Should You Downsize in Retirement as a Teacher?

Downsizing can improve cash flow—but it’s not always the right move.

Early TRS Retirement: Understanding Your Options as a Texas Teacher Thinking about leaving the classroom before you reach full retirement eligibility? You’re not alone. Many Texas teachers consider stepping away from their careers early for various reasons – burnout, family obligations, health concerns, or simply wanting to pursue other opportunities while they’re still young enough […]

Thinking about leaving the classroom before you reach full retirement eligibility? You’re not alone. Many Texas teachers consider stepping away from their careers early for various reasons – burnout, family obligations, health concerns, or simply wanting to pursue other opportunities while they’re still young enough to enjoy them.

The decision to retire early from the Teacher Retirement System of Texas (TRS) is complex and comes with significant financial implications. Unlike some career fields where early retirement might mean accessing a full pension with minor reductions, TRS has specific rules and penalties that can dramatically impact your monthly benefits for the rest of your life.

This guide will help you understand exactly what early retirement means within the TRS system, the financial costs involved, and alternative strategies that might better serve your long-term financial security.

In the TRS system, early retirement occurs when you choose to begin receiving your pension benefits before meeting the standard retirement requirements. The normal retirement scenarios for Texas teachers are:

If you don’t meet any of these criteria but have at least 5 years of service credit, you can still choose to retire early. However, this decision comes with permanent reductions to your monthly pension that will affect you for the entire duration of your retirement.

The earliest you can begin receiving TRS retirement benefits is age 55, provided you have at least 5 years of creditable service. Retiring between ages 55-59 without meeting the Rule of 80 is considered early retirement and triggers actuarial reductions.

Regardless of when you choose to retire, you must have accumulated at least 5 years of creditable service with TRS. This service doesn’t have to be consecutive, but it must total at least 5 full years. Partial years count toward this requirement based on the actual days worked during the school year.

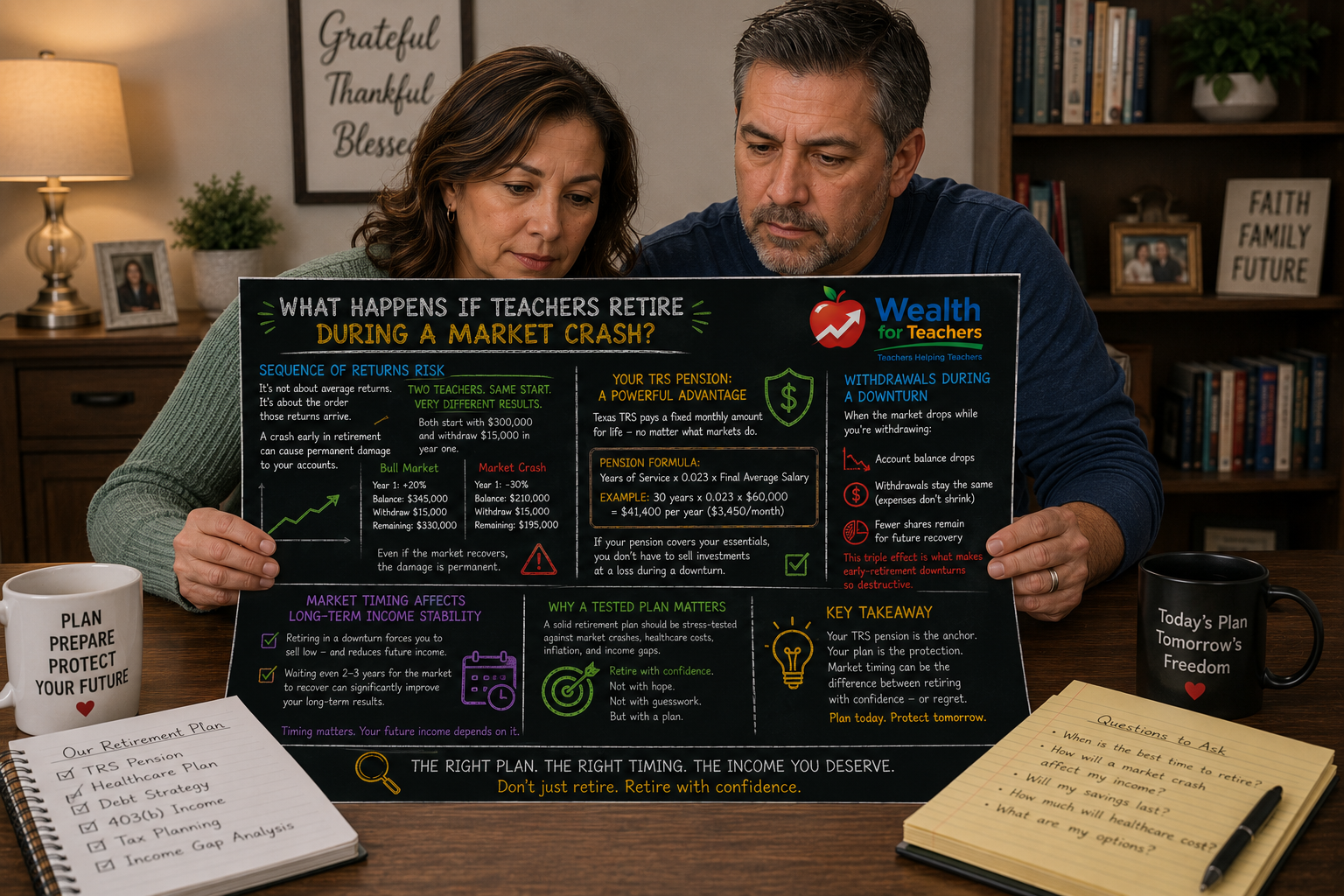

The financial consequences of early TRS retirement are substantial and permanent. Unlike temporary penalties that might be lifted at a certain age, the reductions applied to your pension for early retirement last for your entire lifetime.

TRS applies actuarial reductions based on how early you retire before age 60. These reductions are calculated to account for the longer period over which you’ll receive benefits. The reduction rates are:

For example, if you retire at age 55, you’ll face a 30% reduction in your monthly pension (5 years × 6% = 30%). This means you’ll receive only 70% of what your full pension would have been.

The cumulative effect of these reductions over a retirement that could span 30-40 years is enormous. Consider a teacher who would have received $3,000 per month at full retirement but chooses to retire at 55. With the 30% reduction, they’ll receive $2,100 per month instead.

Over 30 years, this represents a loss of $324,000 in pension income ($900 per month × 12 months × 30 years). This doesn’t account for annual cost-of-living adjustments, which would make the actual loss even greater.

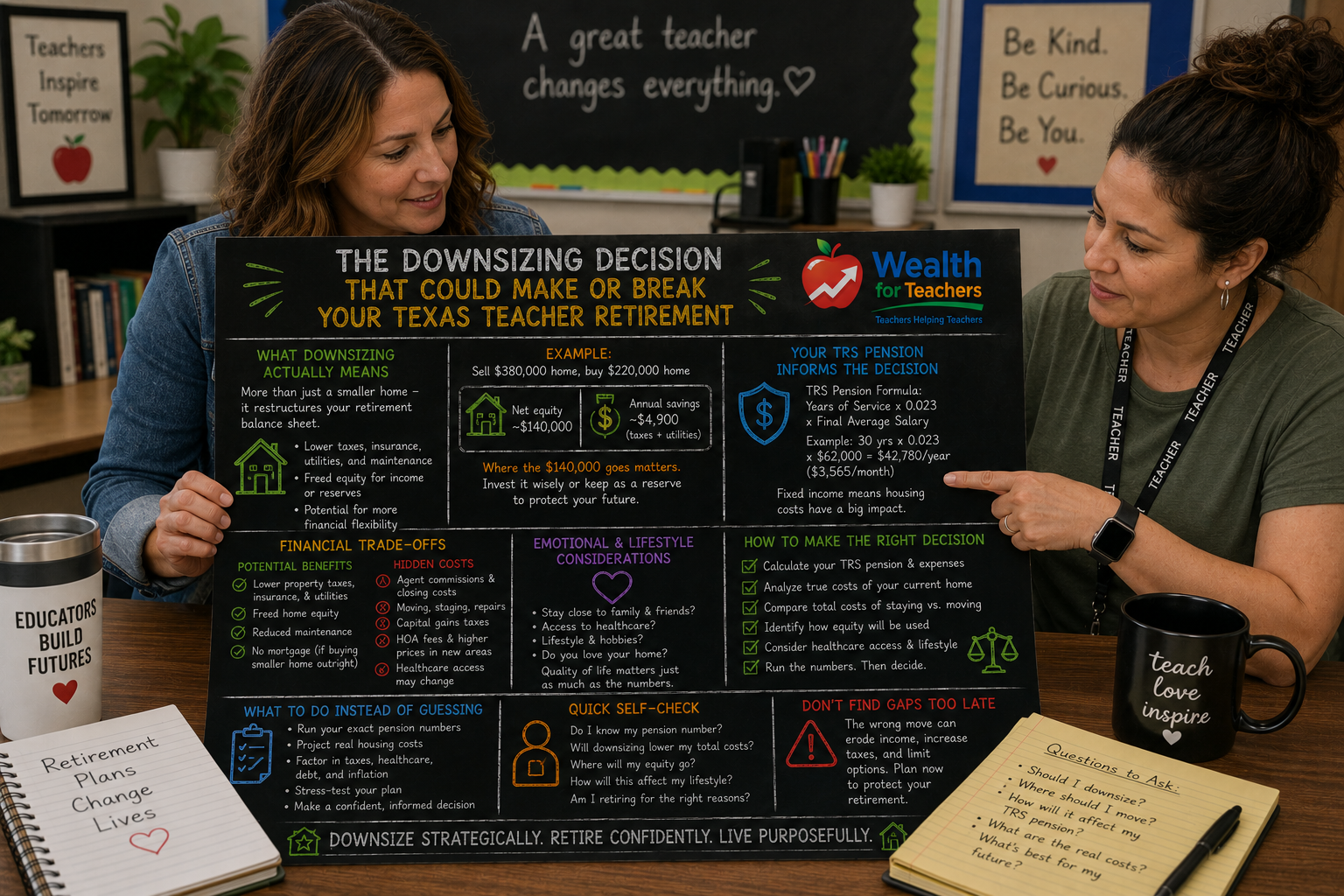

Understanding how TRS calculates your pension is crucial for making an informed decision about early retirement. The basic formula remains the same whether you retire early or at full retirement age, but the early retirement reductions are applied after the base calculation.

TRS uses a straightforward formula with a flat 2.3% multiplier for each year of service:

Annual Pension = (Years of Service × 0.023) × Final Average Salary

Let’s walk through an example calculation:

Example (assumptions stated for illustration):

Step 1: Calculate Base Benefit Percentage

Benefit % = 20 years × 2.3% = 46%

Step 2: Calculate Full Retirement Pension

Annual Pension = $65,000 × 46% = $29,900 per year ($2,492 per month)

Step 3: Apply Early Retirement Reduction

Retiring at 55 means 5 years before age 60: 5 × 6% = 30% reduction

Reduced Annual Pension = $29,900 × (100% – 30%) = $20,930 per year ($1,744 per month)

This teacher loses $748 per month ($8,970 annually) by retiring early, and this reduction is permanent.

The Rule of 80 is often misunderstood by teachers considering early retirement. This rule allows you to retire without actuarial reductions when your age plus years of service equals or exceeds 80. However, it’s not necessarily “early” retirement in the traditional sense.

To qualify for unreduced benefits under the Rule of 80, you need:

For example, a teacher who is 58 years old with 22 years of service meets the Rule of 80 (58 + 22 = 80) and can retire with full benefits. However, a 45-year-old teacher with 35 years of service, despite having more than 80 combined, must wait until age 55 to retire.

If you’re close to meeting the Rule of 80, it often makes financial sense to continue working rather than retire early with reductions. Even one additional year of service can make a dramatic difference in your lifetime pension income.

Consider purchasing additional service credit if you’re close to the Rule of 80. TRS allows members to purchase credit for various types of service, including military service, out-of-state teaching, or leave without pay. This purchased service counts toward both your years of service calculation and the Rule of 80.

One of the most significant challenges of early retirement is maintaining health insurance coverage. TRS provides retiree health insurance, but the eligibility requirements and costs vary significantly based on when you retire.

To be eligible for TRS-Care (the retiree health insurance program), you must:

If you retire early without meeting the Rule of 80, you may face higher premiums for TRS-Care coverage. Additionally, if you’re under age 65, you’ll need to maintain this coverage until you’re eligible for Medicare.

Some teachers consider using COBRA continuation coverage from their active employment, but this is typically only available for 18-36 months. After COBRA expires, you’ll need to find alternative coverage, which can be expensive for individuals not yet eligible for Medicare.

Marketplace insurance plans under the Affordable Care Act might be an option, but premiums can be substantial, especially if your reduced pension income affects your eligibility for subsidies.

Early retirement from TRS doesn’t affect your eventual eligibility for Social Security or Medicare, but it does impact your financial planning for these programs. You may also want to understand how inflation impacts Teacher retirement Income.

Most Texas teachers don’t pay into Social Security on their teacher salary, so they won’t receive Social Security benefits based on their teaching career. However, if you’ve worked in other jobs that paid Social Security taxes, you might be eligible for benefits.

Be aware of the Windfall Elimination Provision (WEP), which can reduce Social Security benefits for people who also receive pensions from employment where they didn’t pay Social Security taxes. This includes TRS pensions.

You become eligible for Medicare at age 65, regardless of when you retire. If you retire early from TRS, you’ll need to bridge the gap between your retirement and Medicare eligibility with other health insurance options.

Planning for Medicare premiums is important, as these will be ongoing costs throughout your retirement. Medicare Part B premiums are based on your income, so your pension amount will affect these costs.

Yes, but there are strict limitations. If you retire and later return to TRS-covered employment, you’ll face restrictions on your earnings and may have to suspend your pension payments. The rules are complex and vary based on how long you’ve been retired and the type of position you take.

Your contributions remain yours regardless of when you retire, as long as you have at least 5 years of service. These contributions, plus interest, are factored into your pension calculation. You cannot withdraw your contributions once you begin receiving monthly pension payments.

No, TRS is a defined benefit pension plan, not a defined contribution plan like a 401(k). You cannot roll your TRS pension to an IRA. However, if you have a 403(b) or 457(b) account from your school district, those accounts can typically be rolled over.

Early retirement reductions generally don’t affect the death benefits available to your beneficiaries. However, the reduced monthly amount you receive will impact any survivor benefits that are calculated as a percentage of your pension.

Purchasing service credit can help you meet the Rule of 80 or reach other retirement milestones sooner. However, you cannot purchase service credit specifically to avoid early retirement reductions if you’re already below the minimum retirement age.

Having both doesn’t prevent early retirement from TRS, but be aware of the Windfall Elimination Provision and Government Pension Offset, which can reduce your Social Security benefits. These federal rules affect many public employees who have pensions from non-Social Security covered employment.

TRS doesn’t offer lump-sum distributions for service retirement. You’ll receive monthly payments for life once you begin your pension. The only exception is if your calculated monthly benefit is extremely small, in which case TRS might offer a small lump sum instead.

The reduction is 6% per year (0.5% per month) for each month you retire before age 60. TRS calculates this precisely based on your exact retirement date and birthdate. You can request a retirement estimate from TRS for your specific situation.

Before making the decision to retire early from TRS, consider these alternative strategies that might better serve your financial future while still addressing your desire to change your current situation.

If burnout or stress is driving your desire to retire early, consider taking a sabbatical or unpaid leave of absence. This gives you time to recharge without permanently reducing your pension benefits. Many school districts offer sabbatical programs for experienced teachers.

During a leave of absence, you can:

Consider moving to a different position within education that might be less stressful or better suited to your current life stage. Options might include:

These positions often still qualify for TRS participation, allowing you to continue building your pension without the stress of a traditional classroom.

Work with your district to create a phased retirement plan. Some districts allow experienced teachers to reduce their workload gradually while maintaining benefits. This might involve:

Instead of retiring early with reduced benefits, focus on building wealth outside of TRS that will allow you to retire comfortably when you reach full retirement eligibility. This approach involves:

Determine the minimum amount you need to save now that will grow to support your retirement needs. This “coast” number represents the point where you could stop saving entirely and still have adequate retirement funds by age 65.

Once you reach this number, you might feel more comfortable making career changes or taking lower-stress positions, knowing your retirement security is already established.

If your desire for early retirement is driven by financial stress, consider moving to an area with a lower cost of living while continuing to teach. Your TRS benefits are portable within Texas, and moving to a less expensive area can dramatically improve your quality of life without sacrificing your pension benefits.

Develop income sources outside of teaching that could eventually replace your teaching salary. This might involve:

Building these revenue streams while still teaching allows you to transition gradually and maintains your TRS benefits until you reach full retirement eligibility.

Before making any major decisions about early retirement, consult with a financial advisor who understands TRS and teacher-specific financial planning. They can help you model different scenarios and understand the long-term implications of your choices.

A good financial advisor can also help you optimize your 403(b) and other retirement savings, potentially creating enough wealth outside of TRS to make early retirement financially viable without taking the pension reductions.

The decision to pursue early retirement from TRS is one of the most significant financial choices you’ll make in your career. While the desire to leave teaching early is understandable, the permanent financial consequences require careful consideration. In most cases, finding alternative solutions that allow you to reach full retirement eligibility will serve your long-term financial security much better than accepting the substantial penalties that come with early retirement.

Take time to explore all your options, run the numbers carefully, and consider seeking professional guidance before making this irreversible decision. Your future self will thank you for the careful planning you do today.