Is Early TRS Retirement Ever a Smart Move?

Early TRS Retirement: Understanding Your Options as a Texas Teacher Thinking about leaving the classroom before you reach full retirement eligibility? You’re not alone. Many Texas teachers consi...

TRS Retirement Planning Mistakes for Texas Teachers Planning for retirement as a Texas teacher involves navigating the Teacher Retirement System (TRS), but many educators make costly mistakes along the way. These TRS retirement planning mistakes can significantly impact your financial security in your golden years, potentially costing you thousands of dollars in lost benefits. As […]

Planning for retirement as a Texas teacher involves navigating the Teacher Retirement System (TRS), but many educators make costly mistakes along the way. These TRS retirement planning mistakes can significantly impact your financial security in your golden years, potentially costing you thousands of dollars in lost benefits.

As a Texas teacher, you’ve dedicated your career to educating others. Now it’s time to educate yourself about avoiding the most common retirement planning pitfalls. Understanding these mistakes early can help you make informed decisions that protect your financial future and maximize your TRS benefits.

Texas Teacher Retirement Guide

Texas teachers often make critical errors when planning for retirement that can cost them dearly. These mistakes typically stem from a lack of understanding about how TRS works or failing to plan far enough in advance.

Get Your Free Guide 10 Monet Mistakes Teachers Make.

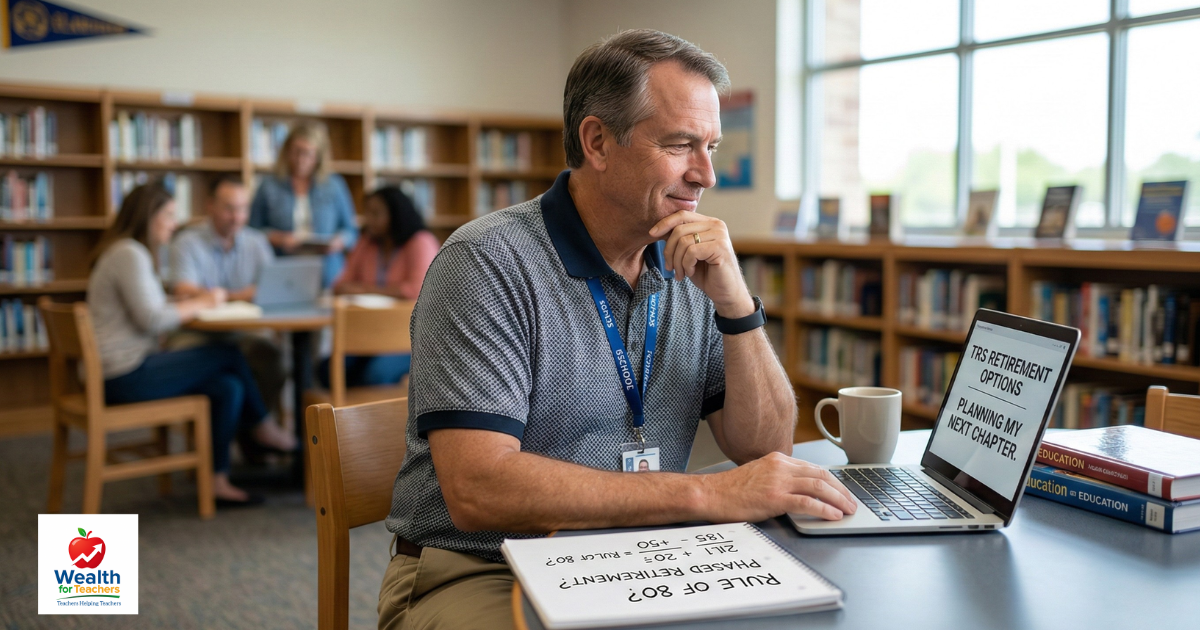

One of the most significant mistakes Texas teachers make is not fully grasping the Rule of 80. This rule allows you to retire without penalty when your age plus years of service credit equal 80 or more. Many teachers assume they need to work until age 65, missing opportunities for earlier retirement.

The Rule of 80 can dramatically change your retirement timeline. A teacher who starts at age 22 could potentially retire at 51 with 29 years of service (22 + 29 = 51). However, many teachers don’t realize this possibility exists or fail to plan accordingly.

Another common mistake is not understanding the five-year vesting requirement. Teachers who leave the profession before completing five years of creditable service forfeit their employer contributions and retirement benefits. This mistake is particularly costly for career changers who don’t realize the long-term implications.

Some teachers mistakenly believe they can work part-time or take breaks without affecting their vesting timeline. However, TRS has specific rules about what constitutes creditable service, and interruptions can delay your vesting date significantly.

Service credit forms the foundation of your TRS retirement benefits, yet many teachers make errors that reduce their total creditable service or delay their retirement eligibility.

Texas teachers with military service often overlook the opportunity to purchase military service credit through TRS. This purchased service credit counts toward both your years of service and benefit calculations, potentially allowing for earlier retirement and higher monthly benefits.

The cost to purchase military service credit is typically much lower than the long-term benefit increase it provides. However, many teachers either don’t know about this option or wait too long to take advantage of it.

Teachers who worked in other states before coming to Texas may be able to purchase out-of-state service credit. This process involves working with both TRS and your previous state’s retirement system, but it can significantly boost your retirement benefits.

The application process can be complex, and many teachers give up or procrastinate. However, the long-term financial benefits often justify the effort required to navigate the paperwork and requirements.

Many teachers never review their TRS service records for accuracy. Errors in your employment history, salary information, or service credit calculations can cost you money in retirement. These mistakes often go unnoticed until it’s too late to correct them easily.

Regular review of your TRS account can help identify discrepancies early. Issues such as missing employment periods, incorrect salary information, or uncredited substitute teaching can all impact your final benefit calculation.

When you retire can be just as important as how much service credit you have. Poor timing decisions represent some of the most expensive TRS retirement planning mistakes.

Retiring before meeting the Rule of 80 results in significant benefit reductions. These reductions are permanent and can cost you thousands of dollars over your retirement lifetime. Yet some teachers retire early without fully understanding the financial impact.

The reduction formula is complex, but generally, you’ll lose about 5% of your benefit for each year you retire before meeting the Rule of 80. For a teacher with a $3,000 monthly benefit, retiring three years early could result in a permanent reduction to about $2,550 per month.

On the flip side, some teachers work longer than necessary, thinking more years always means better benefits. While additional service credit does increase your monthly benefit, the increase may not justify the delayed retirement, especially considering factors like health and quality of life.

TRS benefits are calculated using your highest five years of salary, so working additional years at a lower salary (perhaps as a substitute or part-time teacher) won’t necessarily improve your benefit calculation.

Texas teachers don’t pay into Social Security through their teaching positions, but many have Social Security benefits from other employment. Coordinating TRS retirement with Social Security claiming decisions requires careful planning that many teachers neglect.

Some teachers rush to claim Social Security at 62, not realizing how this decision interacts with their overall retirement income strategy. Others wait too long to claim, missing years of benefits they could have received.

Understanding how TRS calculates your monthly retirement benefit is crucial, yet many teachers make mistakes that reduce their final benefit amount.

Your TRS benefit is calculated using your five highest salary years, but many teachers don’t strategically plan to maximize these years. Working additional responsibilities, coaching positions, or summer school during your final years can significantly boost your retirement benefit.

Some teachers miss opportunities to include supplemental pay in their high-five calculation. Stipends for department head positions, coaching, or other extra duties can increase your creditable compensation if structured properly.

TRS uses different benefit multipliers based on when you were hired and your years of service. Teachers hired before September 1, 2007, have more generous multipliers than those hired later. Understanding your specific multiplier helps you plan more accurately.

Many newer teachers don’t realize they have a lower multiplier and may need to work additional years or save more independently to maintain their desired lifestyle in retirement.

Cost-of-living adjustments (COLAs) for TRS retirees are not automatic and depend on legislative action. Many teachers assume their benefits will automatically increase with inflation, leading to inadequate retirement planning.

Recent retirees have experienced minimal COLAs, making it crucial to plan for the purchasing power erosion of your TRS benefit over time.

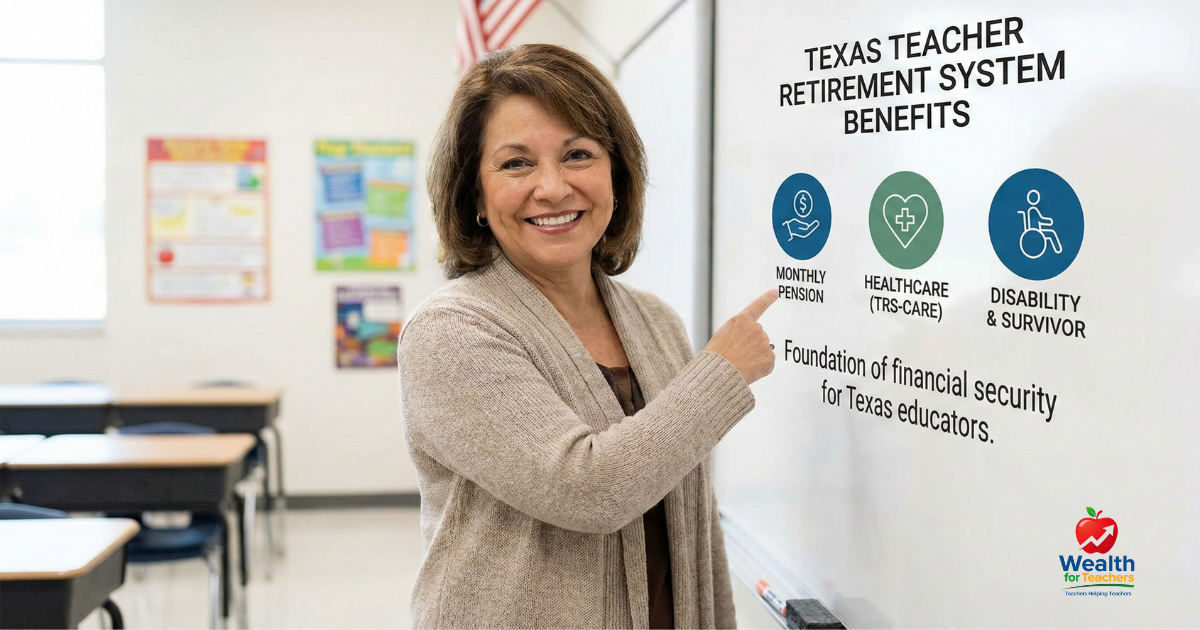

Healthcare costs in retirement can devastate your budget if not properly planned. Texas teachers often make mistakes regarding TRS-Care and Medicare coordination.

Not all TRS retirees qualify for TRS-Care health insurance. You must meet specific criteria, including the Rule of 80 or having 10 years of service credit with Medicare eligibility. Many teachers assume they’ll automatically have access to this coverage.

Teachers who retire early without meeting TRS-Care eligibility requirements face a significant coverage gap until they become Medicare eligible. This gap can be expensive and requires alternative insurance arrangements.

Teachers who become eligible for Medicare must understand how it coordinates with TRS-Care. Failing to enroll in Medicare Part A and B when first eligible can result in permanent penalties and coverage complications.

Many retired teachers don’t understand the Medicare enrollment timeline or the implications of their choices. These decisions can affect both your coverage options and costs for the rest of your retirement.

Healthcare costs typically increase faster than general inflation, but many teachers don’t factor this into their retirement planning. According to Fidelity, the average retired couple may need approximately $300,000 for healthcare expenses in retirement.

TRS-Care premiums and out-of-pocket costs have increased significantly over the years, and this trend is likely to continue. Budgeting for these increases is essential for long-term financial security.

Beyond TRS benefits, Texas teachers often make broader financial planning mistakes that affect their retirement security.

Many teachers rely too heavily on their TRS pension and don’t save enough in additional retirement accounts. While TRS provides a solid foundation, it may not fully replace your pre-retirement income, especially considering inflation and healthcare costs.

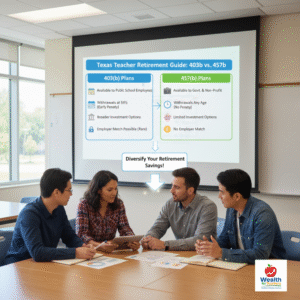

The 403(b) and 457(b) plans available to Texas teachers offer valuable tax advantages, but participation rates are often low. Many teachers who do participate don’t contribute enough to maximize their retirement security.

Understanding 403(b) vs 457(b) for Texas teachers can help you make better supplemental retirement saving decisions.

Teachers who do participate in supplemental retirement plans often make poor investment choices. High-fee annuities and overly conservative portfolios can significantly reduce long-term growth potential.

Many teachers are intimidated by investment decisions and default to options that may not serve their long-term interests. Understanding basic investment principles or seeking professional guidance can improve outcomes significantly.

Retired teachers often face unexpected expenses or income disruptions. Having an adequate emergency fund and understanding your options for accessing retirement funds early can prevent financial hardship.

Some teachers retire without considering how they’ll handle major expenses like home repairs, medical emergencies, or family financial crises. Planning for these possibilities is crucial for retirement security.

Many teachers fail to update their estate planning documents after retirement or don’t understand how TRS benefits are handled upon death. Proper beneficiary designations and estate planning can protect your surviving spouse and family.

TRS survivor benefits have specific rules and limitations that differ from Social Security survivor benefits. Understanding these differences helps ensure your family is protected.

Avoiding these TRS retirement planning mistakes requires proactive planning and ongoing education. Here’s how to protect your retirement security:

Begin retirement planning as soon as you start teaching. Understanding your benefits early allows you to make informed career decisions and maximize your retirement security. Even if retirement seems far away, early planning compounds over time.

Create a retirement timeline that considers the Rule of 80, your desired retirement age, and your financial goals. This timeline should be flexible but provide a framework for your planning decisions.

Log into your TRS account at least once per year to review your service credit, salary history, and benefit estimates. Look for errors or missing information and contact TRS promptly to resolve any issues.

Use the TRS benefit calculator to estimate your retirement income under different scenarios. This tool helps you understand how additional years of service or salary changes affect your benefits.

Investigate opportunities to purchase additional service credit, including military service and out-of-state teaching experience. Calculate the cost versus benefit of these purchases to make informed decisions.

Consider strategies to maximize your creditable compensation during your high-five years. This might include taking on additional responsibilities, coaching positions, or summer school assignments.

Understand your healthcare options in retirement and plan accordingly. If you won’t qualify for TRS-Care, research alternative coverage options and budget for higher healthcare costs.

Learn about Medicare enrollment requirements and timing. Consider how Medicare supplements or advantage plans might work with your overall healthcare strategy.

Don’t rely solely on TRS for your retirement income. Contribute to 403(b) or 457(b) plans if available, and consider additional savings vehicles like IRAs or taxable investment accounts.

Many teachers benefit from understanding Texas teachers 403(b) guide principles to make better supplemental retirement decisions.

Consider working with a financial advisor who understands teacher retirement benefits. They can help you create a comprehensive retirement plan that coordinates all your income sources and addresses your specific needs.

Professional guidance is particularly valuable for complex situations involving multiple retirement systems, substantial outside savings, or unique family circumstances.

Ready to take control of your teacher retirement planning? Our comprehensive planning process helps Texas teachers avoid costly mistakes and maximize their retirement security.

The impact depends on the specific mistake. Some errors, like retiring before the Rule of 80, result in permanent benefit reductions. Others, like missing service credit opportunities, mean lower monthly benefits. However, many mistakes can be corrected if caught early enough.

Yes, most service record errors can be corrected, but it’s easier when caught early. Contact TRS member services with documentation supporting your claim. Common fixes include adding missing employment periods, correcting salary information, or updating personal information.

This depends on your individual situation. Meeting the Rule of 80 allows full benefits without reduction, but working longer increases your monthly benefit. Consider factors like your health, job satisfaction, financial needs, and other retirement income sources when making this decision.

Most financial experts recommend additional retirement savings beyond TRS. While TRS provides a solid foundation, supplemental savings help ensure retirement security, especially considering healthcare costs and potential benefit changes. The tax advantages of 403(b) plans make them attractive for many teachers.

Texas teachers don’t earn Social Security credits through teaching, but you may have Social Security benefits from other employment. These benefits aren’t directly affected by your TRS pension, but coordinating the timing of both can optimize your total retirement income.

If health or family circumstances require early retirement, understand the reduction in benefits and plan accordingly. Consider part-time work or substitute teaching to extend your working years if possible. Explore disability retirement options if health issues prevent continued work.

Review your retirement planning annually and after major life changes like marriage, divorce, or significant salary changes. Legislative changes to TRS benefits also warrant plan reviews. Regular monitoring helps ensure you stay on track toward your retirement goals.

TRS provides educational materials, webinars, and counseling services. Many school districts offer retirement planning seminars. Professional financial advisors familiar with teacher benefits can provide personalized guidance. Online calculators and planning tools also help model different retirement scenarios.

Get Your Free Guide 10 Money Mistakes Teachers Make.