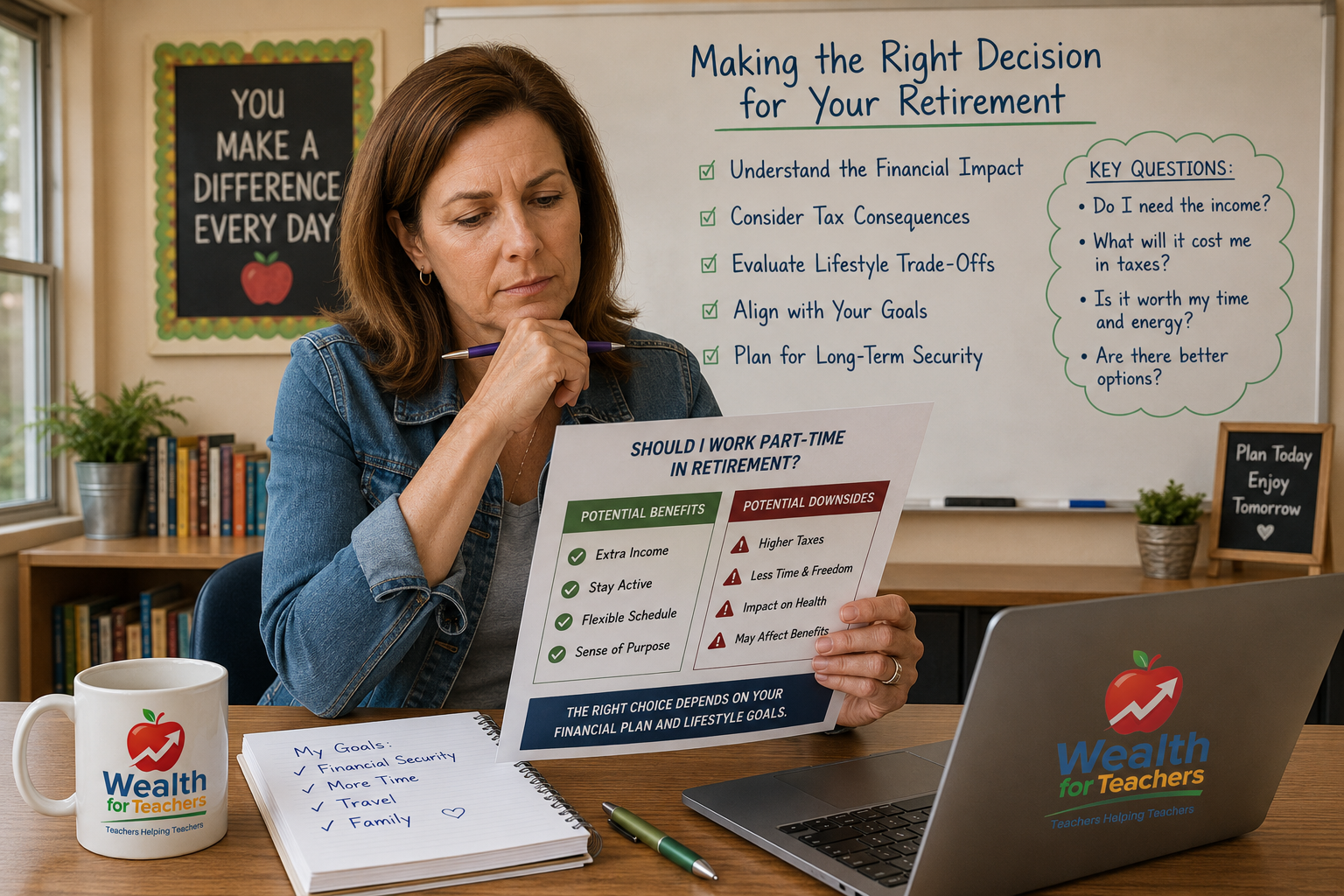

Should Teachers Work Part-Time After Retirement? (Is It Worth It?)

Part-time work can boost income—but is it the right choice?

Guaranteed income can reduce risk—but it’s not always right.

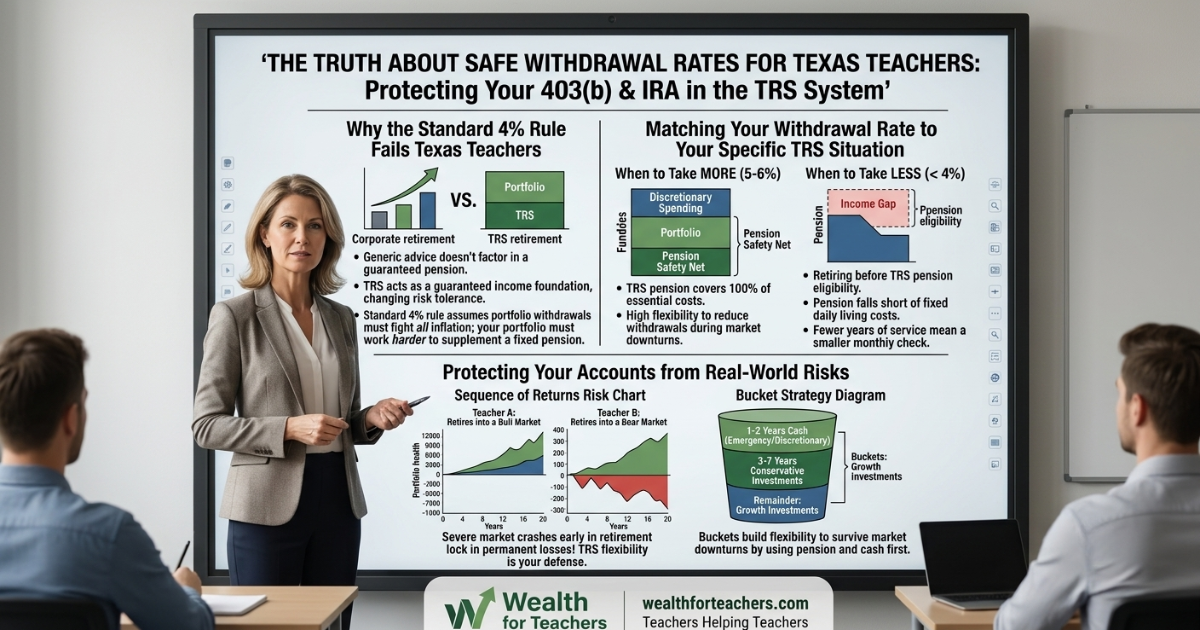

Texas teachers often discover too late that relying solely on TRS pension payments creates significant income gaps in retirement. The decision between adding annuities or maximizing guaranteed income strategies becomes critical when you realize your TRS pension may not cover your actual living expenses.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

Understanding the real difference between annuity vs pension teachers face requires looking beyond simple monthly payment comparisons. The choice affects your financial flexibility, inflation protection, and ability to handle unexpected expenses throughout retirement.

Most teachers assume their TRS pension provides enough guaranteed income security. However, the reality is more complex. Your pension calculation using the 2.3% multiplier may seem straightforward, but it doesn’t account for rising costs, healthcare expenses, or the need for additional income streams.

The Texas Teacher Retirement Planning Guide reveals that successful teacher retirement plans combine multiple guaranteed income sources rather than depending on a single payment stream.

Most retirement plans fail because they are never tested under real-world conditions. Teachers often create plans based on best-case scenarios without considering inflation, healthcare costs, or market volatility that could derail their financial security.

Your Texas TRS pension provides a guaranteed monthly payment calculated as: Annual Pension = (Years of Service × 0.023) × Final Average Salary. This creates a predictable income foundation that continues for life.

Use the TRS calculator to estimate your pension and identify potential income gaps.

For example, a teacher with 30 years of service and a $65,000 final average salary receives: 30 × 0.023 × $65,000 = $44,850 annually, or $3,738 monthly.

This guaranteed payment offers several advantages:

However, your TRS pension also has limitations that create potential income gaps. The payment amount is fixed based on your service and salary, regardless of your actual retirement expenses. How inflation quietly reduces your TRS pension over time becomes a critical factor in long-term financial planning.

Your TRS pension typically replaces 60-70% of your pre-retirement income if you work a full career. This replacement ratio assumes your expenses decrease in retirement, but many teachers find their costs remain steady or increase due to:

The gap between your TRS pension and actual expenses creates the need for additional guaranteed income sources.

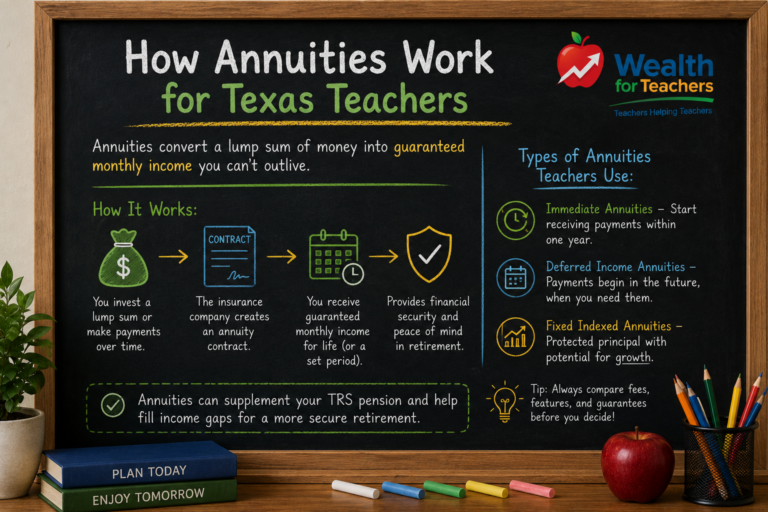

Annuities function as private pension contracts that convert a lump sum payment into guaranteed monthly income. For teachers, annuities can supplement TRS pension payments by providing additional predictable income streams.

The most relevant annuity types for teachers include:

You make a single premium payment and begin receiving monthly payments within one year. This works well for teachers who want to convert 403(b) or 457(b) savings into guaranteed income at retirement.

You pay premiums now but delay income payments until a future date. Teachers often use these to create guaranteed income that begins when TRS pension payments start, filling specific income gaps.

These provide guaranteed minimum returns with potential for higher returns based on market index performance. The principal is protected while offering some inflation protection through market participation.

Your payments fluctuate based on underlying investment performance. While these offer growth potential, they eliminate the guaranteed income certainty that teachers typically seek.

Annuities become valuable for Texas teachers in specific situations where guaranteed income fills critical gaps that TRS pension alone cannot address.

Teachers who retire before being eligible for full TRS benefits often need guaranteed income to bridge the gap. An annuity can provide monthly payments from early retirement until TRS pension payments begin.

Consider a teacher who retires at 60 with 25 years of service but must wait until 65 for unreduced TRS benefits. An annuity funded with 403(b) savings can provide guaranteed income during those five years.

Teachers with shorter careers or lower final average salaries may receive TRS pensions that fall short of their income needs. The biggest retirement income gaps teachers don’t see coming often affect educators who changed careers or took time off for family reasons.

An annuity can supplement a smaller TRS pension to reach your target retirement income level.

TRS cost-of-living adjustments are not guaranteed and depend on legislative approval. Annuities with inflation protection riders can provide income that automatically increases with rising costs, protecting your purchasing power over time.

Healthcare costs typically increase faster than general inflation. An annuity specifically designed to cover rising healthcare premiums ensures you can maintain insurance coverage without straining your budget.

Many Texas teachers find their TRS pension provides sufficient guaranteed income without needing additional annuities. This typically occurs when:

Teachers with 30+ years of service and higher final average salaries often find their TRS pension meets their guaranteed income needs. Additional retirement savings can remain invested for growth rather than converted to annuity payments.

Keeping retirement savings invested instead of purchasing annuities maintains flexibility for unexpected expenses, legacy planning, and potential long-term care needs. Your 403(b) and 457(b) accounts provide access to funds that annuities typically do not offer.

Both TRS pensions and annuities carry costs that affect your actual retirement income. Understanding these costs prevents surprises that could derail your financial plan.

These costs compound over time and significantly impact your total retirement income. Why a fixed pension can create hidden retirement risks for teachers becomes particularly relevant when considering the total cost of guaranteed income strategies.

Sarah, a 58-year-old Texas teacher with 28 years of service, wants to retire early. Her TRS pension at 58 would be reduced, but she could receive full benefits at 65.

Strategy: Sarah uses $200,000 from her 403(b) to purchase a seven-year immediate annuity providing $2,400 monthly. This bridges her income gap until full TRS pension begins at 65.

Result: Sarah maintains her desired lifestyle during early retirement without permanently reducing her TRS pension benefits.

Mike taught for 22 years with a $58,000 final average salary. His TRS pension calculation: 22 × 0.023 × $58,000 = $29,348 annually, or $2,446 monthly.

This pension falls short of his $4,000 monthly income target. Mike uses $300,000 in retirement savings to purchase an immediate annuity providing an additional $1,600 monthly.

Result: Mike combines TRS pension ($2,446) plus annuity payments ($1,600) to reach his $4,046 monthly income goal.

No. Your TRS account provides a pension, not a lump sum for annuity purchases. You can use 403(b), 457(b), or other retirement savings to buy annuities that supplement your TRS pension.

Delaying Social Security typically provides better returns than annuity purchases. Should teachers delay Social Security often becomes a more valuable strategy than purchasing additional annuities.

This depends on your annuity contract terms. Some annuities provide death benefits to beneficiaries, while others cease payments upon death. Period certain and joint-and-survivor options provide more protection for heirs.

Some annuities offer inflation protection riders, but these typically cost 0.5% to 1.5% annually in fees. TRS occasionally provides cost-of-living adjustments without additional fees, but these are not guaranteed.

No. Converting all savings to annuities eliminates flexibility for unexpected expenses, healthcare costs, and legacy planning. Most teachers benefit from combining guaranteed income with invested assets.

Rather than viewing this as an either-or decision, successful teacher retirement planning combines your TRS pension with strategic guaranteed income supplements where needed.

Determine your real retirement expenses, including healthcare, housing, and lifestyle costs. Compare this to your projected TRS pension to identify any income gaps.

Teachers comfortable with some investment risk may prefer keeping retirement savings invested rather than purchasing annuities. Those wanting maximum income certainty may benefit from annuity supplements.

The timing of guaranteed income purchases affects your total retirement income. What is a safe withdrawal rate for teachers in retirement can help determine when to convert investments to guaranteed income.

Model different combinations of TRS pension, Social Security, annuities, and investment withdrawals to find the optimal mix for your situation.

If you have 30+ years of service and a TRS pension exceeding $3,500 monthly, you may not need annuities. Your guaranteed income likely covers basic expenses, allowing other savings to remain invested for growth and flexibility.

Consider annuities only for specific purposes like healthcare cost inflation or leaving a guaranteed income stream for your spouse.

Teachers receiving TRS pensions below $2,500 monthly often benefit from annuity supplements. Use retirement savings to purchase immediate annuities that fill the gap between your pension and income needs.

Focus on low-cost immediate annuities rather than complex products with high fees and multiple riders.

Teachers retiring before full TRS pension eligibility can use annuities to bridge income gaps. Purchase temporary annuities that provide payments until your full TRS benefits begin.

This strategy works best when early retirement is planned and you have sufficient retirement savings to fund the bridge period.

Teachers concerned about rising healthcare costs may benefit from annuities specifically designed to increase payments for medical expenses. These products provide inflation protection for healthcare costs that typically exceed general inflation rates.

Evaluate whether the additional cost provides sufficient value compared to keeping savings invested and withdrawing as needed for healthcare expenses.

Teachers whose spouses will receive reduced TRS survivor benefits may use annuities to provide guaranteed income continuation. Joint-and-survivor annuities ensure your spouse maintains adequate income after your death.

Compare annuity survivor benefits to TRS survivor options and life insurance alternatives to determine the most cost-effective protection.

Answer these questions to identify potential gaps or uncertainty in your retirement income plan:

If you cannot calculate your specific TRS pension using your years of service and final average salary, you lack the foundation needed to evaluate additional guaranteed income needs.

Without knowing your actual retirement expenses, you cannot determine whether your TRS pension provides adequate guaranteed income or requires supplementation.

Teachers who underestimate inflation’s impact on purchasing power may find their guaranteed income inadequate in later retirement years.

If you have not evaluated Social Security optimization, TRS benefit maximization, and investment withdrawal strategies, you may be considering expensive annuities when better alternatives exist.

Teachers who have not planned for survivor income needs may leave spouses with inadequate guaranteed income or purchase unnecessary insurance coverage.

Most teachers do not discover gaps in their retirement plan until it is too late to make meaningful corrections. By the time you realize your TRS pension falls short of your income needs, you may have limited options to bridge the gap.

Annuity purchases become more expensive as you age, and retirement account balances may be insufficient to generate the guaranteed income you need. Teachers who wait until the final years before retirement often face difficult choices between working longer, reducing expenses, or accepting financial uncertainty.

Testing your retirement assumptions and income projections while you still have time to adjust your strategy prevents these last-minute crises. The decisions you make about guaranteed income today determine your financial security throughout retirement.

Every Texas teacher’s retirement situation is unique. Your years of service, final average salary, other retirement savings, and income needs create a specific combination that requires personalized analysis.

Understanding whether annuities complement your TRS pension or create unnecessary costs requires examining your complete financial picture. The right guaranteed income strategy depends on factors that generic advice cannot address.

Schedule your comprehensive TRS retirement analysis to discover the optimal combination of guaranteed income sources for your specific situation.

Use the TRS calculator to estimate your pension and identify potential income gaps.