Is Early TRS Retirement Ever a Smart Move?

Early TRS Retirement: Understanding Your Options as a Texas Teacher Thinking about leaving the classroom before you reach full retirement eligibility? You’re not alone. Many Texas teachers consi...

TRS Retirement Benefits for Texas Teachers: Your Complete Guide to Securing Financial Freedom As a Texas teacher, you’ve dedicated your career to educating the next generation. Now it’s time to focus on securing your own future through the Teacher Retirement System of Texas (TRS). Understanding your TRS retirement benefits isn’t just important—it’s essential for building […]

As a Texas teacher, you’ve dedicated your career to educating the next generation. Now it’s time to focus on securing your own future through the Teacher Retirement System of Texas (TRS). Understanding your TRS retirement benefits isn’t just important—it’s essential for building the retirement you deserve after years of service in the classroom.

Whether you’re a new teacher just starting your career or a veteran educator planning your retirement timeline, knowing how TRS works can make the difference between a comfortable retirement and financial uncertainty. The good news is that TRS provides one of the most comprehensive retirement benefit packages available to public employees in Texas.

Teacher Retirement System (TRS) Guide

The Teacher Retirement System of Texas serves over 1.6 million active and retired public education employees. As a TRS member, you’re part of a defined benefit pension plan that provides guaranteed monthly payments for life after you retire.

Get Your Free Guide 10 Money Mistakes Teachers Make

TRS membership is automatic for all Texas public school employees, including:

Your TRS benefits consist of three main components: the pension plan, supplemental savings options, and retiree healthcare coverage. Each plays a crucial role in your overall retirement security.

Most Texas teachers don’t pay into Social Security, which means TRS serves as your primary retirement income source. This makes understanding your benefits even more critical since you won’t have Social Security as a backup.

However, this also means your TRS benefits are designed to be more comprehensive than typical pension plans. The system recognizes that teachers need robust retirement security without Social Security benefits.

Your TRS pension forms the foundation of your retirement income. This defined benefit plan guarantees monthly payments based on your years of service and salary history, providing predictable income you can count on throughout retirement.

The TRS pension includes several valuable features that protect your financial future:

You can retire with full TRS benefits under several scenarios:

Meeting these requirements ensures you receive your full pension benefit without any reductions for early retirement.

Beyond your pension, TRS offers supplemental retirement savings through the 403(b) program. This voluntary program allows you to save additional money for retirement on a tax-advantaged basis.

The TRS 403(b) program provides several advantages:

Contributing to your 403(b) is especially important since most Texas teachers don’t have Social Security benefits. Every dollar you save now compounds over time, potentially adding thousands to your annual retirement income.

Consider these approaches to maximize your 403(b) benefits:

For detailed guidance on 403(b) retirement plans for teachers, understanding your investment options and contribution strategies is essential for long-term success.

TRS-ActiveCare provides crucial healthcare coverage for retired teachers. Since Medicare doesn’t begin until age 65, having access to affordable healthcare through TRS bridges this critical gap for early retirees.

Retired teachers can choose from several healthcare plans:

The state contributes toward your healthcare premiums, making TRS-ActiveCare significantly more affordable than individual insurance policies. This benefit alone can save thousands of dollars annually.

When planning for retirement, factor healthcare costs into your budget. Consider:

Understanding TRS vesting is crucial for protecting your retirement benefits. Vesting determines when you earn the right to receive pension benefits, even if you leave teaching before retirement.

TRS uses a cliff vesting schedule:

Once you’re vested, you’ve earned the right to receive pension benefits at retirement age, even if you leave teaching. However, your benefit amount depends on your final salary and total service credit.

Service credit determines both your vesting status and benefit amount. You earn service credit through:

Maximizing your service credit can significantly impact your retirement income. Each additional year of service increases your pension benefit.

Your TRS pension amount depends on three key factors: your years of service credit, your highest average salary, and the benefit multiplier.

The basic formula is: Years of Service Credit × Highest Average Salary × Benefit Multiplier = Annual Pension

Here’s how each component works:

This includes all creditable service in TRS-covered employment. The more years you work, the higher your benefit. Teachers with 30+ years of service typically see the most significant benefits.

TRS calculates your benefit using your five highest consecutive years of salary. This encourages teachers to work their highest-earning years, typically later in their careers.

The multiplier with years of service:

Consider a teacher with 20 years of service and a highest average salary of $60,000:

Consider a teacher with 30 years of service and a highest average salary of $60,000:

This calculation shows why reaching 20 and 30 years of service creates significant benefit improvements.

Smart planning throughout your career can dramatically increase your retirement benefits. Here are proven strategies Texas teachers use to optimize their TRS benefits.

Consider these long-term approaches:

Since TRS uses your five highest consecutive years, strategic career moves in your final decade can significantly boost benefits. Consider:

The timing of your retirement affects both your pension amount and healthcare coverage. Consider:

Understanding Texas teacher retirement age requirements helps you plan the optimal timing for your specific situation.

Many Texas teachers supplement their TRS benefits through:

Learning from others’ mistakes can protect your retirement security. Here are the most common TRS planning errors and how to avoid them.

Many teachers fail to budget adequately for healthcare in retirement. Healthcare costs typically increase with age, and even with TRS-ActiveCare, you’ll have premium costs and out-of-pocket expenses.

Plan for healthcare expenses by:

Teachers who leave before reaching five years of service forfeit all pension benefits. If you’re considering leaving teaching, understand the financial impact on your retirement security.

Without Social Security, your TRS pension and personal savings become even more critical. Teachers who don’t participate in supplemental savings often struggle to maintain their lifestyle in retirement.

Retiring too early can result in benefit reductions, while retiring too late might mean missing opportunities for other activities. Plan your retirement timing carefully based on your financial needs and personal goals.

Now that you understand common mistakes, here’s your action plan for maximizing your TRS retirement benefits:

Even if retirement seems far away, early planning gives you more options and better outcomes. Begin by:

Make strategic career decisions that benefit both your current situation and future retirement:

Diversify your retirement income beyond just your TRS pension:

TRS rules and benefits can change over time. Stay current by:

Consider working with financial professionals who understand teacher retirement benefits. They can help with:

For more detailed planning strategies, explore our comprehensive guide on teacher retirement planning to develop a personalized approach to your financial future.

If you’re vested (5+ years of service), you keep your pension benefits but can’t collect them until you reach retirement age. If you’re not vested, you can withdraw your contributions plus interest. However, withdrawing contributions means giving up all future pension benefits, so consider this decision carefully.

Most Texas teachers don’t pay into Social Security, so they won’t receive Social Security benefits based on their teaching career. However, if you worked in other jobs where you paid Social Security taxes, you might be eligible for those benefits. Be aware of potential offsets like the Windfall Elimination Provision that could reduce Social Security benefits.

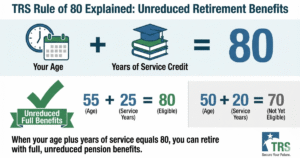

The Rule of 80 allows you to retire with full benefits when your age plus years of TRS service credit equals 80. For example, if you’re 55 years old with 25 years of service, you meet the Rule of 80 (55 + 25 = 80). This allows unreduced retirement benefits without waiting until age 65.

You may be able to purchase out-of-state service credit to increase your TRS benefits. This process involves paying the actuarial cost of adding those years to your TRS record. Contact TRS to determine if your previous teaching qualifies and get cost estimates for purchasing this service credit.

Financial experts typically recommend saving 10-15% of your income for retirement. Since Texas teachers often don’t have Social Security, consider contributing at least enough to get any employer match, then work toward higher contribution rates. The 2024 contribution limit is $23,000, with an additional $7,500 catch-up contribution allowed if you’re 50 or older.

Yes, but with restrictions. TRS retirees can work part-time (less than half-time) without affecting benefits. Full-time employment may require suspension of pension payments. There are also specific rules about when you can return to work and for how long. Consult TRS guidelines or speak with a counselor before making employment decisions after retirement.

TRS benefits are protected by the Texas Constitution, making them very secure. The system is regularly monitored and has maintained stable funding through various market conditions. According to the TRS Comprehensive Annual Financial Report, the system continues to meet its obligations to retirees while building long-term sustainability.

TRS doesn’t typically offer lump sum payments for the pension portion of your benefits. Your pension provides guaranteed monthly income for life, which offers security that lump sums can’t match. However, you can access your 403(b) account as either monthly payments or lump sums, giving you flexibility in how you structure your retirement income.

Ready to take control of your retirement planning? Our comprehensive resources and expert guidance can help you maximize your TRS benefits and build the retirement you deserve. Every year you wait to optimize your retirement strategy could cost you thousands in future benefits.

Don’t let uncertainty about your retirement benefits keep you awake at night. Get personalized guidance on maximizing your TRS benefits and building comprehensive retirement security.

Get Your Free TRS Retirement using or Calculator