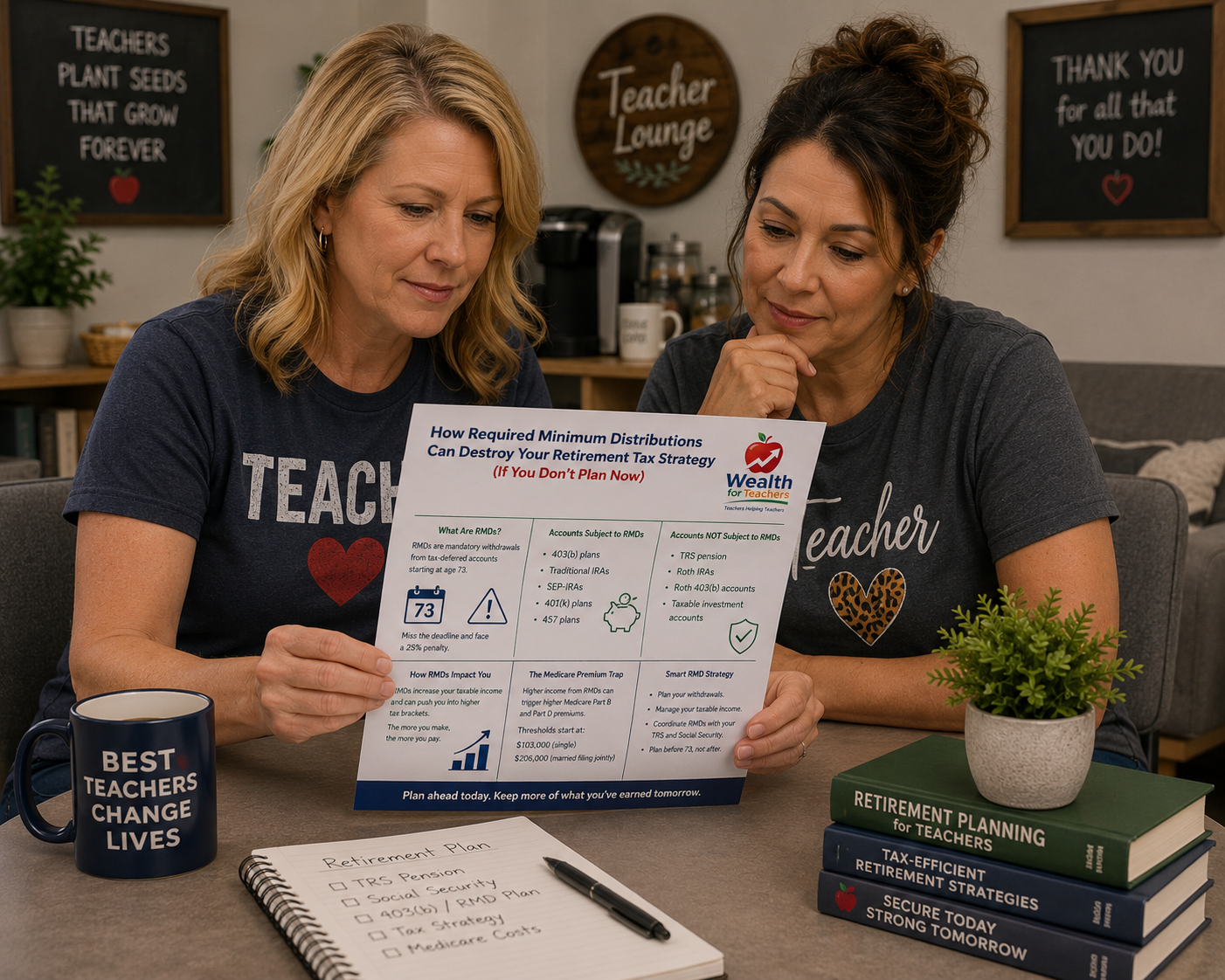

What Teachers Need to Know About Required Minimum Distributions (RMDs) Before It’s Too Late

Required Minimum Distributions can increase taxes if not planned correctly. Learn how teachers should handle RMDs.

Thinking about cashing out your TRS? Learn the hidden taxes, penalties, and long-term costs that could drain your retirement. Free guide for Texas teachers.

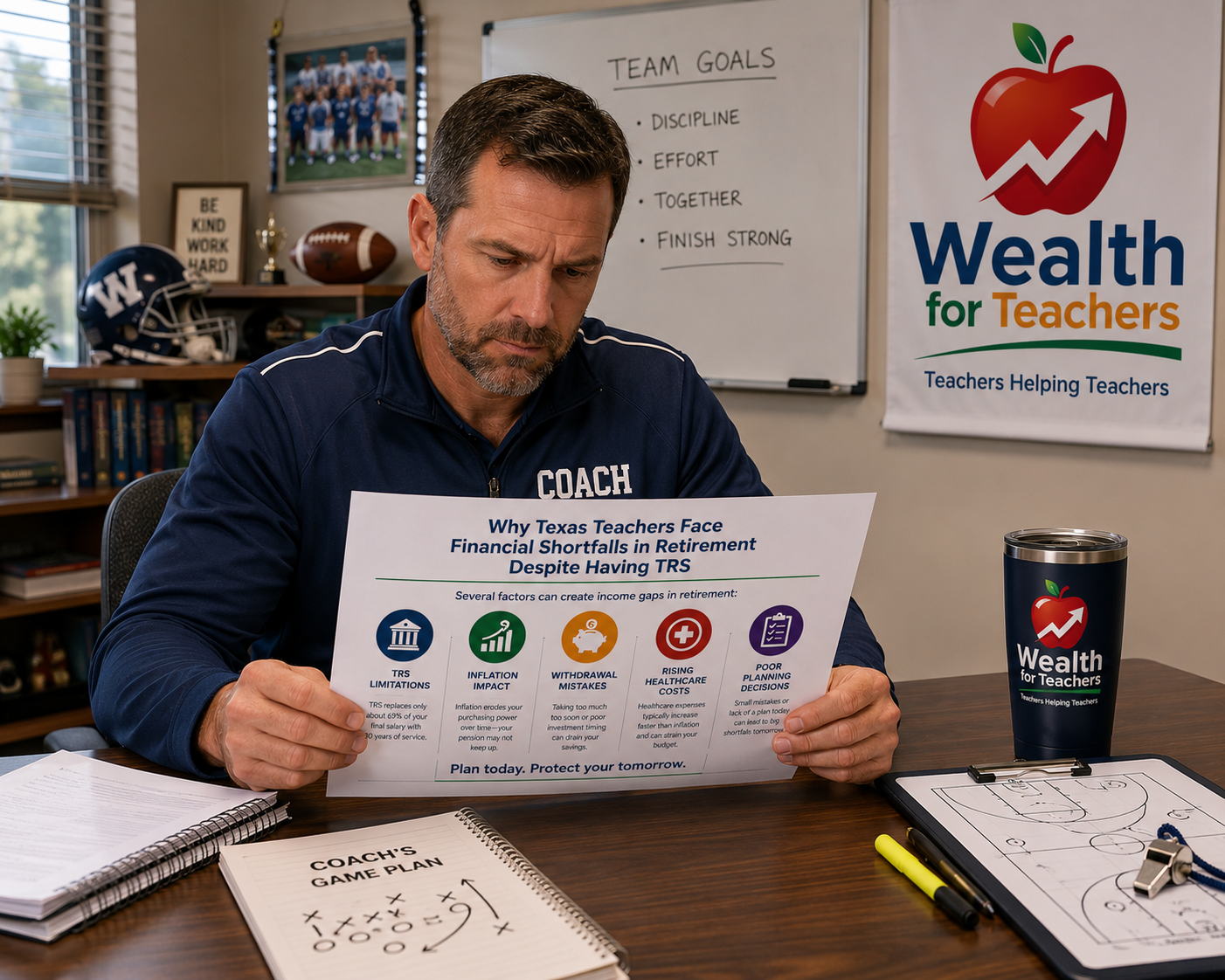

The Teacher Retirement System of Texas (TRS) serves as the cornerstone of retirement security for educators across the Lone Star State. With over 1.6 million members, TRS represents one of the largest public retirement systems in the United States, providing essential benefits to teachers, administrators, and education support staff throughout Texas.

Understanding your TRS benefits isn’t just important—it’s crucial for making informed decisions about your financial future. Whether you’re a new teacher just starting your career or a veteran educator planning your retirement, knowing how the system works can help you maximize your benefits and avoid costly mistakes.

Many Texas educators leave money on the table simply because they don’t fully understand their retirement benefits. From vesting requirements to benefit calculations, the TRS system has specific rules and opportunities that can significantly impact your retirement income.

Texas Teacher Retirement Guide

The Teacher Retirement System of Texas is a defined benefit pension plan established in 1937 to provide retirement, disability, and survivor benefits to Texas public education employees. TRS operates as a trust fund, with contributions from members, employers, and the state funding the system’s operations and benefit payments.

TRS covers employees of Texas public schools, community colleges, regional education service centers, and charter schools. The system also extends to certain employees of state agencies involved in education, such as the Texas Education Agency and the Texas School for the Blind and Visually Impaired.

The system operates under Texas state law and is governed by a nine-member Board of Trustees. Six members are appointed by the governor, while three are elected by TRS members. This structure ensures both state oversight and member representation in system governance.

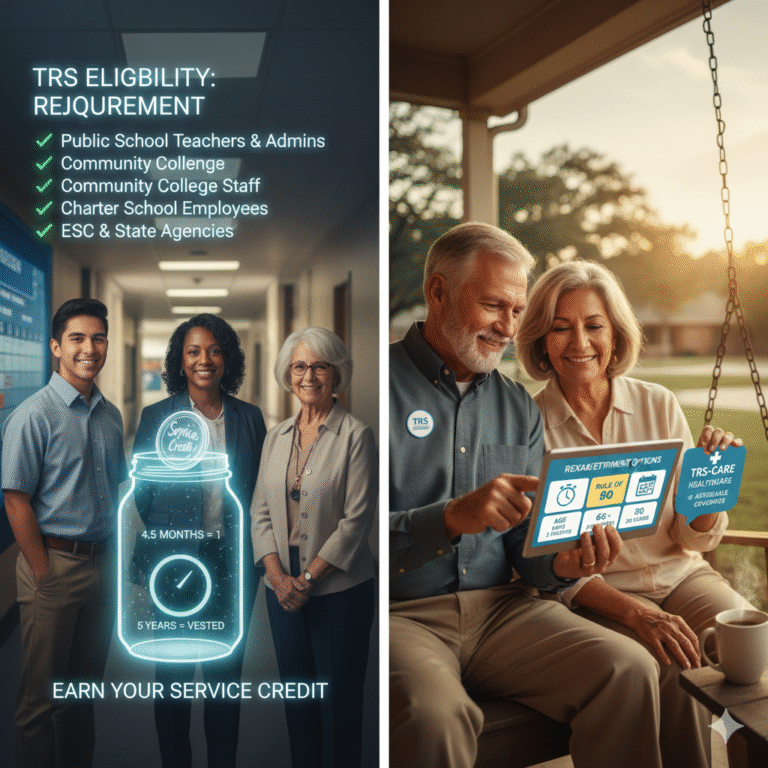

Understanding TRS eligibility is fundamental for Texas educators. Most public education employees in Texas are automatically enrolled in TRS when they begin employment, but there are specific requirements and exceptions to be aware of.

You’re automatically enrolled in TRS if you work in any of these positions:

TRS membership requires both employee and employer contributions:

These contributions are mandatory and are automatically deducted from your paycheck. The combined contributions fund your future retirement benefits and help maintain the system’s financial stability.

Service credit is earned for each school year you work in a TRS-covered position. You earn one year of service credit for working at least four and one-half months in a school year. Part-time employees earn proportional service credit based on their work schedule.

TRS provides several types of benefits designed to support members and their families throughout various life circumstances. Understanding these benefit types helps you plan effectively for your future.

Service retirement is the primary benefit most teachers work toward. This monthly pension is calculated based on your years of service, average salary, and a benefit multiplier. The benefit provides income for life, with built-in cost-of-living adjustments to help protect against inflation.

TRS offers disability benefits for members who become unable to work due to a mental or physical condition. There are two types of disability benefits:

Disability benefits provide monthly income and may include healthcare coverage, depending on your specific situation and years of service.

TRS provides financial protection for your beneficiaries through various survivor benefits. These may include monthly payments to surviving spouses and eligible children, as well as lump-sum death benefits.

If you leave TRS-covered employment before retirement, you may be eligible to withdraw your member contributions plus interest. However, this option means forgoing your pension benefits, so it requires careful consideration.

Understanding how TRS calculates your retirement benefits is crucial for planning your financial future. The benefit calculation uses a straightforward formula, but several factors can significantly impact your final monthly payment.

Your monthly TRS benefit is calculated using this formula:

Years of Service Credit × Average of Highest 5 Years’ Salary × 2.3% = Monthly Benefit

Let’s break down each component:

This includes all creditable service you’ve earned in TRS-covered positions. You can earn up to one year of service credit per school year, and the maximum service credit for benefit calculation purposes is typically 40 years.

TRS uses your five highest salary years to calculate your average salary. These don’t have to be consecutive years, and the system automatically identifies your highest-earning years. Only TRS-reportable compensation counts toward this calculation.

The 2.3% multiplier applies to each year of service credit. This means that with 30 years of service, you’d receive 69% (30 × 2.3%) of your average salary as your monthly benefit.

Consider a teacher with:

Monthly benefit calculation:

30 × $65,000 × 2.3% = $44,850 annually, or $3,737.50 monthly

Understanding Texas teacher retirement calculator tools can help you project your future benefits based on different scenarios and career decisions.

Vesting determines your right to receive TRS benefits. Unlike some retirement systems with complex vesting schedules, TRS has straightforward rules that provide security for Texas educators.

You become vested in TRS after completing five years of service credit. Once vested, you have earned the right to receive a monthly retirement benefit when you meet the age and service requirements, even if you leave TRS-covered employment.

Vesting provides several important protections:

If you leave TRS-covered employment before reaching five years of service, you can:

However, you won’t be eligible for a monthly retirement benefit until you become vested.

TRS offers several retirement options, each with different age and service requirements. Understanding these options helps you plan the timing of your retirement and optimize your benefits.

The Rule of 80 is often the most attractive retirement option for Texas teachers. You can retire without penalty when your age plus years of service credit equals 80, with at least five years of service credit and a minimum age of 55.

Benefits of Rule of 80 retirement:

You can retire at age 65 with just five years of service credit. This option provides full benefits without any reduction, making it attractive for later-career educators or those who change careers.

This option allows retirement at age 60 with 20 years of service credit. You’ll receive full benefits without reduction, providing flexibility for educators who want to retire in their early 60s.

TRS also offers early retirement with reduced benefits:

Early retirement can provide flexibility, but the benefit reductions are permanent, so careful consideration is essential.

TRS-Care provides healthcare coverage for eligible retirees and their dependents. Understanding these benefits is crucial since healthcare often represents a significant expense in retirement.

You’re eligible for TRS-Care if you:

TRS-Care offers several coverage levels:

TRS-Care premiums vary based on your years of service and coverage level. Generally, more years of service result in lower premium costs. The state of Texas subsidizes a portion of the premiums, making TRS-Care more affordable than many private insurance options.

For detailed information about TRS healthcare benefits, including current premium rates and coverage details, consult the official TRS resources or speak with a benefits counselor.

Yes, TRS allows you to purchase certain types of service credit, including military service, out-of-state teaching experience, and leave of absence periods. However, there are specific rules, deadlines, and costs associated with each type of purchase. Contact TRS directly to determine your eligibility and get cost estimates for purchasing additional service credit.

Part-time TRS members earn proportional service credit based on their work schedule. For example, if you work half-time, you’ll earn 0.5 years of service credit per school year. Your contributions and future benefits are also calculated proportionally based on your part-time salary.

Yes, but there are restrictions. You can work in non-TRS covered positions without affecting your benefits. If you return to TRS-covered employment, you may work up to certain limits without losing benefits, but exceeding these limits can result in suspension of your retirement payments.

Divorce can impact TRS benefits in several ways. Your spouse may be entitled to a portion of your TRS benefits as marital property, depending on your divorce decree. You’ll also need to update your beneficiary information and may need to make changes to survivor benefit elections.

TRS benefits are protected by the Texas Constitution, which prohibits the reduction of retirement benefits for current members and retirees. The system undergoes regular actuarial evaluations, and the Texas Legislature makes adjustments as needed to ensure long-term sustainability. The Teacher Retirement System of Texas provides detailed financial reports and actuarial studies for those interested in the system’s financial health.

If you withdraw your TRS contributions, you can roll eligible portions to another qualified retirement account, such as an IRA or another employer’s 401(k) plan. However, this means giving up your right to future TRS pension benefits, so consider this decision carefully.

You should apply for TRS retirement benefits 60-90 days before your planned retirement date. The application process includes completing retirement paperwork, attending a benefits counseling session, and making important elections about survivor benefits and healthcare coverage. TRS provides online tools and counselors to help guide you through this process.

TRS offers several survivor benefit options for spouses, including monthly payments and lump-sum death benefits. The specific benefits available depend on your years of service, age at retirement, and the survivor benefit option you elect. You can choose to provide full or partial survivor benefits, but higher survivor benefits result in reduced monthly retirement payments during your lifetime.

Rather than trying to navigate the complex TRS system alone, take these proactive steps to optimize your retirement benefits:

Don’t wait until retirement to understand your benefits. Schedule annual reviews of your TRS account to:

TRS regularly offers workshops and webinars covering various topics:

These educational opportunities provide valuable information and allow you to ask specific questions about your situation.

While TRS provides excellent benefits, they’re just one part of your overall retirement strategy. Consider working with a financial advisor who understands teacher retirement planning to:

To optimize your TRS benefits:

TRS benefits and rules can change based on legislative action or system needs. Stay informed by:

Your TRS benefits represent a significant portion of your retirement security. By understanding how the system works and taking proactive steps to optimize your benefits, you can build confidence in your financial future and focus on what you do best—educating Texas students.

Don’t leave your financial future to chance. Get personalized guidance on maximizing your TRS benefits and creating a comprehensive retirement plan that works for your unique situation.

Remember, the decisions you make today about your TRS benefits will impact your financial security for decades to come. Take the time to understand your options, ask questions, and make informed choices that align with your retirement goals. Your future self will thank you for the careful planning you do today.

Get your Free TRS Calculator:

Required Minimum Distributions can increase taxes if not planned correctly. Learn how teachers should handle RMDs.

Stable income is the foundation of retirement security. Learn how to build it.