How to Build a Guaranteed Income Floor as a Teacher

Stable income is the foundation of retirement security. Learn how to build it.

Teacher Retirement Income Plan: A Complete Guide for Texas Educators Planning your financial future as an educator requires understanding how your teacher retirement income plan actually works. Unlike private sector employees who rely heavily on 401(k) plans, teachers have access to pension systems that provide guaranteed monthly income for life after retirement. Texas teachers can […]

Planning your financial future as an educator requires understanding how your teacher retirement income plan actually works. Unlike private sector employees who rely heavily on 401(k) plans, teachers have access to pension systems that provide guaranteed monthly income for life after retirement.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

For Texas educators, the Teacher Retirement System of Texas (TRS) serves as the foundation of your retirement security. However, many teachers don’t fully understand how their pension benefits are calculated or what additional steps they should take to ensure financial comfort in retirement.

This comprehensive guide breaks down everything you need to know about building a solid teacher retirement income plan, from understanding your TRS pension benefits to exploring supplemental savings strategies that can enhance your financial security.

The Texas Teacher Retirement System operates as a defined benefit pension plan, meaning your retirement income is predetermined based on a specific formula rather than investment performance. This provides predictable, guaranteed monthly payments for the rest of your life after you retire.

Use the TRS calculator to estimate your pension and identify potential income gaps.

Your TRS pension serves as the cornerstone of your teacher retirement income plan. Unlike 401(k) plans where you bear the investment risk, TRS manages the investments and guarantees your benefit amount based on your years of service and salary history.

The system covers all public school employees in Texas, including teachers, administrators, counselors, and support staff. You become vested in the system after five years of service, meaning you’ve earned the right to receive pension benefits when you reach retirement age.

TRS also provides additional benefits beyond the basic pension:

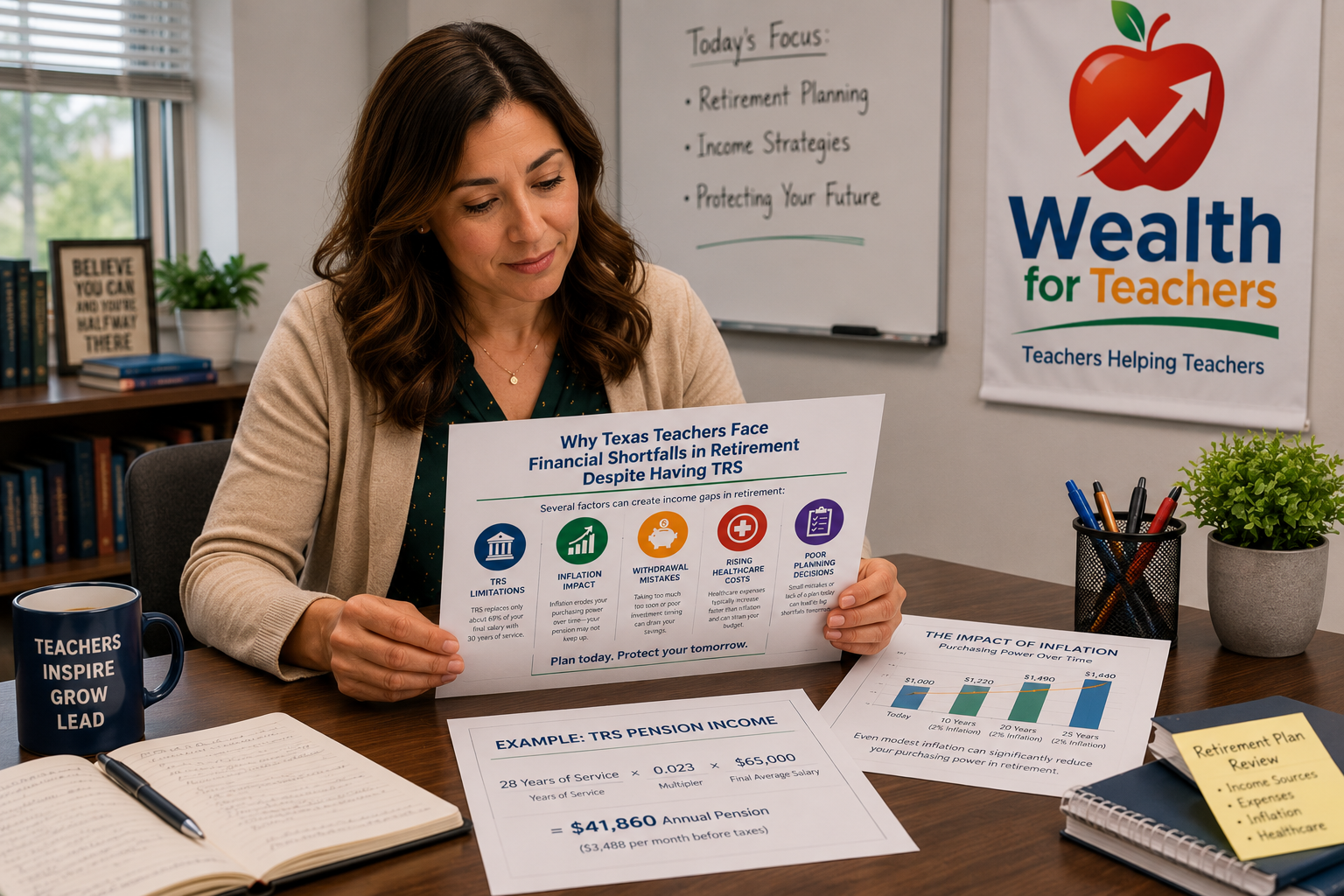

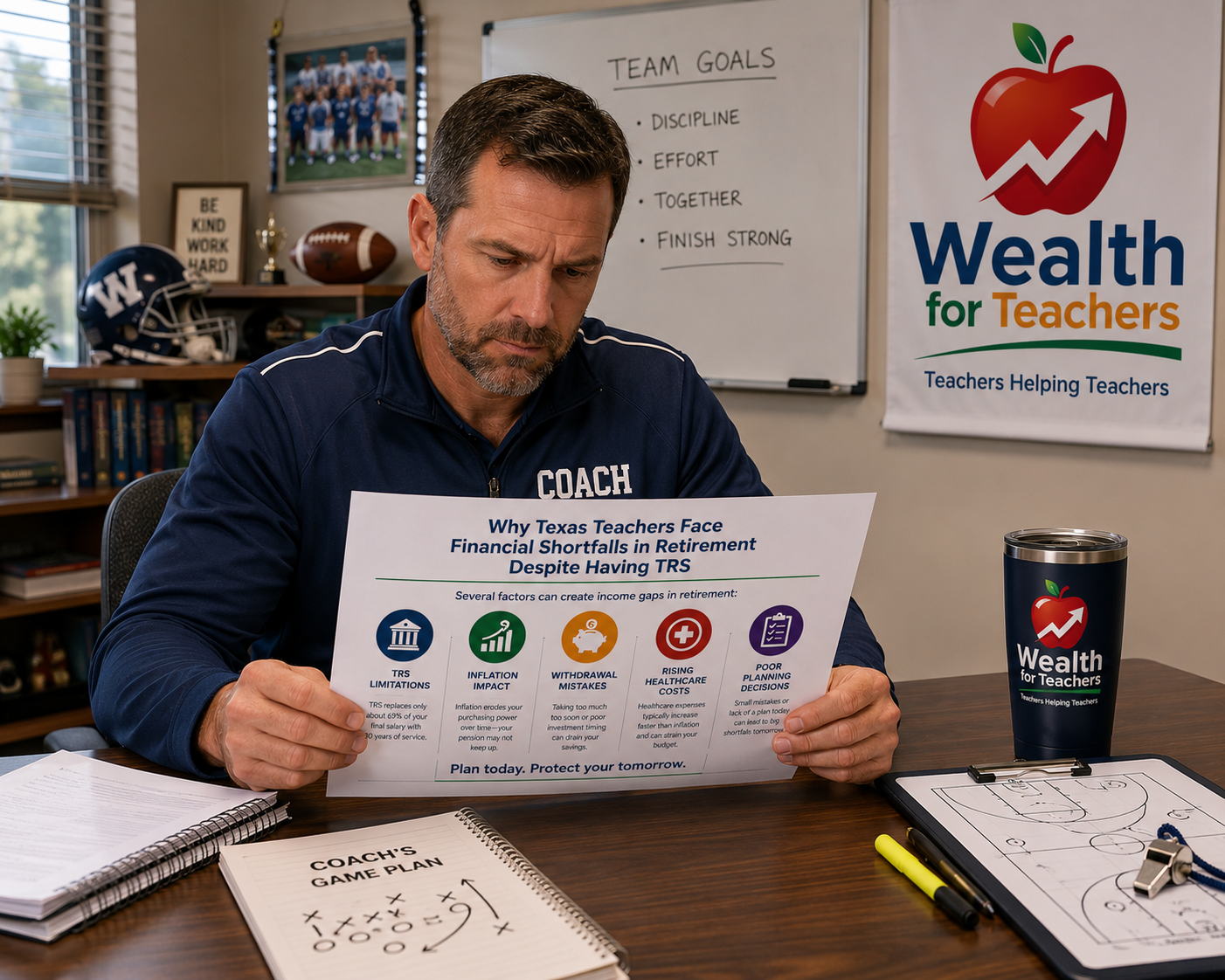

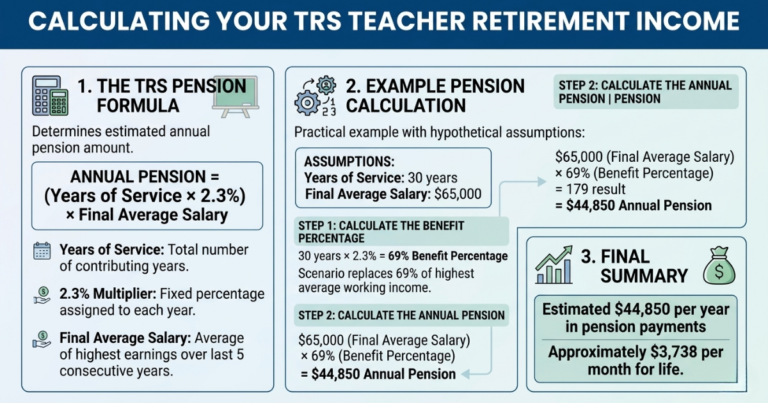

Understanding how TRS calculates your pension benefit is crucial for effective retirement planning. The formula is straightforward and uses a flat multiplier of 2.3% for each year of service credit.

The basic TRS pension formula is:

Annual Pension = (Years of Service × 2.3%) × Final Average Salary

Your Final Average Salary represents the highest consecutive five years of your career. TRS takes your five highest-paying years and calculates the average to determine this amount.

Let’s look at a practical example to illustrate how this works:

Example only – Assumptions:

Step 1: Calculate benefit percentage

Benefit % = 30 years × 2.3% = 69%

Step 2: Calculate annual pension

Annual Pension = $65,000 × 69% = $44,850

This teacher would receive $44,850 per year, or approximately $3,738 per month, for life.

The flat 2.3% multiplier applies consistently throughout your career. Whether you’re in your first year or your thirtieth year of service, each additional year adds exactly 2.3% to your benefit percentage.

TRS offers several retirement options, but understanding when you can retire with full benefits is essential for your teacher retirement income plan. Also, You may also want to understand the differences between TRS Tier 1 vs Tier 2 vs Tier 3.

You can retire with full, unreduced benefits under these conditions:

You can retire before meeting full retirement requirements, but your benefits will be permanently reduced:

The reduction for early retirement is significant. For example, retiring at age 55 with 25 years of service would result in a 25% permanent reduction in your monthly pension benefit.

While your TRS pension provides a solid foundation, most financial experts recommend supplementing it with additional savings to maintain your pre-retirement lifestyle.

Texas teachers have access to 403(b) plans, which function similarly to 401(k) plans in the private sector. These tax-advantaged accounts allow you to save additional money for retirement.

Key benefits of 403(b) plans include:

Teachers can also contribute to IRAs to further enhance their retirement savings:

Roth IRAs can be particularly valuable for teachers because they provide tax-free income in retirement, which can help manage your overall tax burden when combined with your TRS pension. Also, You may also want to understand should you roll your TRS into an IRA if you leave teaching?

A comprehensive teacher retirement income plan typically includes:

The relationship between teacher pensions and Social Security can be complex and varies significantly depending on where you worked throughout your career.

Texas teachers who only work in TRS-covered positions do not pay into Social Security for their teaching income. However, you may still be eligible for Social Security benefits if you:

If you receive both a TRS pension and Social Security benefits, your Social Security benefits may be reduced due to the Windfall Elimination Provision. This federal law can reduce Social Security benefits for people who receive pensions from employment where they didn’t pay Social Security taxes.

Understanding how WEP might affect your benefits is crucial when planning your overall retirement income strategy.

Healthcare costs represent one of the largest expenses in retirement, making it a critical component of your teacher retirement income plan.

Texas teachers may be eligible for TRS-Care, the health insurance program for TRS retirees. Eligibility requirements include:

TRS-Care provides several plan options with varying coverage levels and costs. Premium costs are based on your years of service and retirement date.

When you become eligible for Medicare at age 65, TRS-Care coordinates with Medicare to provide comprehensive coverage. Understanding how these programs work together helps you budget for healthcare costs in retirement.

Many teachers make critical errors when planning their retirement income strategy. Avoiding these mistakes can significantly improve your financial security in retirement.

Many teachers assume their expenses will decrease dramatically in retirement. While some costs may decline, others like healthcare often increase. A realistic budget should account for:

The temptation to retire as soon as you’re eligible can be strong, but retiring before you qualify for full benefits can permanently reduce your monthly income. Each year you work beyond minimum eligibility typically increases your pension benefit.

Relying solely on your TRS pension may not provide enough income to maintain your desired lifestyle. Starting supplemental savings early in your career allows compound interest to work in your favor.

Failing to properly designate beneficiaries or understand survivor benefit options can leave your spouse or family without adequate income if something happens to you.

Building a successful teacher retirement income plan requires proactive steps throughout your career. Here’s what you should do to maximize your retirement security:

Even if you’re years away from retirement, understanding your benefits and starting supplemental savings early makes a tremendous difference. The power of compound interest means that small contributions made early in your career can grow significantly over time.

Since your pension is based on your highest five consecutive years of earnings, consider strategies to increase your salary during those peak earning years:

Take advantage of tax-advantaged savings opportunities:

Develop a detailed plan that includes:

Your teacher retirement income plan should evolve as your circumstances change:

Consider working with a financial advisor who understands teacher retirement benefits. They can help you:

Also read, the biggest TRS mistakes that Teachers make at 50+.

Your pension replacement ratio depends on your years of service and final salary. With 30 years of service, your TRS pension replaces about 69% of your final average salary (30 years × 2.3% = 69%). Most financial experts recommend replacing 70-80% of pre-retirement income for a comfortable retirement, so you may need additional savings to bridge the gap.

Yes, but there are restrictions. You can work in non-TRS covered positions without affecting your pension. If you return to work in a TRS-covered position, you must wait at least 12 months after retirement, and there are limits on how much you can earn without suspending your pension benefits.

If you’re vested (five years of service), you can leave your contributions in TRS and claim your pension when you reach retirement age. Your benefit will be based on your years of service and salary history at the time you left. You can also choose to withdraw your contributions, but you’ll forfeit any employer contributions and future pension benefits.

TRS pension benefits may be subject to division in divorce proceedings. A Qualified Domestic Relations Order (QDRO) can award a portion of your pension to your former spouse. It’s important to understand these implications and work with legal counsel to protect your retirement security during divorce proceedings.

This decision involves weighing higher monthly payments during your lifetime against providing continued income for your spouse after your death. The choice depends on your spouse’s age, health, other income sources, and life insurance coverage. Many couples benefit from consulting a financial advisor to model different scenarios.

A common guideline is to save 10-15% of your income for retirement beyond your pension contributions. If your district offers matching contributions to your 403(b), prioritize contributing enough to receive the full match first. Then gradually increase your contributions, especially when you receive salary increases.

Start planning as early as possible, ideally within your first few years of teaching. Even if retirement seems far away, understanding your benefits and beginning supplemental savings early gives you more options and financial security later. The earlier you start, the less you need to save each month to reach your retirement goals.

TRS benefits are protected by the Texas Constitution, which prohibits the reduction of pension benefits once earned. While the system faces long-term funding challenges, these typically result in changes for future employees rather than reductions in benefits for current members and retirees. However, staying informed about system health and legislative changes is always wise.

Creating a solid teacher retirement income plan requires understanding your TRS pension benefits, planning for additional savings, and making informed decisions throughout your career. By taking proactive steps and avoiding common mistakes, you can build the financial security needed for a comfortable retirement after your years of dedicated service to education.

Use the TRS calculator to estimate your pension and identify potential income gaps.