How to Build a Guaranteed Income Floor as a Teacher

Stable income is the foundation of retirement security. Learn how to build it.

TRS and Social Security: How Texas Teacher Retirement Coordinates With Federal Benefits When you’re a Texas teacher planning for retirement, understanding how your Teacher Retirement System (TRS) pension works alongside Social Security benefits is crucial for making informed decisions about your financial future. Unlike some states where teachers don’t pay into Social Security at all, […]

When you’re a Texas teacher planning for retirement, understanding how your Teacher Retirement System (TRS) pension works alongside Social Security benefits is crucial for making informed decisions about your financial future. Unlike some states where teachers don’t pay into Social Security at all, Texas teachers participate in both systems, creating unique opportunities and considerations for your retirement planning.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

This comprehensive guide explains exactly how TRS and Social Security work together, what benefits you can expect from each system, and how to maximize your combined retirement income. Whether you’re just starting your teaching career or approaching retirement, understanding these two pillars of your retirement security will help you make better financial decisions.

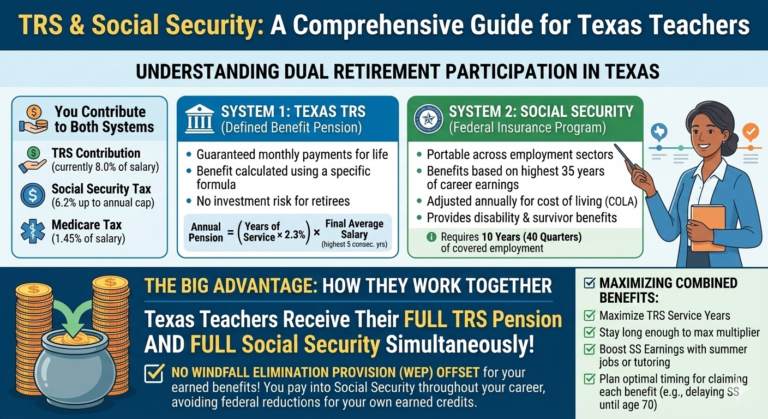

Texas is one of the states where public school teachers participate in both the Teacher Retirement System and Social Security. This dual participation means you’re building retirement benefits through two separate systems simultaneously throughout your teaching career.

Use the TRS calculator to estimate your pension and identify potential income gaps.

Here’s how it works in practice:

This dual system creates a more robust retirement foundation compared to teachers in states that only participate in one system or the other. However, it also means you need to understand how both systems work to optimize your retirement strategy.

While both systems provide retirement income, they operate very differently:

TRS operates as a defined benefit pension plan:

Social Security functions as a federal insurance program:

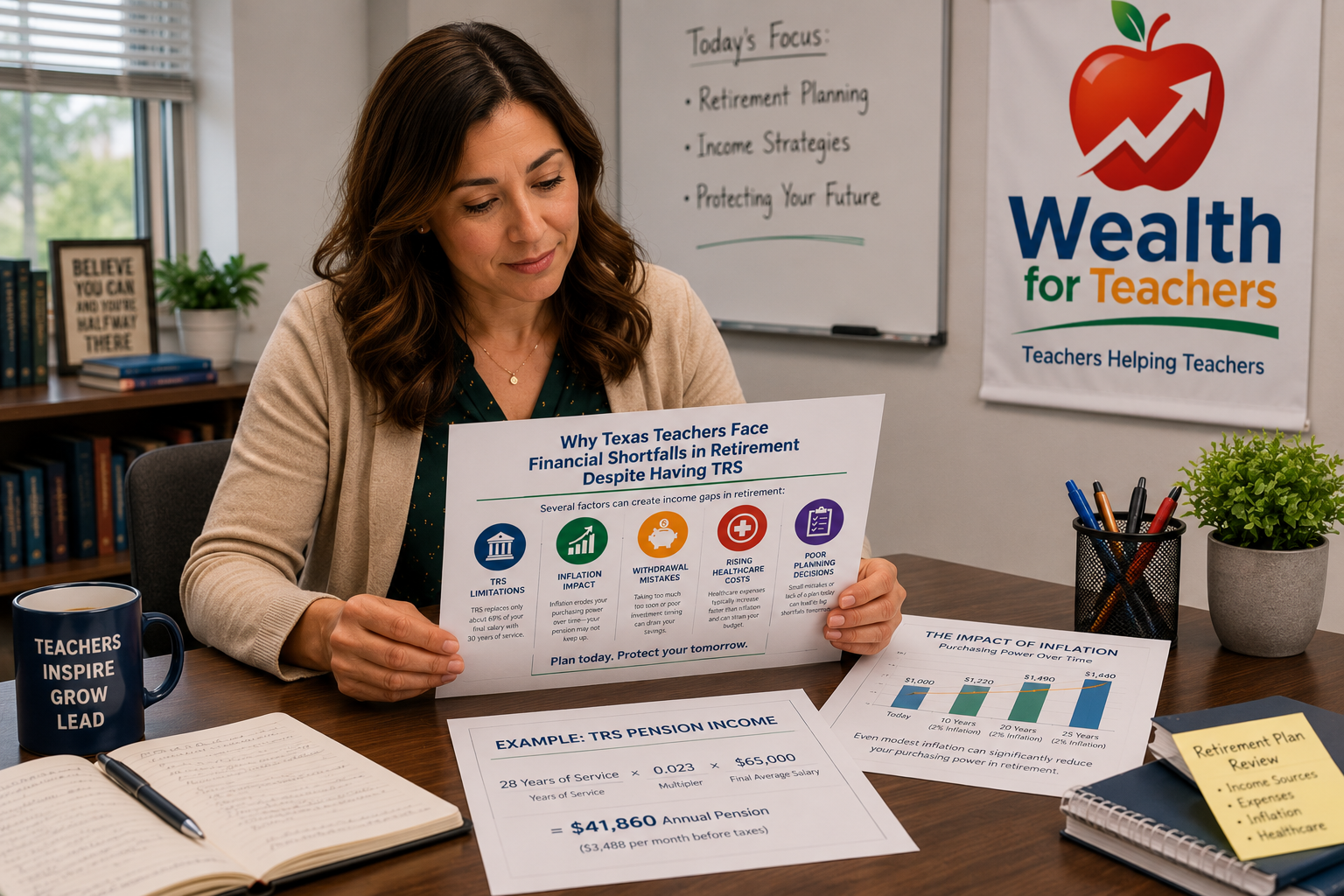

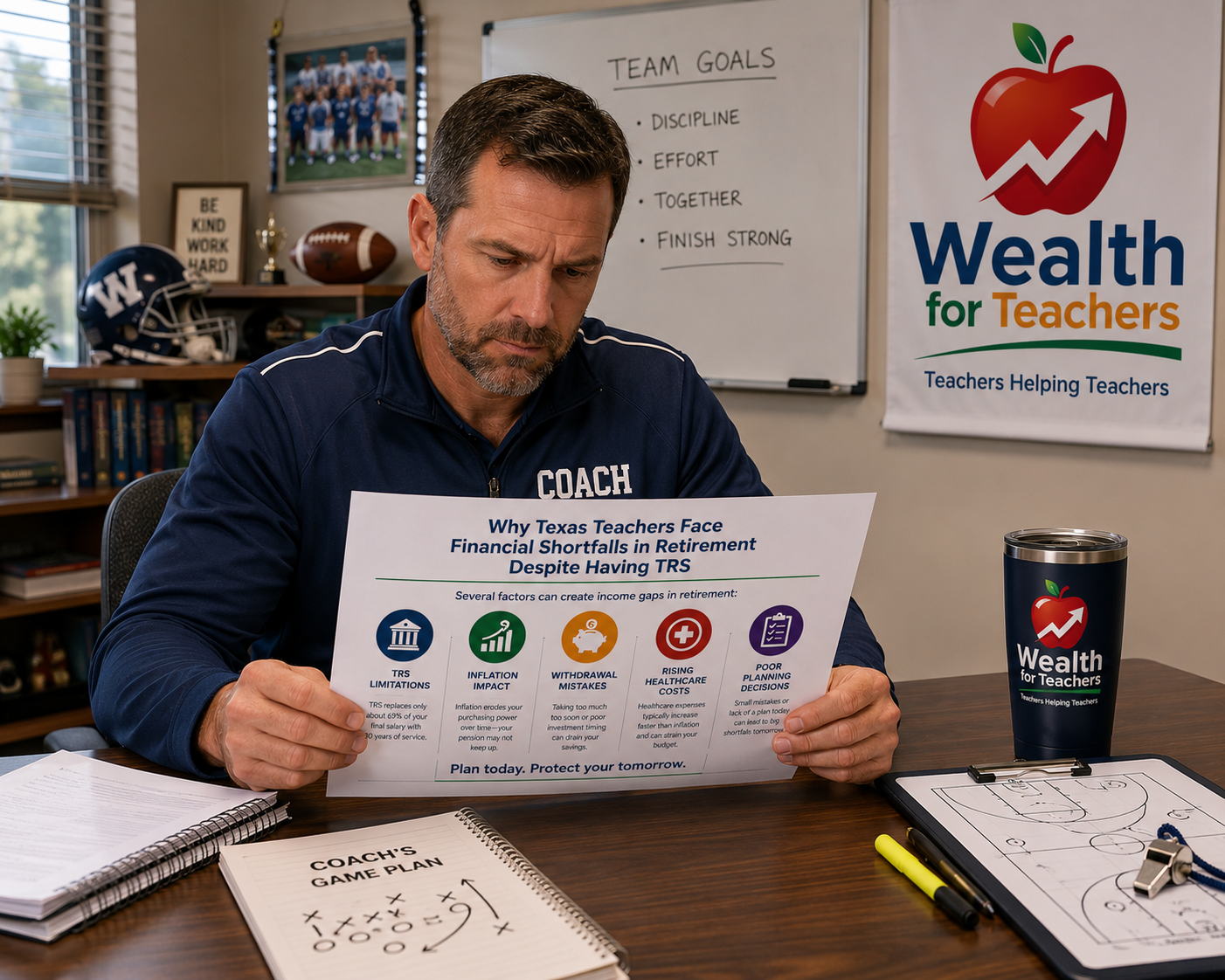

The Texas TRS pension uses a straightforward formula that applies a flat 2.3% multiplier for each year of creditable service. This multiplier does not change based on how many years you work – it remains constant throughout your career.

Your annual TRS pension equals:

Annual Pension = (Years of Service × 2.3%) × Final Average Salary

Let’s break this down with a clear example:

Example (for illustration purposes only):

Calculation:

This teacher would receive $37,375 annually from TRS, or about $3,115 per month.

Your Final Average Salary for TRS purposes is calculated using your five highest consecutive years of salary. This typically occurs at the end of your career when your salary is highest, but TRS will automatically use whichever five consecutive years produce the highest average.

As a Texas teacher, you earn Social Security credits just like workers in the private sector. You need 40 quarters (10 years) of covered employment to qualify for Social Security retirement benefits.

Social Security uses a complex formula based on your highest 35 years of earnings, adjusted for inflation. The system applies different percentages to different portions of your average indexed monthly earnings:

This progressive formula means lower-income earners receive a higher percentage of their pre-retirement income from Social Security compared to higher earners.

The average Social Security benefit varies widely based on your earnings history and the age you claim benefits. Teachers who work additional jobs during summers or after retirement may increase their Social Security benefits by adding to their earnings record.

Important timing considerations:

One of the advantages of Texas teacher retirement is that TRS and Social Security benefits don’t reduce each other. You can collect your full TRS pension and your full Social Security benefits simultaneously without any offset or reduction.

This differs significantly from some other states where teacher pensions are subject to the Windfall Elimination Provision (WEP) or Government Pension Offset (GPO). Texas teachers generally avoid these federal provisions because they pay into Social Security throughout their careers.

The Windfall Elimination Provision typically reduces Social Security benefits for people who receive pensions from employment where they didn’t pay Social Security taxes. Since Texas teachers do pay Social Security taxes, WEP typically doesn’t apply to their benefits.

The Government Pension Offset affects spousal and survivor Social Security benefits for people receiving government pensions. Texas teachers need to understand how GPO might affect spousal benefits, though the impact varies based on individual circumstances.

The timing of when you claim TRS and Social Security benefits can significantly impact your total retirement income. These systems have different eligibility requirements and optimal claiming strategies.

You can retire with full TRS benefits under several scenarios:

Your Social Security claiming decision should coordinate with your TRS retirement timing:

If you retire from teaching before Social Security eligibility:

If you’re eligible for both simultaneously:

To optimize your TRS and Social Security benefits, consider these strategies throughout your career:

Maximize your TRS benefits:

Boost your Social Security earnings:

Create a comprehensive retirement timeline that considers:

Yes, Texas teachers can collect both TRS pension benefits and Social Security simultaneously without reduction from either system. This is one of the significant advantages of Texas teacher retirement compared to some other states. You may also want to understand the biggest TRS retirement mistakes teachers make at 50+.

Yes, as long as you worked at least 10 years (40 quarters) in covered employment. Your years teaching in Texas count toward Social Security eligibility because Texas teachers pay Social Security taxes.

If you return to work for a TRS-covered employer after retirement, your TRS benefits may be suspended depending on your type of retirement and the position you take. However, working in non-TRS employment generally doesn’t affect your TRS benefits. Social Security has earnings limits before full retirement age that could temporarily reduce benefits if you earn too much.

Your TRS benefits are vested after 5 years of service credit. If you leave before vesting, you can withdraw your contributions. If you’re vested, you can leave your money in the system and claim benefits at retirement age, or you may be eligible for a refund of contributions. Your Social Security benefits remain yours regardless of when you leave teaching.

If you work in Social Security-covered employment after retiring from teaching, those earnings can potentially increase your Social Security benefits. Social Security recalculates your benefits annually if your new earnings would result in higher benefits.

Both TRS and Social Security provide survivor benefits, but they work differently. TRS survivor benefits depend on your retirement option selection, while Social Security survivor benefits are based on your earnings record and when benefits are claimed. Survivors may be eligible for benefits from both systems.

This depends on your individual situation. Delaying Social Security until age 70 can increase your benefits by up to 8% per year after full retirement age. If your TRS pension covers your basic expenses, delaying Social Security might make sense to maximize your total retirement income.

If you have service in states where teachers don’t pay Social Security taxes, those years could potentially subject your Social Security benefits to the Windfall Elimination Provision, reducing your benefits. However, your Texas teaching years count as covered employment for Social Security purposes.

Rather than trying to navigate TRS and Social Security coordination alone, take these proactive steps to optimize your retirement planning:

Don’t rely solely on TRS and Social Security for retirement security. These systems provide a foundation, but most financial experts recommend replacing 70-80% of pre-retirement income. Consider additional retirement savings through:

Stay informed about your projected benefits from both systems:

Healthcare represents one of the largest expenses in retirement. Texas teachers have access to TRS health insurance in retirement, but you’ll need to budget for:

The interaction between TRS, Social Security, and your other retirement savings can be complex. Consider working with financial professionals who understand teacher retirement benefits to help you:

Understanding how TRS and Social Security work together gives you a significant advantage in retirement planning. By maximizing both systems and supplementing them with additional savings, you can work toward a financially secure retirement that supports the lifestyle you’ve earned through your years of dedicated service to Texas students.

Take action now to review your current trajectory toward retirement. The decisions you make today about your career length, salary growth, and additional retirement savings will determine your financial security in retirement. Your future self will thank you for the planning you do today.

Use the TRS calculator to estimate your pension and identify potential income gaps.