How to Build a Guaranteed Income Floor as a Teacher

Stable income is the foundation of retirement security. Learn how to build it.

Annuities for Teachers: Making the Right Choice for Your Retirement As a Texas teacher, you’ve dedicated your career to educating others. Now it’s time to educate yourself about one of the most important financial decisions you’ll make: whether annuities belong in your retirement strategy. Texas teachers can also run a full pension estimate using the […]

As a Texas teacher, you’ve dedicated your career to educating others. Now it’s time to educate yourself about one of the most important financial decisions you’ll make: whether annuities belong in your retirement strategy.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

You already have a strong foundation with the Texas Teacher Retirement System (TRS). But many teachers wonder if adding an annuity can enhance their financial security. The answer isn’t simple – it depends on your specific situation, goals, and understanding of how these products actually work.

This guide cuts through the sales pitches and complex terminology to help you make an informed decision about annuities as a Texas educator.

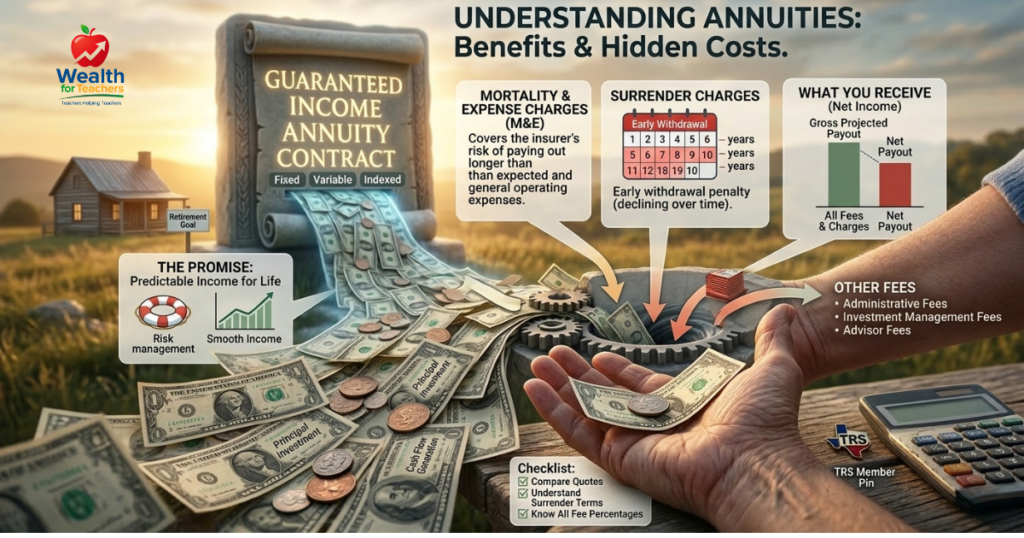

An annuity is essentially an insurance contract. You give an insurance company money (either as a lump sum or through payments), and in return, they promise to pay you income later – usually during retirement.

Use the TRS calculator to estimate your pension and identify potential income gaps.

Think of it as the opposite of life insurance. With life insurance, you pay premiums and the company pays a benefit when you die. With annuities, you pay money upfront and the company pays you while you’re alive.

Sounds simple, right? Unfortunately, the annuity industry has created dozens of variations, each with different features, fees, and complexity levels. This complexity isn’t accidental – it makes it harder for you to compare products and understand what you’re really buying.

All annuities make one core promise: guaranteed income. The insurance company takes on the investment risk and guarantees you’ll receive payments for a certain period or for life.

This guarantee comes at a cost. Insurance companies aren’t charities – they need to make a profit, pay their employees, fund their marketing, and build reserves for claims. All of these costs come out of your returns.

Teachers are prime targets for annuity sales, and it’s not because these products are perfect for educators. Here’s why you see so many annuity seminars and mailers aimed at teachers:

Teachers have predictable paychecks and stable employment. This makes you attractive customers who are likely to keep making payments and less likely to surrender policies early.

Most teacher preparation programs don’t include comprehensive financial education. This knowledge gap makes it easier for salespeople to position complex products as solutions to problems you may not fully understand.

Teachers often worry about retirement security, especially given the political uncertainty around pension systems. Annuity salespeople exploit this fear by positioning their products as “safe” alternatives or supplements to your pension.

Many school districts allow insurance companies to offer annuities through 403(b) plans. This gives salespeople direct access to teachers and an air of institutional approval.

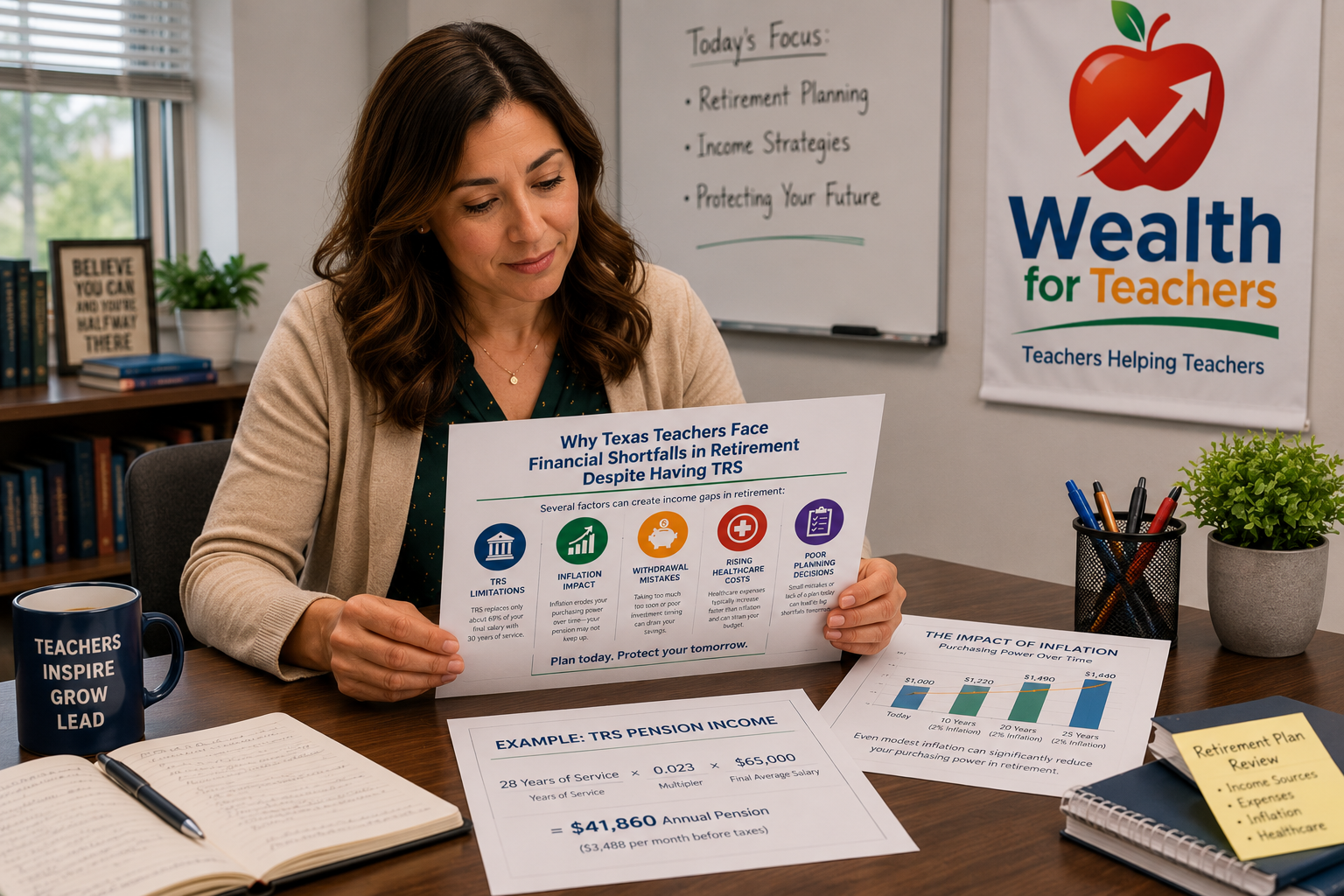

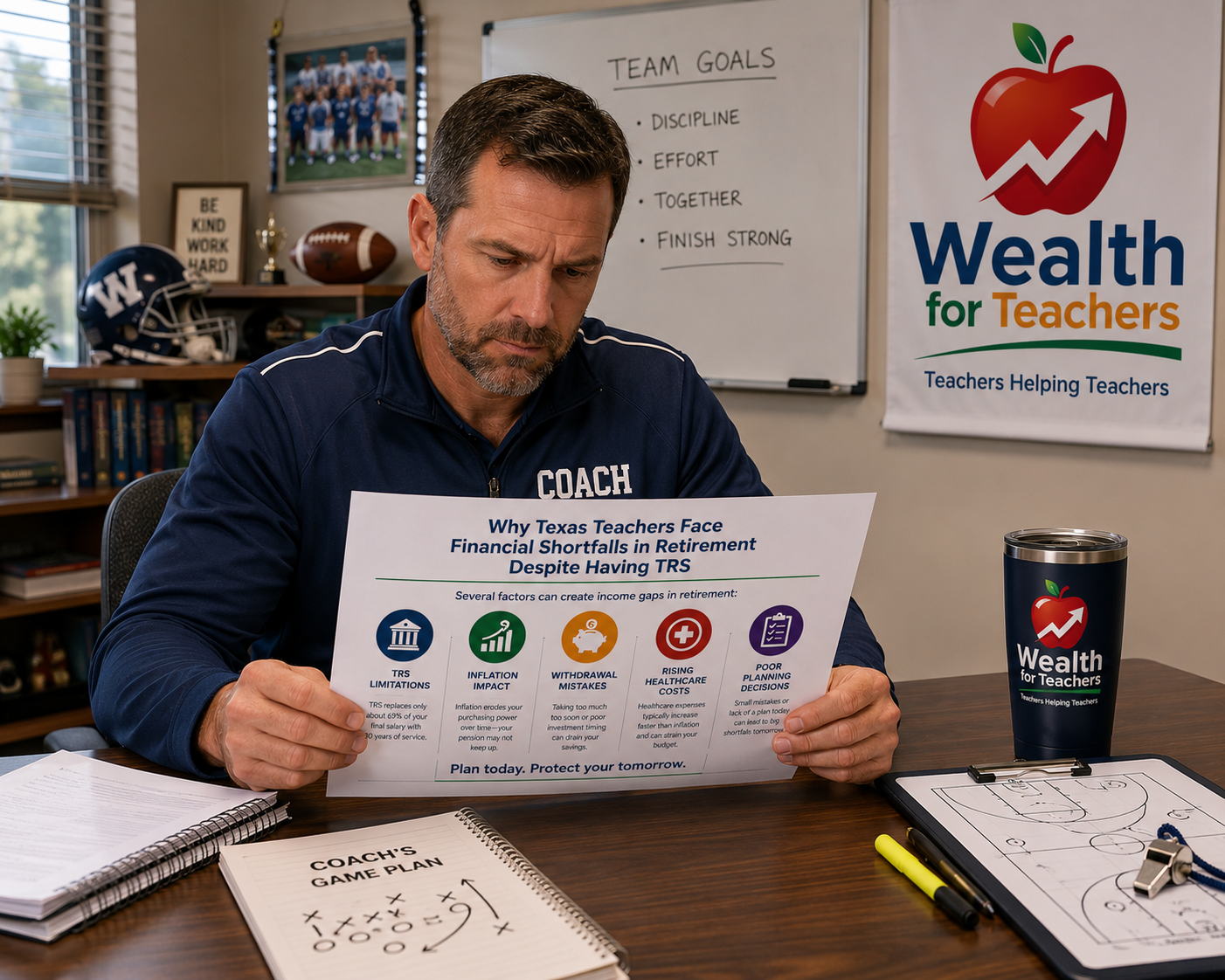

Before considering any annuity, you need to understand the retirement benefits you already have as a Texas teacher. The Texas Teacher Retirement System provides a defined benefit pension that’s actually quite generous compared to what most private sector workers receive.

Texas TRS uses a straightforward formula with a flat 2.3% multiplier per year of service:

Annual Pension = (Years of Service × 0.023) × Final Average Salary

Let’s look at an example to see how this works:

Example only – assumptions stated:

• Years of Service: 25 years

• Final Average Salary: $65,000

Benefit % = 25 years × 2.3% = 57.5%

Annual Pension = $65,000 × 57.5% = $37,375

This pension is guaranteed for life and includes annual cost-of-living adjustments when the system’s funding allows.

Your TRS membership also includes:

These benefits have significant value that annuity salespeople rarely mention when comparing their products to your “inadequate” pension. Before making retirement income decisions, it’s important to understand why Teachers Retire Asset-rich but Income Poor.

Understanding the different types of annuities helps you evaluate any sales pitch more effectively.

These offer a guaranteed interest rate for a specific period. They’re the simplest type of annuity, but the rates are typically low – often barely keeping pace with inflation.

Fixed annuities might make sense if you’re extremely conservative and nearing retirement, but they’re rarely the best choice for teachers with decades left in their careers.

Variable annuities let you invest in mutual fund-like accounts within the insurance contract. Your returns depend on how these investments perform.

The problem? Variable annuities typically charge high fees that can easily exceed 2-3% annually. These fees make it very difficult to build wealth over time.

These are heavily marketed to teachers. FIAs promise to capture some stock market gains while protecting your principal. They sound perfect, but the reality is more complicated.

FIAs use complex formulas involving caps, spreads, and participation rates that limit your upside potential. The insurance company keeps most of the market gains while giving you a small portion.

You pay a lump sum and immediately start receiving payments. These can make sense in very specific situations, but they’re rarely appropriate for teachers who are still working.

Annuity fees are often hidden in complex terminology and buried in lengthy contracts. Here are the costs you need to understand:

This covers the insurance company’s profit and the cost of guarantees. Typical charges range from 1.0% to 1.5% annually.

These cover record-keeping and customer service, usually 0.1% to 0.3% per year.

For variable annuities, each investment option charges its own fee, typically 0.5% to 1.5% annually.

Optional features like guaranteed minimum income benefits can cost an additional 0.5% to 1.5% per year.

If you need to access your money early, you’ll face surrender charges that can be 7-10% in the first year, declining over 7-10 years.

Total annual costs can easily exceed 3% per year. Over 20-30 years, these fees can consume hundreds of thousands of dollars in potential returns.

Despite their drawbacks, annuities aren’t universally bad. There are specific situations where they might be appropriate for teachers:

If you’re close to retirement and want guaranteed income beyond your TRS pension, an immediate annuity might make sense for a portion of your savings.

If you’ve maximized contributions to your 403(b) and IRA and still want tax-deferred growth, a low-cost annuity could be considered.

If market fluctuations cause you to make poor investment decisions (like selling during downturns), the guarantees in an annuity might prevent costly mistakes.

While education is preferable, if you absolutely refuse to learn about investing and have significant assets, a simple annuity might be better than making poor investment choices.

Recognizing these warning signs can save you from costly mistakes:

For most Texas teachers, there are better alternatives to annuities for building retirement wealth:

Focus on low-cost index funds in your 403(b) plan. Look for options with expense ratios below 0.5%. If your plan doesn’t offer good options, advocate with your district for better choices.

A Roth IRA gives you access to the entire investment universe, usually with much lower costs than annuities. You can invest in broad market index funds and pay fees of 0.1% or less.

Before investing in any retirement account, make sure you have 3-6 months of expenses saved in a high-yield savings account. This prevents you from needing to access retirement funds early.

If your district offers a 457(b) plan, it can provide additional tax-deferred savings opportunities with more flexible withdrawal rules than 403(b) plans.

A portfolio of low-cost index funds covering the total stock market and bonds is likely to outperform complex annuity products over the long term, especially after fees.

If you need guidance, work with a fee-only financial advisor who doesn’t sell annuities. They can help you create a comprehensive plan without the conflicts of interest that come with commission-based sales. You should also understand why TRS alone may not be enough for retirement.

A: Yes, your TRS pension is very likely to be there. While the system faces funding challenges, Texas has a strong history of supporting TRS and making necessary contributions. Pensions are also protected by law and the Texas Constitution. Don’t let fear-mongering drive you toward expensive annuities.

A: Every teacher’s situation is different. What works for your colleague may not work for you. Also, people who buy annuities often defend their decision even when it wasn’t optimal, because admitting a mistake is psychologically difficult. Do your own research.

A: No. Any illustration showing high returns in an annuity is likely misleading. Fixed index annuities, in particular, use complex calculations that severely limit your upside potential. If it sounds too good to be true, it probably is.

A: At 55, you still have a long investment horizon. While annuities can provide guarantees, the high fees often make them a poor choice for long-term wealth building. Consider a more conservative investment mix instead of locking into expensive guarantees.

A: First, look carefully – many plans have low-cost options that aren’t aggressively marketed. If your plan truly only offers expensive annuities, consider contributing only enough to get any employer match, then maximize a Roth IRA with better investment options.

A: It depends on how long you’ve owned it. Most annuities have surrender periods of 7-10 years with declining penalties. After the surrender period, you can usually withdraw your money, though you may owe taxes. For newer purchases, you might have a “free look” period of 10-30 days to cancel without penalty.

A: Insurance company ratings indicate the company’s ability to pay claims, but they don’t address whether the product is good for you. A highly-rated company can still sell expensive, underperforming products. Focus on the product features and costs, not just the company’s rating.

A: No. Your 403(b) and IRA already provide tax-deferred growth with much lower costs and better investment options. Non-qualified annuities (outside retirement accounts) do offer tax deferral, but the high fees usually outweigh this benefit for most people.

Making smart financial decisions as a teacher means cutting through the sales pitches and focusing on what actually builds long-term wealth. Your TRS pension provides a solid foundation – now build on it with low-cost, diversified investments rather than expensive insurance products designed to benefit the company selling them more than you.

You should also understand How Inflation Impacts Teacher Retirement Income.

Use the TRS calculator to estimate your pension and identify potential income gaps.