How to Build a Guaranteed Income Floor as a Teacher

Stable income is the foundation of retirement security. Learn how to build it.

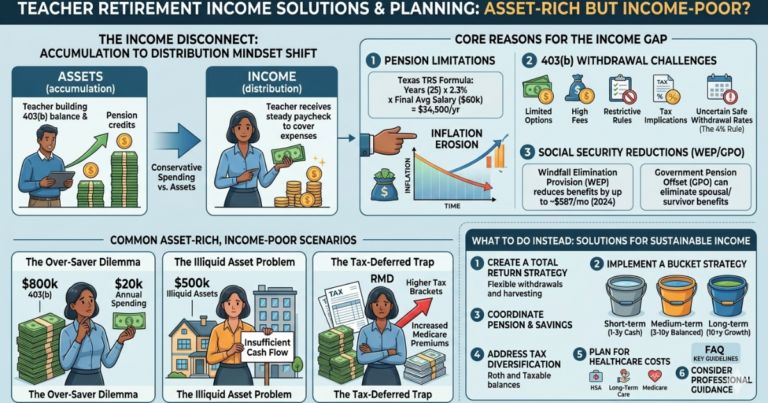

Teacher Retirement Income Problems: When Assets Don’t Generate Enough Money Many teachers face a harsh reality when they retire: having significant assets but struggling to generate enough monthly income to maintain their lifestyle. This phenomenon, often called being “asset-rich but income-poor,” affects educators across the country who discover their retirement savings don’t translate into the […]

Many teachers face a harsh reality when they retire: having significant assets but struggling to generate enough monthly income to maintain their lifestyle. This phenomenon, often called being “asset-rich but income-poor,” affects educators across the country who discover their retirement savings don’t translate into the steady paycheck they need.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

Understanding why this happens and how to address it can make the difference between a comfortable retirement and one filled with financial stress. Teachers who plan ahead can avoid the common pitfalls that leave many retirees with substantial net worth but insufficient monthly cash flow.

Teachers often accumulate assets throughout their careers but struggle to convert those assets into reliable retirement income. This disconnect stems from several unique challenges educators face in retirement planning.

Use the TRS calculator to estimate your pension and identify potential income gaps.

The teaching profession traditionally emphasizes defined benefit pensions, which provide predictable monthly payments. However, many teachers supplement their pensions with retirement accounts that require different withdrawal strategies. When these strategies aren’t properly coordinated, teachers can find themselves with substantial account balances but inadequate monthly income.

Additionally, teachers frequently retire earlier than workers in other professions, extending the period they need their assets to last. A teacher retiring at 58 might need their savings to provide income for 30 years or more, creating pressure to preserve principal while generating current income.

Throughout their careers, teachers focus on accumulating assets in their 403(b) accounts and building pension credits. This accumulation mindset serves them well during their working years but becomes a liability in retirement.

Retirement requires a fundamental shift from saving money to spending it strategically. Many teachers struggle with this transition, preferring to preserve their account balances rather than use them to generate income. This conservative approach often results in retirees living on less income than their assets could safely provide.

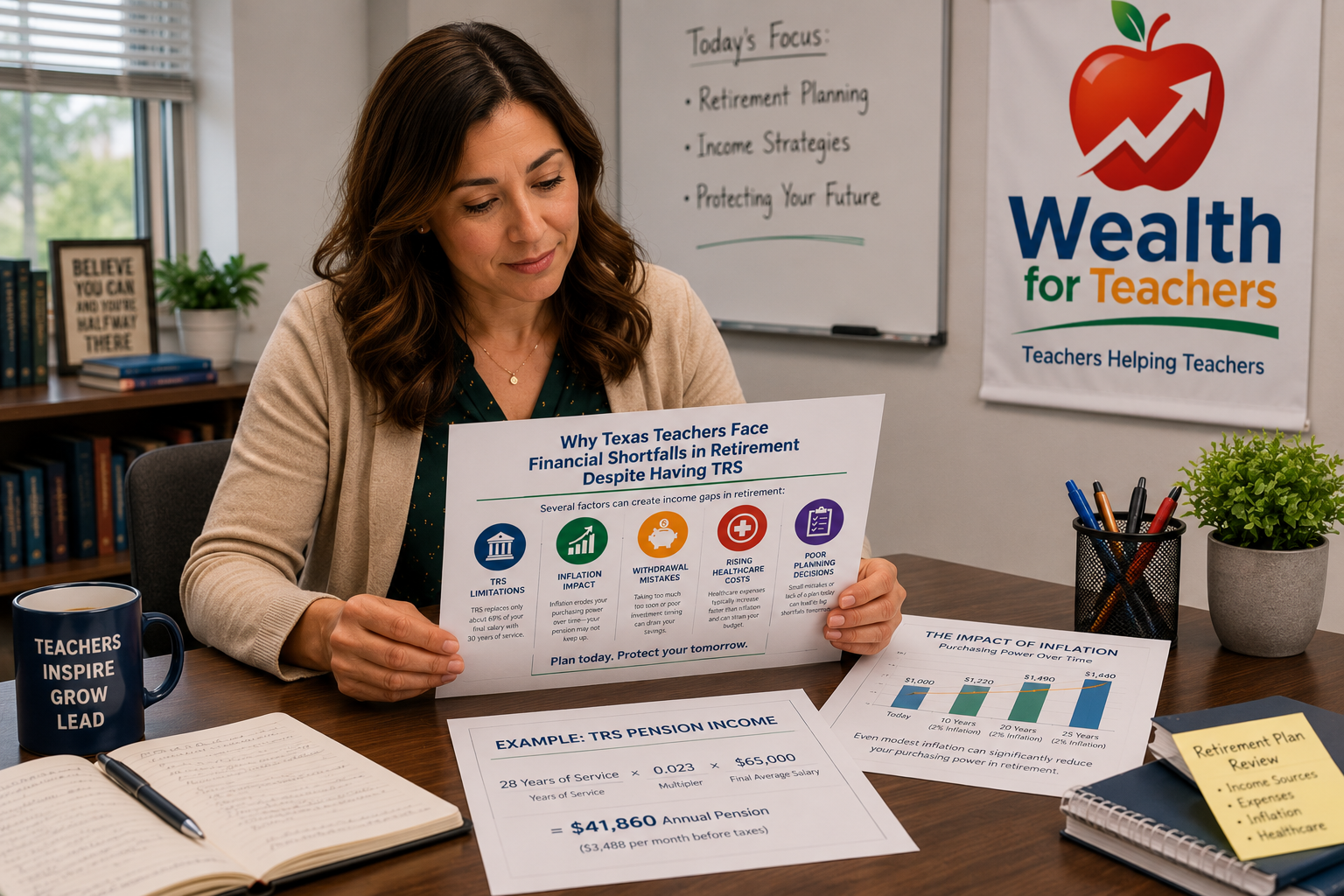

Teacher pension systems provide valuable retirement security, but they rarely replace 100% of pre-retirement income. Understanding how pension benefits are calculated helps teachers identify potential income gaps before they retire.

For Texas TRS participants, the pension calculation uses a straightforward formula:

Example Pension Calculation (for illustration only):

While this teacher has earned a meaningful pension benefit, the $34,500 annual payment represents a significant reduction from their working income. The gap between pension income and living expenses must be filled by other sources. You may also want to understand the differences between TRS Tier 1 vs Tier 2 vs Tier 3.

Many teacher pensions provide limited cost-of-living adjustments, if any. Over a 20-30 year retirement, inflation can significantly erode the purchasing power of a fixed pension payment.

Teachers who retire with pensions that seem adequate today may find themselves struggling financially in later years as living costs rise faster than their pension payments. This reality makes supplemental retirement savings even more critical for maintaining purchasing power throughout retirement.

Many teachers accumulate substantial balances in their 403(b) accounts but lack a clear strategy for converting these assets into retirement income. The challenge isn’t just having money saved – it’s knowing how to withdraw it efficiently.

Teachers often face several withdrawal obstacles:

These challenges can leave teachers with substantial account balances but hesitant to use their money effectively in retirement.

Many teachers have heard of the “4% rule” for retirement withdrawals but don’t understand its limitations. This rule suggests retirees can safely withdraw 4% of their portfolio value annually, adjusted for inflation.

While this guideline provides a starting point, it doesn’t account for individual circumstances like:

Teachers who rigidly apply the 4% rule might unnecessarily restrict their retirement lifestyle, while others might withdraw too aggressively and risk running out of money.

Some teachers face reduced Social Security benefits due to the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO). These provisions can significantly impact retirement income planning.

The WEP affects teachers who receive pensions from employment where they didn’t pay Social Security taxes. It can reduce their Social Security benefits by up to $587 per month in 2024. The GPO can eliminate spousal or survivor benefits for teachers receiving government pensions.

Teachers affected by these provisions often discover the impact late in their careers, leaving little time to adjust their retirement savings strategies. This can create unexpected income shortfalls in retirement. You can read more about how social security and TRS work together.

Teachers who may be affected by WEP or GPO need to plan for potentially significant reductions in expected Social Security benefits. This requires:

Failing to plan for these reductions can leave teachers with substantial asset-to-income conversion challenges in retirement.

Several scenarios commonly leave teachers with significant assets but insufficient income. Recognizing these situations early helps teachers take corrective action.

Some teachers accumulate large 403(b) balances through decades of consistent saving but become paralyzed by the fear of spending their nest egg. They might have $800,000 in retirement accounts but limit themselves to withdrawing only $20,000 annually, living below their means unnecessarily.

This scenario often develops when teachers:

Some teachers invest heavily in real estate or other illiquid assets during their careers. While these investments may appreciate significantly, they don’t generate the monthly income needed for day-to-day expenses.

A teacher might own rental properties worth $500,000 but struggle to generate sufficient cash flow if:

Teachers who save primarily in tax-deferred accounts like traditional 403(b)s can face significant tax burdens in retirement. Large account balances might generate substantial required minimum distributions (RMDs) starting at age 73, pushing retirees into higher tax brackets.

This scenario becomes problematic when:

Teachers can avoid asset-rich, income-poor scenarios by implementing comprehensive retirement income strategies that coordinate all their retirement resources.

Instead of focusing solely on dividends and interest, teachers should consider total return investing. This approach allows for more flexible withdrawal strategies and can provide better long-term results.

A total return strategy might include:

Many teachers benefit from organizing their retirement assets into different “buckets” based on when they’ll need the money:

This approach helps teachers feel more comfortable spending their assets while maintaining growth potential for the future.

Teachers should view their pension and personal savings as components of an integrated retirement income system. This might involve:

Teachers heavily invested in tax-deferred accounts should consider building tax-free and taxable account balances. This diversification provides flexibility for managing taxes in retirement.

Strategies might include:

Healthcare expenses can significantly impact retirement income needs. Teachers should factor these costs into their asset-to-income conversion strategies through:

The complexity of converting assets into sustainable retirement income often warrants professional assistance. Teachers might benefit from working with advisors who understand:

A: The amount depends on your desired retirement lifestyle and expected pension benefit. A common guideline suggests having 10-12 times your final salary saved across all retirement accounts, but this varies based on your specific TRS benefit calculation, Social Security expectations, and retirement goals. Focus on replacing the income gap between your pension and your desired retirement spending rather than hitting arbitrary savings targets.

A: Generally, you cannot take distributions from your employer’s 403(b) plan while still employed unless you qualify for a hardship withdrawal or reach age 59½. However, you may be able to access funds from previous employers’ 403(b) plans or roll money to an IRA for more flexible access. Always check your specific plan rules and consider tax implications before making withdrawals.

A: TRS pensions rarely provide 100% income replacement. Using the TRS formula of 2.3% per year of service, a teacher with 30 years would receive 69% of their final average salary. Most financial experts recommend 70-80% income replacement in retirement, so you’ll likely need additional sources like 403(b) savings, Social Security, or part-time work to maintain your pre-retirement lifestyle.

A: Monitor your withdrawal rate as a percentage of your total portfolio value. Starting withdrawals above 5-6% annually may indicate you’re spending too aggressively. Also watch for declining account balances during good market years, difficulty maintaining your desired lifestyle, or anxiety about running out of money. Regular portfolio reviews and stress-testing your withdrawal strategy can help ensure sustainability.

A: This depends on your interest rate, tax situation, and overall retirement income strategy. If you have a low mortgage rate and limited retirement savings, you might be better served investing extra money rather than paying off the house. However, eliminating the mortgage payment can significantly reduce your required retirement income, providing more financial security. Consider your complete financial picture when making this decision.

A: Your 403(b) assets will pass to your designated beneficiaries according to your beneficiary forms on file with the plan administrator. Beneficiaries typically have options for receiving the funds, including lump-sum distributions or stretched distributions over their lifetimes (though recent law changes have modified these rules). Keep your beneficiary designations current and consider the tax implications for your heirs when planning your estate.

A: Yes, pension income is generally considered qualifying income for mortgage applications. Lenders typically require documentation of your pension benefits, such as an award letter from TRS. However, debt-to-income ratios still apply, so ensure your total monthly obligations don’t exceed lending guidelines. Some lenders may be more familiar with teacher pensions than others, so shop around if you encounter difficulties.

A: Retiring from teaching doesn’t directly affect Social Security benefits, but stopping work reduces the years of earnings used in your Social Security calculation. Social Security benefits are based on your highest 35 years of earnings, so retiring early might mean some years with zero earnings are included in the calculation. Additionally, claiming Social Security before your full retirement age results in permanently reduced benefits, regardless of when you stop teaching.

Use the TRS calculator to estimate your pension and identify potential income gaps.