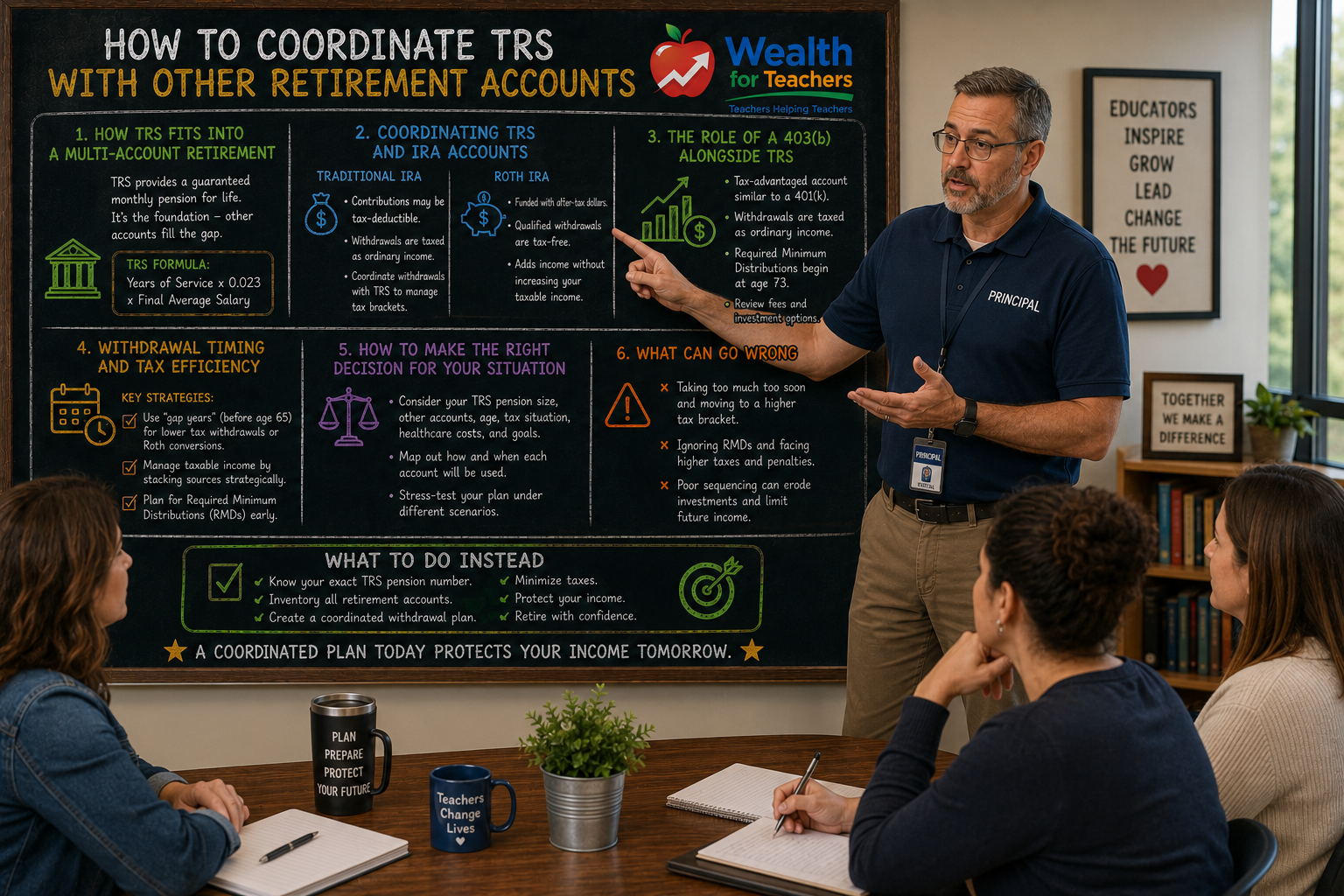

How to Coordinate TRS With IRAs, 403(b)s, and Other Accounts

TRS is only one piece of the puzzle. Learn how to align it with your other accounts.

TRS alone isn’t enough. Learn how to align all your retirement accounts the right way.

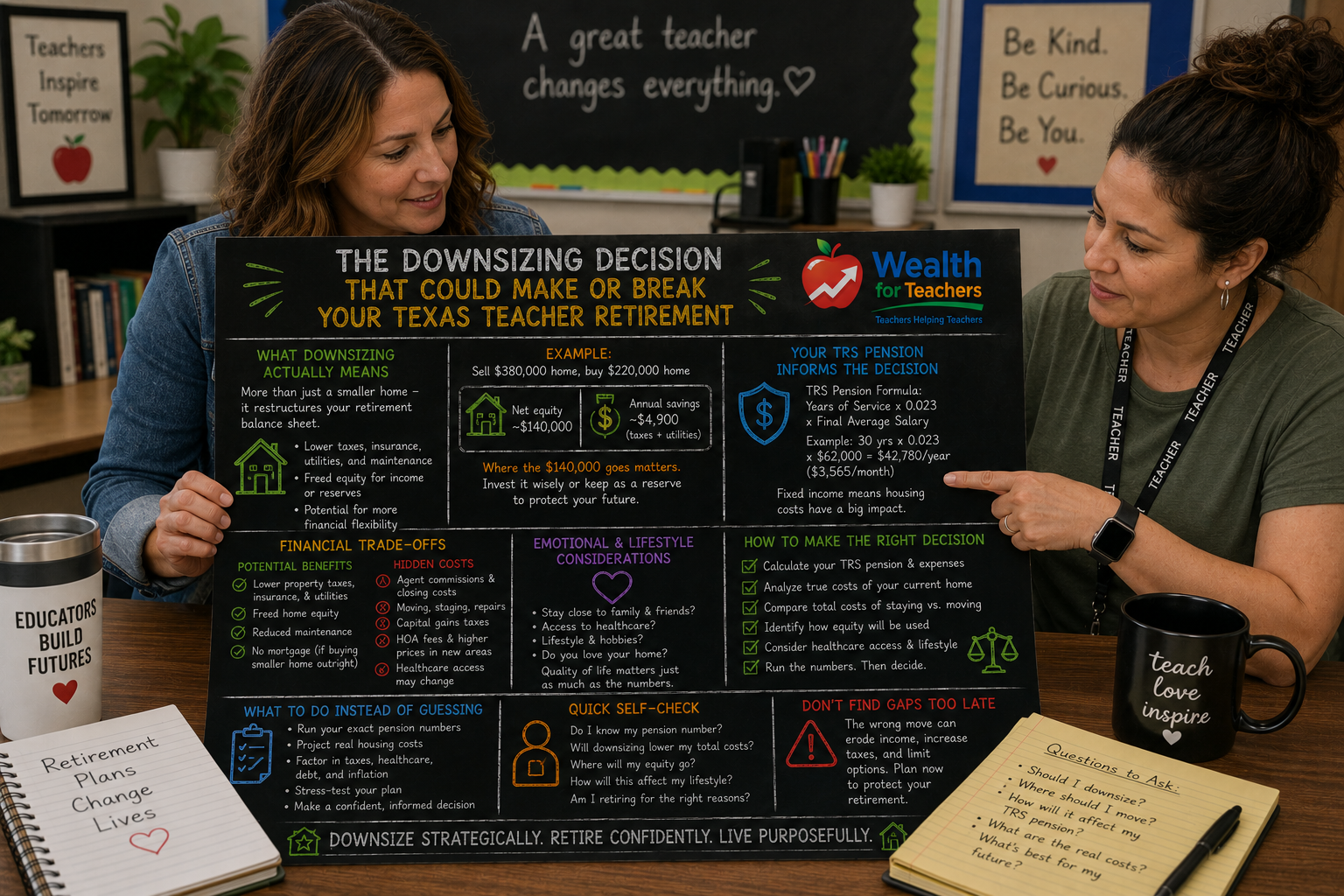

Most Texas teachers assume their TRS pension will carry them through retirement. The reality is different. With TRS providing only a baseline income, the way you coordinate TRS and IRA withdrawals—plus any 403(b) distributions—determines whether you maintain your lifestyle or face financial stress in retirement.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

The coordination challenge isn’t optional. Your TRS pension starts immediately when you retire, but your supplemental accounts follow different rules. IRAs and 403(b)s have required minimum distributions (RMDs) starting at age 73. Social Security begins between ages 62 and 70. Without proper sequencing, you could trigger unnecessary taxes, lose government benefits, or run out of money earlier than expected.

Texas teachers who successfully coordinate TRS and IRA strategies follow specific withdrawal sequences that minimize taxes while maximizing income longevity. Those who don’t often discover their mistakes when it’s too late to fix them. This comprehensive Texas Teacher Retirement Planning Guide will show you how to align all your retirement accounts correctly.

Most retirement coordination plans fail because they look good on paper but fall apart under real market conditions, unexpected expenses, or changes in tax laws. The strategies that work are stress-tested against multiple scenarios before implementation.

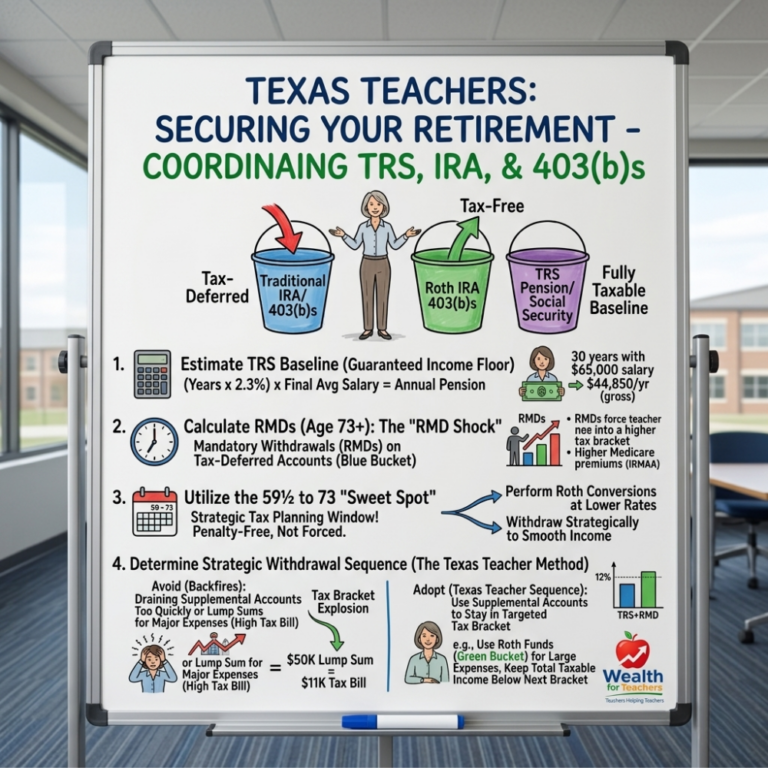

When you coordinate TRS and IRA withdrawals effectively, you’re managing three distinct tax buckets. Each bucket has different rules, different tax consequences, and different optimal timing.

Use the TRS calculator to estimate your pension and identify potential income gaps.

Your traditional IRA and 403(b) contributions reduced your taxable income when you made them. Every withdrawal is taxed as ordinary income. This bucket grows tax-free but creates a tax bill later. Most teachers accumulate significant balances here through years of contributing to school district 403(b) plans.

Roth accounts use after-tax dollars but grow and withdraw tax-free in retirement. This bucket provides tax-free income that doesn’t increase your Medicare premiums or affect Social Security taxation. Many teachers underestimate the value of tax-free income in retirement.

Your TRS pension is fully taxable as ordinary income. Social Security may be partially taxable depending on your total retirement income. These provide your baseline retirement income but push you into higher tax brackets when combined with IRA withdrawals.

The coordination challenge is optimizing withdrawals across all three buckets to minimize your lifetime tax bill while maintaining the income you need.

TRS pension payments begin immediately when you retire with the Rule of 80 or at age 65 with five years of service. Your pension amount is fixed: (Years of Service × 0.023) × Final Average Salary. A teacher with 30 years and a $65,000 final average salary receives $44,850 annually from TRS.

Your other accounts follow different schedules. You can access IRA and 403(b) funds penalty-free at age 59½. Required minimum distributions (RMDs) start at age 73, forcing withdrawals whether you need the money or not.

This timing mismatch creates opportunities and risks. Teachers who retire before age 59½ need bridge strategies to avoid early withdrawal penalties. Those who continue working past age 73 face complex RMD calculations while still employed.

The years between age 59½ and 73 offer the most flexibility. You can access all accounts penalty-free but aren’t forced to take distributions. This window allows strategic Roth conversions, tax-loss harvesting, and income smoothing that becomes impossible once RMDs begin.

The order you tap your accounts affects your total tax bill and account longevity. Most financial advisors recommend the traditional sequence: taxable accounts first, tax-deferred accounts second, tax-free accounts last. For Texas teachers, this approach often backfires.

Because your TRS pension provides baseline income, you can use a more sophisticated approach:

For example, a teacher with a $45,000 TRS pension might strategically withdraw $15,000 annually from traditional IRAs to stay in the 12% tax bracket, while using Roth funds to cover larger expenses without tax consequences.

Many teachers either ignore their supplemental accounts entirely or drain them too quickly. Both approaches create problems. Ignoring supplemental accounts means living on TRS alone, which rarely maintains pre-retirement lifestyle. Draining accounts too quickly eliminates the compound growth that extends account longevity.

Teachers often trigger massive tax bills by withdrawing large lump sums for major expenses. Taking $50,000 from an IRA for home repairs when you’re already in the 22% tax bracket creates an unnecessary $11,000 tax bill. Strategic planning spreads withdrawals across multiple years or uses different account types.

Large IRA withdrawals increase your modified adjusted gross income (MAGI), triggering higher Medicare Part B and Part D premiums. These Income-Related Monthly Adjustment Amounts (IRMAA) can add $2,000+ to your annual healthcare costs based on income from two years prior.

Teachers who delay all IRA and 403(b) withdrawals until age 73 face massive required distributions that push them into higher tax brackets permanently. A $500,000 IRA balance requires approximately $18,500 in annual RMDs at age 73, increasing each year.

RMDs fundamentally alter your retirement income strategy. Once they begin, you lose control over the timing and amount of your tax-deferred withdrawals. The IRS sets minimum distribution amounts based on your account balance and life expectancy.

Understanding RMD rules becomes critical for Texas teachers because these forced distributions often exceed what you need for living expenses, pushing you into higher tax brackets and increasing Medicare premiums.

The years between retirement and age 73 offer your best opportunity to optimize tax-deferred account balances. Strategic withdrawals during this window can:

A teacher who converts $20,000 annually from traditional to Roth IRAs between ages 65 and 73 can significantly reduce future RMD obligations while building tax-free income.

Successful coordination requires moving beyond simple withdrawal sequences to integrated income planning. Start by calculating your baseline income from TRS and Social Security, then determine how much additional income you need from supplemental accounts.

Your TRS pension creates an income floor—guaranteed money you receive regardless of market conditions. Your income ceiling represents your maximum comfortable standard of living. The gap between floor and ceiling determines how much you need from other accounts and when you need it.

Project your tax brackets in retirement considering TRS income, Social Security, and required distributions. Identify years where strategic withdrawals or Roth conversions can optimize your lifetime tax bill. Building retirement income streams that span multiple tax buckets provides the most flexibility.

Model your strategy under different conditions: market downturns, unexpected expenses, changes in tax laws, and varying longevity assumptions. Strategies that work in average conditions often fail during stress periods.

Your optimal coordination strategy depends on your specific circumstances. Here are the most common decision paths Texas teachers face:

When this applies: You meet TRS Rule of 80 requirements before age 65

Use the TRS calculator to estimate your pension and identify potential income gaps.