Should You Downsize in Retirement as a Teacher?

Downsizing can improve cash flow—but it’s not always the right move.

A fixed pension loses buying power over time. Learn how inflation affects TRS.

Your Texas TRS pension provides a fixed monthly payment for life, but that fixed amount becomes worth less every year due to inflation. While your $4,200 monthly pension might cover your expenses today, it will buy significantly less in 10, 15, or 25 years of retirement.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

Understanding the inflation TRS pension impact helps you plan for the purchasing power erosion that affects every Texas teacher’s retirement income. Unlike Social Security, which includes cost-of-living adjustments, your TRS pension stays the same nominal amount while everything around you becomes more expensive.

This creates a hidden retirement income gap that grows larger each year you remain retired. The teachers who recognize this early and plan accordingly maintain their standard of living throughout retirement. Those who don’t often find themselves struggling financially in their later retirement years.

Most retirement plans fail because they are never tested under real-world conditions like sustained inflation, unexpected healthcare costs, or market downturns. A comprehensive Texas Teacher Retirement Planning Guide examines these variables and stress-tests your plan before you need it most.

Inflation reduces the purchasing power of your TRS pension every single year. Even with historically low inflation rates around 2-3% annually, your pension buys noticeably less after a decade of retirement.

Use the TRS calculator to estimate your pension and identify potential income gaps.

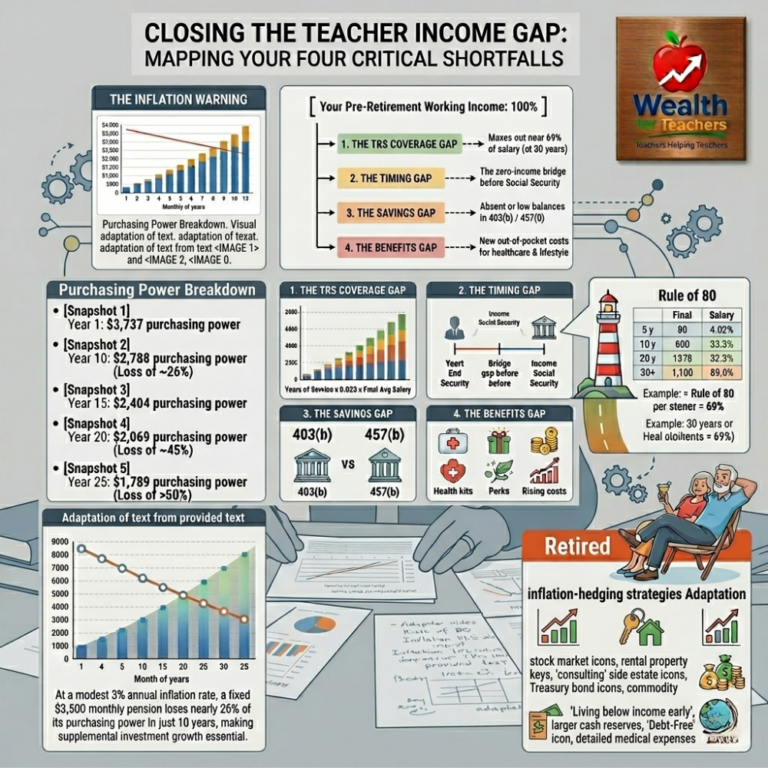

Your TRS pension calculation uses this formula: Annual Pension = (Years of Service × 0.023) × Final Average Salary. A teacher with 30 years of service earning a $65,000 final average salary receives an annual pension of $44,850, or $3,737 per month.

That $3,737 monthly payment never changes, but inflation affects everything you buy:

The gap between your fixed income and rising expenses widens every year you stay retired.

Let’s examine how a $3,737 monthly TRS pension loses value over a typical 25-year retirement with 3% annual inflation:

Year 1 of retirement: $3,737 monthly pension has $3,737 in purchasing power

Year 10 of retirement: Same $3,737 monthly pension has $2,788 in today’s purchasing power

Year 20 of retirement: Same $3,737 monthly pension has $2,069 in today’s purchasing power

Year 25 of retirement: Same $3,737 monthly pension has $1,789 in today’s purchasing power

Your pension loses more than half its purchasing power over 25 years with just 3% inflation. Higher inflation rates, which we’ve seen in recent years, accelerate this erosion significantly.

This creates what economists call “real income decline” – your nominal income stays the same while your real income falls every year.

Many federal employees and Social Security recipients receive annual cost-of-living adjustments (COLAs) that help their income keep pace with inflation. Texas TRS does not provide automatic COLAs.

The Texas Legislature can approve ad hoc increases to TRS pensions, but these are:

Since 2004, TRS has provided only a few small increases that haven’t kept up with cumulative inflation. You cannot count on legislative increases to protect your pension’s purchasing power.

Healthcare expenses typically increase faster than general inflation, creating additional pressure on your fixed pension income. Healthcare costs for retired teachers often double every 10-12 years, far outpacing the 2-3% general inflation rate.

TRS-Care premiums for retirees have increased significantly over the past decade. What starts as a manageable healthcare expense in early retirement can consume an ever-growing portion of your fixed pension income.

Medicare doesn’t solve this problem entirely. Medicare supplements, prescription drug coverage, and out-of-pocket expenses continue rising faster than your fixed TRS pension income.

Your TRS pension isn’t the only retirement income source vulnerable to inflation. Other fixed income investments lose purchasing power over time:

Building multiple retirement income streams that include inflation-protected components becomes critical for maintaining purchasing power throughout retirement.

Protecting your retirement income from inflation requires planning beyond your TRS pension. Consider these inflation-hedging strategies:

Create retirement income that can potentially grow with or exceed inflation:

Real assets often maintain or increase value during inflationary periods:

Budget assuming your expenses will increase faster than your TRS pension income. This might mean:

Your inflation protection strategy depends on your specific circumstances and retirement timeline. Here are common decision paths Texas teachers face:

When this applies: You have 25-35 years of retirement ahead, making inflation erosion your biggest risk.

What to consider: Prioritize growth investments over safety. Your TRS pension provides the safety, so other income sources should focus on inflation protection.

What goes wrong: Being too conservative with investments and watching inflation destroy your purchasing power over decades of retirement.

When this applies: You’re retiring around age 58-62 with 20-25 years of expected retirement.

What to consider: Balance current income needs with long-term inflation protection. You need some growth but can’t take excessive risk with income you’ll need soon.

What goes wrong: Focusing only on current income needs and ignoring the inflation impact that will hit hard in your 70s and 80s.

When this applies: Your TRS pension represents most of your retirement income, with minimal 403(b) or other savings.

What to consider: Address the retirement income gap by extending your career, reducing expenses, or creating additional income streams before retiring.

What goes wrong: Retiring too early without adequate inflation protection and watching your standard of living decline throughout retirement.

When this applies: You have significant 403(b), IRA, or other investments beyond your TRS pension.

What to consider: Use your additional savings strategically for inflation protection while treating your TRS pension as the bond-like foundation of your portfolio.

Use the TRS calculator to estimate your pension and identify potential income gaps.