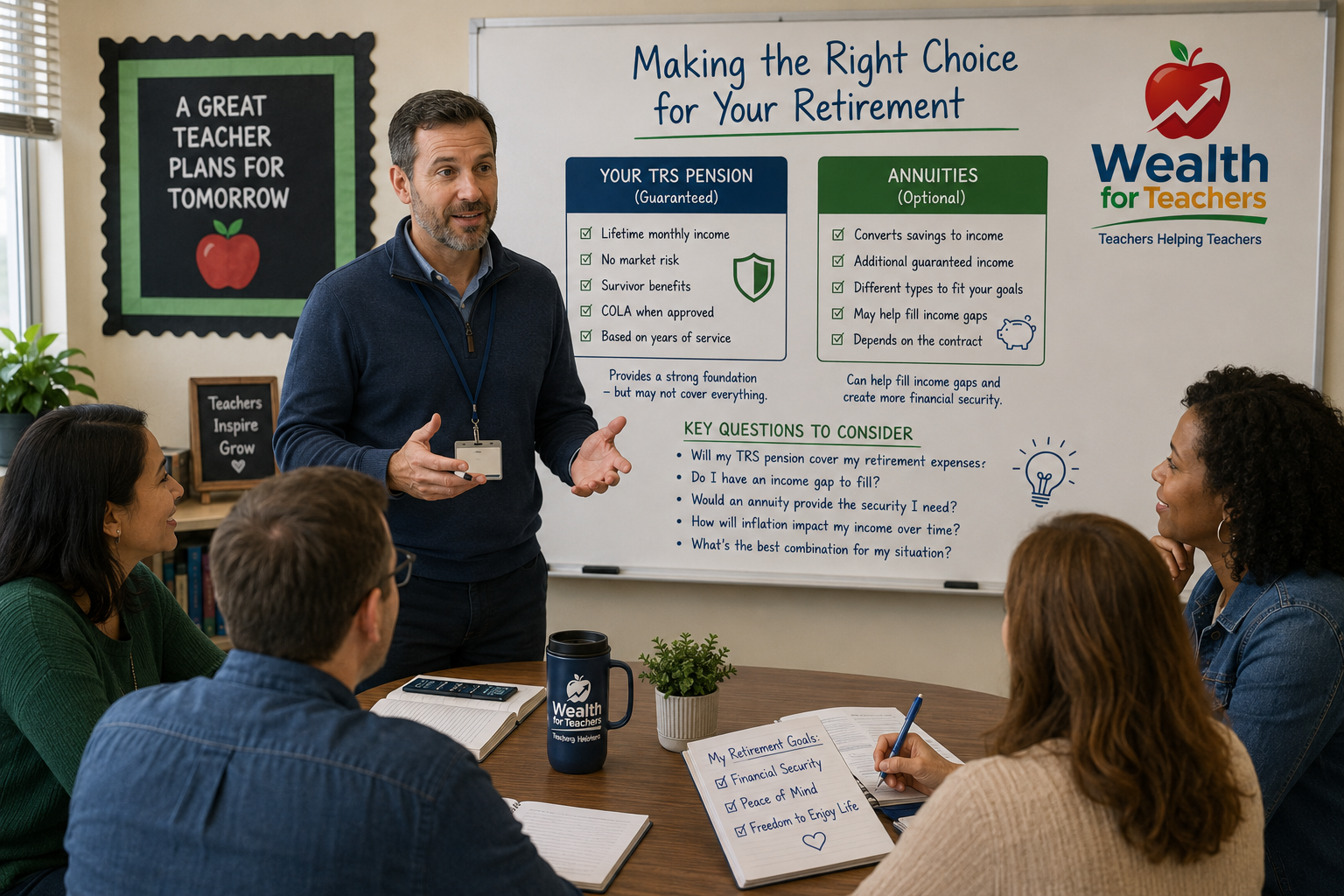

Your Texas TRS pension provides predictable monthly income calculated using the formula: Years of Service × 0.023 × Final Average Salary. This foundation supports basic living expenses but comes with limitations that require other income sources to address.

The pension does not adjust for inflation automatically, and you cannot increase payments if unexpected expenses arise. Additionally, survivor benefits may reduce payments significantly, leaving a surviving spouse with insufficient income if not properly planned around.

Your school district’s 403(b) plan allows tax-deferred contributions that grow without annual tax drag. These accounts provide flexibility that your pension lacks—you control withdrawal timing, amounts, and investment allocation throughout retirement.

The key advantage lies in tax management. You can withdraw smaller amounts in low-income years and larger amounts when needed, managing your tax bracket more effectively than relying solely on pension income.

Individual Retirement Accounts, whether traditional or Roth, give you complete control over investment choices and withdrawal strategies. Roth IRAs provide tax-free growth and withdrawals, while traditional IRAs offer current tax deductions with future taxable withdrawals.

This flexibility becomes crucial when coordinating with your TRS pension timing. You might delay TRS to increase your pension multiplier while living off IRA withdrawals, or use Roth conversions during lower-income periods to reduce future tax burdens.

Properly structured IUL policies provide tax-free retirement income through policy loans while maintaining a death benefit. The cash value grows based on market index performance with downside protection, creating potential for tax-free income that does not count toward provisional income for Social Security taxation.

This income source works particularly well for teachers who expect to be in higher tax brackets during retirement or want to supplement inflation-protected income without increasing taxable income.

Building effective retirement income streams teachers can rely on requires strategic layering, not just accumulation. Each source should address specific risks and complement the others rather than simply adding more money to the total.

Your TRS pension provides guaranteed income but lacks inflation protection and flexibility. Market-based accounts like 403(b)s and IRAs offer growth potential and withdrawal control but carry market risk. Insurance products provide guarantees and tax benefits but with different liquidity and growth characteristics.

Layering these sources means you are not dependent on any single economic condition. Market downturns affect your investment accounts but not your pension. Inflation erodes your pension’s purchasing power but potentially increases your market account values. Interest rate changes affect different accounts differently.

The most critical element involves timing when each income source activates. You might use IRA or 403(b) withdrawals to bridge the gap if you retire before becoming eligible for full TRS benefits. This strategy preserves your pension multiplier while providing needed income.

Alternatively, you could delay Social Security while using other income sources, increasing your eventual Social Security benefit by 8% per year until age 70. The decision to delay Social Security depends heavily on your other income sources and life expectancy expectations.

Smart tax management separates successful retirement income strategies from those that leave money on the table year after year. Understanding how different withdrawals affect your tax situation enables you to keep more of what you have saved.

Your TRS pension creates a tax floor—a baseline taxable income you receive regardless of other decisions. Additional withdrawals from traditional 401(k)s or IRAs add to this base, potentially pushing you into higher tax brackets or triggering additional Medicare premiums.

Strategic withdrawal sequencing can minimize these impacts. You might withdraw from Roth accounts during high-expense years to avoid bracket jumps, or take larger traditional IRA withdrawals in low-expense years to fill lower tax brackets efficiently.

Combined income from your TRS pension, traditional retirement account withdrawals, and other sources affects how much of your Social Security benefit becomes taxable. Understanding this interaction prevents unpleasant surprises and enables better planning.

Tax-free income from Roth accounts or IUL policy loans does not count toward provisional income for Social Security taxation purposes, making these sources valuable for managing overall tax liability in retirement.

Practical examples illustrate how retirement income streams teachers build work together to create sustainable retirement income that addresses real-world needs and challenges.

Sarah retires with 30 years of TRS service and a $65,000 final average salary. Her TRS pension provides $44,850 annually (30 × 0.023 × $65,000). She has $350,000 in her 403(b), $180,000 in a Roth IRA, and a structured IUL policy designed to provide $15,000 annually in tax-free income starting at age 65.

Her income strategy layers these sources: TRS pension covers basic expenses, systematic 403(b) withdrawals provide inflation protection and flexibility, Roth IRA withdrawals remain available for unexpected expenses without tax consequences, and IUL policy loans supplement income without affecting Social Security taxation.

Total projected annual income reaches approximately $75,000, with tax diversification that provides flexibility to manage brackets and unexpected expenses throughout retirement.

Michael plans to retire at 58 with 28 years of service but wants to wait until 62 to begin drawing his TRS pension to maximize the multiplier effect. His strategy involves living off 403(b) and IRA withdrawals for four years while his TRS benefit continues growing.

By delaying TRS, he increases his eventual pension while creating space for Roth conversions during the lower-income bridge period. This strategy requires careful planning to ensure sufficient funds in accessible accounts but can significantly improve long-term income and tax efficiency.

Understanding safe withdrawal rates becomes critical for this strategy, as over-withdrawal during the bridge period could jeopardize the entire plan.

Moving beyond TRS-only retirement requires a systematic approach that builds income diversification while you are still working and can make regular contributions to alternative accounts.

If your district offers 403(b) matching contributions, maximize this free money first. Even a small match represents guaranteed returns that compound over decades of service. Choose low-cost index funds within the plan to minimize fees that erode returns over time.

Focus on consistency rather than trying to time markets or pick winning investments. Regular contributions during your working years create the foundation for flexible retirement income that complements your TRS pension.

Roth IRA contributions provide tax-free growth and withdrawals in retirement, creating valuable tax diversification against your TRS pension and traditional 403(b) income. The annual contribution limits require consistent funding over many years to build substantial balances.

Young teachers particularly benefit from Roth accounts because decades of tax-free growth can create significant retirement income. Even teachers closer to retirement can benefit from tax-free income sources that do not affect Social Security taxation or Medicare premium calculations.

Index Universal Life insurance policies can provide tax-free retirement income through policy loans while maintaining death benefits for survivors. These policies require careful structuring and understanding of costs, but they offer unique benefits for teachers in higher tax brackets or those wanting additional tax-free income sources.

The key lies in working with professionals who understand the specific rules and optimal structuring for retirement income rather than just buying life insurance with a cash value component.

Should I prioritize my 403(b) or a Roth IRA first?

Start with any employer match in your 403(b), then consider Roth IRA contributions for tax diversification. The order depends on your current tax bracket, expected retirement tax bracket, and available investment options in each account type.

How much should I withdraw from each account in retirement?

Your withdrawal strategy should consider your tax bracket, required minimum distributions, Social Security taxation, and cash flow needs. Start with a baseline from your TRS pension, then layer other sources to minimize taxes and maintain desired spending.

Can I use retirement accounts to bridge early retirement before TRS eligibility?

Yes, but you need sufficient balances and a clear withdrawal strategy. IRA withdrawals after age 59½ avoid early withdrawal penalties, and 403(b) plans may allow penalty-free withdrawals at age 55 if you separate from service. Understanding these rules prevents costly mistakes.

Does my TRS pension affect Social Security benefits?

Texas teachers pay into Social Security, so your TRS pension does not reduce Social Security benefits through the Government Pension Offset. However, combined income from TRS and other sources may make more of your Social Security taxable.

Should I consider annuities for additional guaranteed income?

Annuities can provide additional guaranteed income, but you already have significant guaranteed income through TRS. Before adding more guarantees, consider whether you need more flexibility, inflation protection, or tax diversification instead. Guaranteed income strategies require careful evaluation of costs versus benefits.

Your retirement income strategy depends on your specific circumstances, timeline, and goals. These decision paths help you identify which approach fits your situation best.

Choose this path if you prioritize predictable income over growth potential and have 10+ years until retirement. Focus on maximizing your TRS pension through additional service years, building substantial 403(b) balances through consistent contributions, and adding fixed annuities for extra guaranteed income.

Risks include insufficient inflation protection and limited flexibility for unexpected expenses. This approach works best for teachers with modest living expenses and strong family health histories.

This path combines guaranteed income with growth potential and tax diversification. Build your TRS foundation while maximizing 403(b) contributions to diversified index funds, funding Roth IRAs for tax-free income, and considering structured life insurance for additional tax-free retirement income.

This strategy provides flexibility to adjust withdrawals based on market conditions and personal needs while maintaining a guaranteed income base. It requires more active management but offers better inflation protection and tax efficiency.

If you want to retire before full TRS eligibility, focus on building substantial balances in accessible accounts. Maximize 403(b) and IRA contributions, understand penalty-free withdrawal rules, and plan bridge strategies to maintain income while optimizing your eventual TRS benefit.

This path requires careful planning around withdrawal rules and tax implications. Mistakes can be costly through penalties or suboptimal tax management. Consider whether part-time work after retirement might supplement income more efficiently than depleting savings early.

Teachers with higher salaries should focus heavily on tax diversification through Roth accounts and structured life insurance. Current high tax brackets make traditional 403(b) contributions valuable, but Roth conversions during early retirement and tax-free income sources become critical for long-term efficiency.

This strategy requires sophisticated tax planning and potentially higher contribution levels across multiple account types. Working with tax professionals helps optimize timing and account selection.

These diagnostic questions reveal gaps or uncertainties in your retirement income planning that require attention before making final decisions.

Do you know your projected TRS pension amount and when you will be eligible for full benefits? If not, request a benefit estimate from TRS and understand the impact of retiring at different ages on your monthly payment.

Have you calculated how much additional monthly income you will need beyond your TRS pension to maintain your desired lifestyle? Without this baseline, you cannot determine how much to save in other accounts or which withdrawal strategies make sense.

Do you understand how your retirement account withdrawals will affect your taxes and Social Security benefits? Poor withdrawal coordination can cost thousands annually through higher tax brackets and Medicare premiums.

Have you tested your retirement plan under different scenarios like market downturns, inflation, or unexpected health expenses? Plans that work under normal conditions often fail during stress periods that are inevitable over 20-30 year retirements.

Do you have a clear timeline for when to start each income source and how much to withdraw annually? Without specific implementation plans, even good retirement savings can be poorly managed and underperform expectations.

The most common mistake teachers make involves assuming their current retirement strategy will work without testing it under realistic conditions. Inflation erodes fixed pension buying power over decades, market downturns can devastate poorly-timed withdrawals, and unexpected expenses can derail even well-funded plans.

Teachers who wait until within five years of retirement to seriously evaluate their income strategy discover gaps when options for addressing them are limited and expensive. The strategies that work require years of implementation through consistent contributions and proper structuring.

Get Your TRS Analysis

Understanding how your current trajectory aligns with your retirement goals requires personalized analysis of your specific situation, timeline, and objectives. Professional evaluation reveals gaps while there is still time to address them and optimizes strategies you may be using incorrectly.

Use the TRS calculator to estimate your pension and identify potential income gaps.