Is DIY Retirement Planning Risky for Texas Teachers?

DIY retirement planning can lead to costly mistakes. Here’s what Texas teachers should consider.

TRS Retirement Income Gap: Why Your Teacher Pension Won’t Be Enough As a Texas teacher, you’ve likely heard that your Teacher Retirement System (TRS) pension will provide a comfortable retirement. Unfortunately, the reality is far more complex. The TRS retirement income gap represents the significant shortfall between what your pension will actually provide and what […]

As a Texas teacher, you’ve likely heard that your Teacher Retirement System (TRS) pension will provide a comfortable retirement. Unfortunately, the reality is far more complex. The TRS retirement income gap represents the significant shortfall between what your pension will actually provide and what you’ll need to maintain your standard of living in retirement.

Most Texas teachers face a sobering truth: their TRS pension, while valuable, typically replaces only 40-60% of their pre-retirement income. This leaves a substantial gap that must be filled through other savings and investments to avoid a dramatic lifestyle reduction in retirement.

The Texas Teacher Retirement System uses a straightforward formula to calculate your pension benefits. Unlike some retirement systems with complex tiers or progressive multipliers, TRS applies a flat 2.3% multiplier for each year of creditable service.

Here’s how your TRS pension calculation works:

Annual Pension = (Years of Service × 0.023) × Final Average Salary

Your final average salary is typically the highest three or five (depending on your Tier) consecutive years of your career. This means if you teach for 25 years with a final average salary of $60,000, your calculation would be:

While $34,500 annually sounds substantial, it represents a significant reduction from your working income. This is where the retirement income gap becomes apparent.

To receive your full TRS pension, you must meet specific age and service requirements:

These requirements mean many teachers cannot access their full pension benefits immediately upon leaving the classroom, potentially widening the income gap during early retirement years.

Financial experts typically recommend replacing 70-90% of your pre-retirement income to maintain your standard of living. However, most TRS pensions fall well short of this target.

The 70% replacement ratio assumes you’ll have lower expenses in retirement – no mortgage payment, reduced transportation costs, and eliminated work-related expenses. Even with these reductions, most teachers need significantly more than their TRS pension alone provides.

Let’s examine a typical scenario:

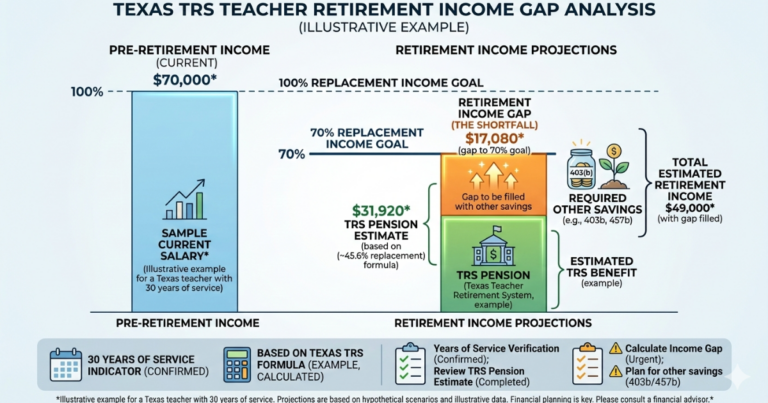

Example: Teacher with 30 Years of Service

This example shows a teacher with 30 years of service barely meeting the minimum 70% replacement ratio. However, many teachers retire with fewer years of service or desire to maintain a higher percentage of their pre-retirement lifestyle.

If you want to maintain 80-90% of your pre-retirement income, the gap becomes more pronounced:

80% Replacement Goal:

90% Replacement Goal:

Several structural factors contribute to the retirement income gap that Texas teachers face:

Teacher salaries often plateau in the later years of a career, limiting the growth of your final average salary. Unlike private sector workers who may see significant income increases throughout their careers, teachers typically follow structured pay scales with modest annual increases.

Many private sector employees have access to employer-matched 401(k) plans in addition to Social Security. Texas teachers don’t pay into Social Security, making TRS their primary government-sponsored retirement benefit. While TRS offers a 403(b) plan, there’s no employer matching contribution.

Your TRS pension includes cost-of-living adjustments, but these don’t always keep pace with actual inflation. Healthcare costs, in particular, tend to rise faster than general inflation, creating additional pressure on fixed retirement incomes.

Teachers often enjoy longer lifespans than the general population, which is wonderful but creates additional financial pressure. A longer retirement means your savings must stretch further, potentially widening the income gap over time.

The size of your retirement income gap depends on several personal factors:

Your years of creditable service directly impact your pension benefit percentage. Teachers who change districts, take breaks from teaching, or start their careers later may have fewer years of service, resulting in lower pension benefits and larger income gaps.

Your three highest consecutive years determine your final average salary. Teachers in higher-paying districts or those who earn additional degrees and certifications typically have higher final average salaries, reducing their income gaps.

Early retirees face potential pension reductions and longer periods without income, widening the gap. Health considerations may force some teachers into early retirement before they’ve accumulated sufficient service years.

Your desired retirement lifestyle significantly impacts the size of your income gap. Teachers who want to travel extensively, maintain expensive hobbies, or support family members may need to replace 90% or more of their pre-retirement income.

Cost of living varies significantly across Texas. Teachers retiring in expensive urban areas like Austin or Dallas may find their pension dollars don’t stretch as far as those retiring in more affordable rural communities.

Let’s examine several realistic scenarios to illustrate how the retirement income gap affects different types of Texas teachers:

Example only with stated assumptions:

This teacher faces a substantial annual gap of nearly $17,000, requiring significant additional savings to bridge the difference.

Example only with stated assumptions:

This veteran teacher actually exceeds the 80% replacement ratio, demonstrating how longer service can minimize or eliminate the income gap.

Example only with stated assumptions:

This teacher needs an additional $14,175 annually to meet their retirement income goals.

Before making retirement income decisions, it’s important to understand

how the TRS pension is calculated.

You can read more in TRS Retirement Eligibility Explained.

You should also understand how inflation impacts retirement income in

How Inflation Impacts Teacher Retirement Income.

For a complete overview, visit our Texas Teacher Retirement Planning Guide.

For most Texas teachers, TRS alone won’t provide sufficient retirement income. While TRS offers a solid foundation, it typically replaces only 40-60% of pre-retirement income for teachers with average service years. You’ll likely need additional savings and investments to maintain your desired lifestyle. For a full overview of why most teachers underestimate their TRS pension.

The amount depends on your retirement goals and service years. A teacher with 25 years of service might need to save enough to generate $10,000-15,000 annually in additional retirement income. This could require accumulated savings of $250,000-400,000, depending on withdrawal rates and investment returns.

Texas teachers don’t pay into Social Security, so you won’t receive Social Security benefits based on your teaching career. However, if you worked in other jobs where you paid Social Security taxes, you might be eligible for reduced Social Security benefits through the Windfall Elimination Provision (WEP).

You can still receive TRS benefits with fewer years of service, but your pension will be proportionally smaller. Each year of service adds 2.3% to your benefit percentage. Teachers with 20 years receive 46% of their final average salary, while those with 25 years receive 57.5%.

TRS’s 403(b) plan can help bridge the retirement income gap, but it doesn’t include employer matching. You’ll need to evaluate the plan’s investment options and fees against other available retirement savings vehicles. Many teachers benefit from maximizing their 403(b) contributions, especially if they’re behind on retirement savings.

If you retire before meeting the full eligibility requirements (such as age 60 with 20 years or age 65 with 5 years), your benefits may be reduced. The reduction depends on how early you retire and can significantly widen your income gap.

If you taught in other states, you might have benefits from multiple teacher retirement systems. However, these benefits typically don’t combine, and some states have different vesting requirements. You’ll need to track benefits from each system separately.

TRS provides cost-of-living adjustments (COLAs), but these may not fully keep pace with inflation, especially in areas like healthcare. Over a 20-30 year retirement, even small gaps between COLAs and actual inflation can erode your purchasing power and widen the effective income gap.

Recognizing the retirement income gap is the first step; addressing it requires a proactive approach to retirement planning beyond your TRS pension.

The power of compound interest makes early savings incredibly valuable. Even small monthly contributions to a 403(b), IRA, or other investment account can grow significantly over a 20-30 year career. Consider automating your contributions to make consistent saving easier.

Work toward accumulating as many service years as possible. Each additional year increases your benefit percentage by 2.3%. If you’re considering early retirement, carefully evaluate the long-term impact on your pension benefits and overall retirement security.

Don’t rely solely on TRS for retirement income. Consider multiple income streams:

Since your pension is based on your final average salary, strategies to increase your earnings in your final years can have a significant impact. Consider pursuing advanced degrees, certifications, or administrative roles that increase your salary.

Healthcare expenses often represent one of the largest retirement costs. TRS provides health insurance options for retirees, but you’ll still face premiums, deductibles, and out-of-pocket costs. Factor these expenses into your retirement income planning.

Your TRS pension remains the same regardless of where you live in retirement. Moving to a lower cost-of-living area can effectively increase your pension’s purchasing power and reduce the income gap.

A financial advisor who understands teacher retirement benefits can help you create a comprehensive retirement strategy. They can model different scenarios, recommend appropriate investment strategies, and help you stay on track toward your retirement goals.

Your retirement planning shouldn’t be set-and-forget. Regularly review your progress, adjust your savings rate as your income increases, and modify your strategy based on changing life circumstances or retirement goals.

The TRS retirement income gap is a reality for most Texas teachers, but it doesn’t have to derail your retirement dreams. By understanding the gap, starting early with supplemental savings, and developing a comprehensive retirement strategy, you can work toward a financially secure and comfortable retirement that goes beyond what TRS alone can provide.

Get Your Free TRS Calculation

DIY retirement planning can lead to costly mistakes. Here’s what Texas teachers should consider.

Market swings can impact your retirement income more than you think. Here’s how teachers are affected.