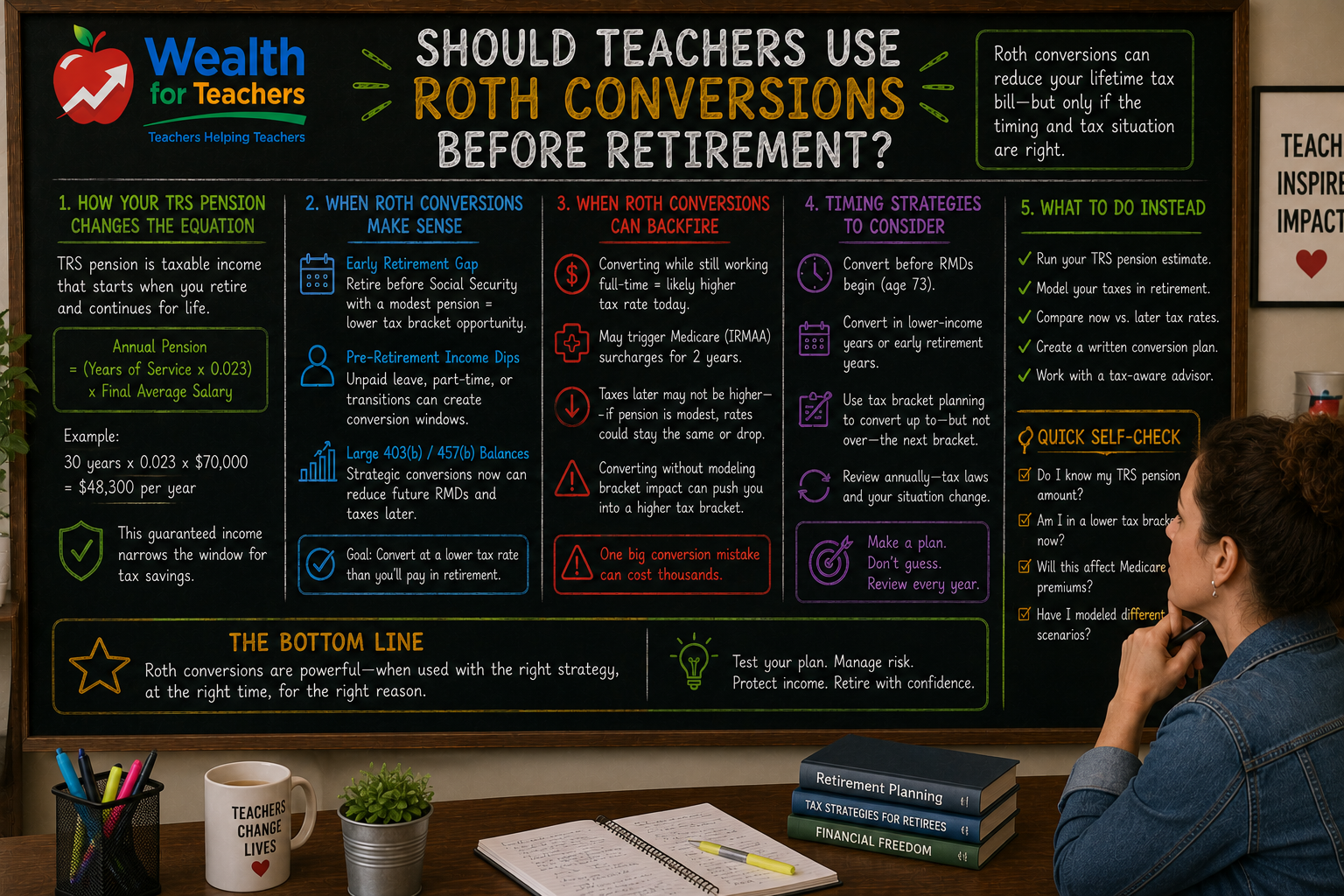

Should Teachers Use Roth Conversions Before Retirement?

Roth conversions can reduce taxes—but only if used correctly.

Many teachers overestimate TRS income. Learn what it really replaces.

Most Texas teachers assume their TRS pension will replace 70% to 80% of their working income. The reality? For many teachers, the TRS income replacement rate falls closer to 45% to 60% of their final salary.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

This gap between expectation and reality creates a dangerous blind spot. Teachers who count on TRS alone often discover too late that their pension covers basic expenses but leaves little room for the lifestyle they worked decades to afford.

Understanding your actual TRS income replacement rate isn’t just about numbers—it’s about making informed decisions while you still have time to adjust. Whether you need additional savings, should delay retirement, or can confidently retire as planned depends on knowing exactly what your pension will and won’t cover.

The Texas Teacher Retirement Planning Guide provides comprehensive strategies for addressing these income gaps, but first you need to understand the math behind TRS replacement rates.

Most retirement plans fail because they are never tested under real-world conditions. Teachers often make assumptions about TRS income replacement without calculating their specific situation or considering how inflation, healthcare costs, and lifestyle changes affect their actual retirement income needs.

Texas TRS uses a straightforward formula that many teachers don’t fully understand. Your annual pension equals your years of service multiplied by 2.3%, then multiplied by your final average salary.

Use the TRS calculator to estimate your pension and identify potential income gaps.

The formula: Annual Pension = (Years of Service × 0.023) × Final Average Salary

This means TRS provides a 2.3% income replacement rate for each year you teach. Work 30 years, and TRS theoretically replaces 69% of your final average salary. Work 25 years, and it replaces 57.5%.

But here’s where most teachers make a critical error: they assume their final average salary represents their actual working income. It doesn’t.

Your TRS final average salary is the highest 60 consecutive months of TRS-covered compensation. For most teachers, this includes base salary but excludes:

If you earn $65,000 in base salary but receive $8,000 annually in supplemental pay, your actual income is $73,000. However, your TRS calculation only uses the $65,000 base salary.

When you calculate TRS income replacement against your total working income—not just your TRS-covered salary—the percentages drop significantly.

Consider Maria, a Texas high school teacher with 28 years of service:

Maria loses nearly 10 percentage points of replacement income because TRS doesn’t cover her full earnings.

Based on TRS-covered salary only:

Based on total teacher income (including non-TRS compensation):

Three common misconceptions lead teachers to overestimate their TRS income replacement rate:

Teachers often forget about supplemental pay, summer income, and other earnings that won’t be replaced by TRS. These “extras” can represent 15% to 25% of total income for active teachers.

While some expenses decrease in retirement, others increase. Healthcare costs often rise significantly, and many teachers want to travel or pursue hobbies they couldn’t afford while teaching.

The common assumption that retirees need only 70% of working income doesn’t account for inflation over a 20-to-30-year retirement or the lifestyle goals that motivate teachers through decades of service.

TRS was designed as one leg of a three-legged retirement stool, alongside Social Security and personal savings. Many teachers focus exclusively on TRS and ignore the other components.

This oversight becomes critical when teachers realize their TRS pension, while reliable, doesn’t provide the financial flexibility they expected in retirement.

Understanding the income gap requires looking at specific scenarios. Here are three common situations:

James teaches and coaches football, earning $62,000 in base salary plus $12,000 in coaching stipends. His total income is $74,000, but TRS only covers the $62,000 base.

After 30 years:

Lisa earns $55,000 during the school year plus $6,000 teaching summer school. Her $61,000 total income drops to $38,500 with TRS after 30 years—a replacement rate of just 63.1%.

Robert receives $58,000 in base salary plus $8,000 as department head. After 32 years of service, his TRS pension of $42,688 replaces only 64.7% of his $66,000 actual income.

Several factors determine your actual TRS income replacement rate:

More years directly increase your replacement rate, but the relationship isn’t always linear with your retirement goals. Working additional years past 30 may not provide enough extra pension to justify delaying retirement.

Teachers with higher levels of non-TRS income face lower replacement rates. This creates a paradox: the most financially successful active teachers often face the largest retirement income gaps.

Teachers whose salaries grew significantly in their final years may find their TRS pension doesn’t keep pace with their lifestyle expectations, even if the replacement rate appears adequate.

TRS-Care costs and coverage gaps can effectively reduce your net retirement income. Creating retirement income strategies that account for healthcare inflation becomes crucial for maintaining purchasing power.

Recognizing the TRS income replacement reality allows you to make informed decisions:

Use your actual total income, not just TRS-covered salary, to determine what percentage TRS will replace. Include all supplemental pay, summer income, and additional compensation.

Determine the monthly dollar amount between your TRS pension and the income you want in retirement. This gap represents what you need from other sources.

Consider how coordinating TRS with IRAs and 403(b)s can help bridge your income

Use the TRS calculator to estimate your pension and identify potential income gaps.