How to Build a Guaranteed Income Floor as a Teacher

Stable income is the foundation of retirement security. Learn how to build it.

Learn about teacher longevity risk and how it affects Texas teachers planning for retirement.

Teacher longevity risk represents one of the most overlooked threats to a secure retirement. While Texas teachers often focus on reaching the Rule of 80 or maximizing their pension benefits, many fail to consider what happens if they live longer than their savings can support.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

The reality is stark: if you outlive your retirement income, you face decades of financial hardship with few options to recover. Unlike working years when you can increase income or change careers, retirement leaves little room for error.

For Texas teachers relying on TRS benefits, understanding longevity risk becomes even more critical. Your pension provides a foundation, but it may not cover all expenses as costs rise and health needs change over time.

This comprehensive Texas Teacher Retirement Planning Guide approach requires examining not just how much you’ll receive from TRS, but how long those benefits need to last and what gaps might emerge.

Most retirement plans fail because they are never tested under real-world conditions. Teachers often make assumptions about expenses, health costs, and lifespan that prove optimistic when faced with actual retirement challenges.

Teacher longevity risk occurs when your retirement income cannot support your expenses for the duration of your retirement. This happens when you live longer than your financial plan anticipated or when inflation erodes your purchasing power over time.

Use the TRS calculator to estimate your pension and identify potential income gaps.

For Texas teachers, longevity risk manifests in several ways:

The challenge intensifies because teaching careers often begin later or include breaks for family care, reducing both TRS service credit and personal savings accumulation time.

A Texas teacher retiring at 60 with 30 years of service might live another 25 to 30 years. That TRS pension must stretch across three decades while maintaining purchasing power against inflation.

Texas teachers encounter specific factors that amplify longevity risk compared to private sector employees.

Most Texas teachers don’t pay into Social Security during their teaching careers. This means no Social Security safety net if other income sources prove insufficient. The WEP and GPO rules can further reduce any Social Security benefits earned from non-teaching employment.

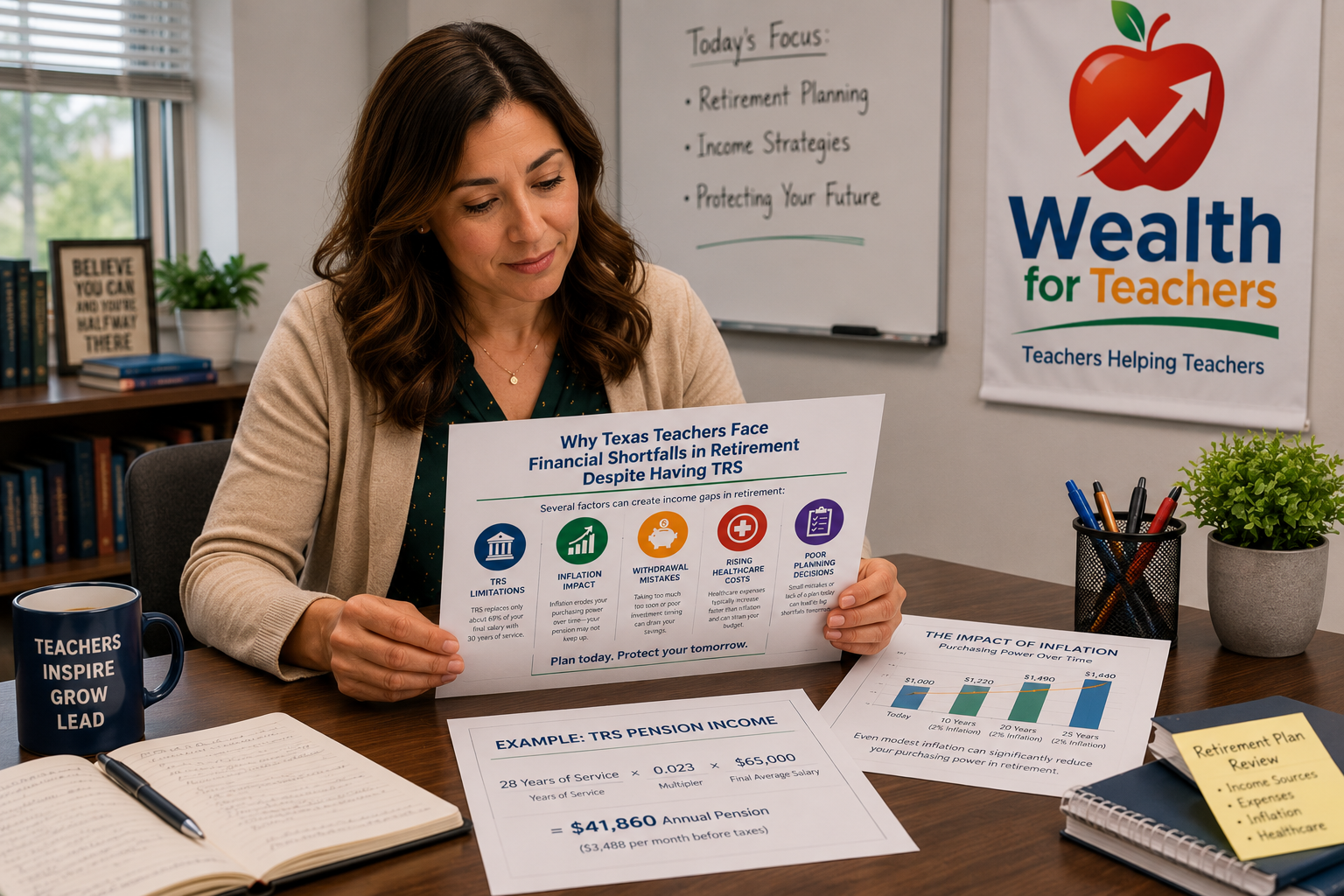

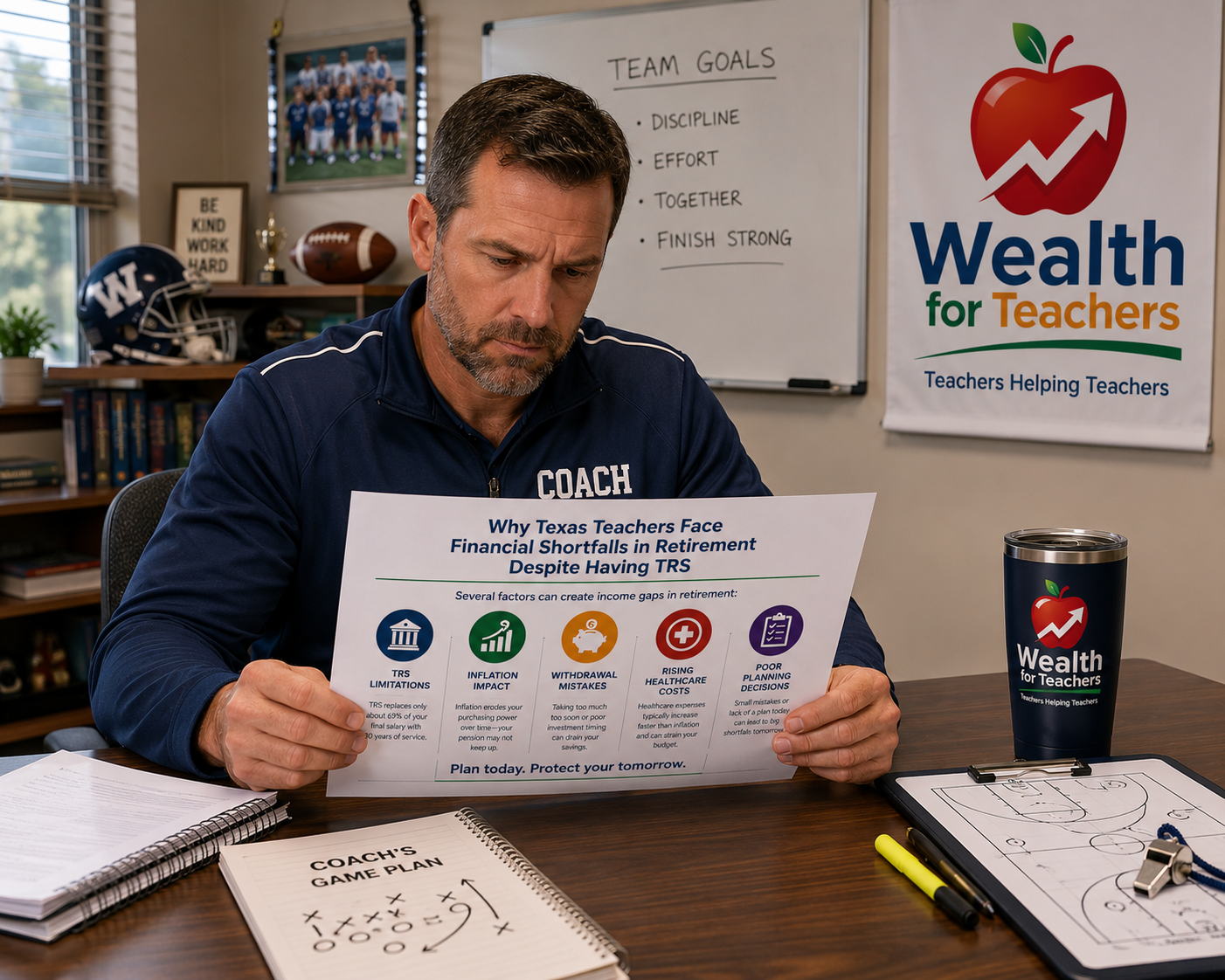

Texas TRS uses a flat 2.3% multiplier per year of service. A teacher with 30 years earns 69% of their final average salary as an annual pension. While substantial, this fixed amount doesn’t increase with inflation, creating purchasing power erosion over long retirement periods.

Many Texas school districts offer 403(b) plans with limited investment options and high fees. Teachers often accumulate less in personal retirement savings compared to employees with access to quality 401(k) plans or other investment vehicles.

Texas TRS DROP allows eligible teachers to continue working while accruing pension benefits in a separate account. However, DROP creates its own longevity risks if teachers don’t properly manage the lump sum distribution after leaving employment.

Texas teachers frequently underestimate longevity risk due to planning errors that seem minor but compound over decades.

Many teachers plan for retirement lengths based on average life expectancy rather than considering they might live well beyond average. A healthy 60-year-old teacher has a significant chance of living past 85, requiring 25+ years of retirement funding.

Teachers often calculate retirement needs using current expense levels without accounting for inflation. Even modest 3% annual inflation reduces purchasing power by nearly 50% over 20 years.

A teacher spending $60,000 annually at retirement would need $108,000 in purchasing power after 20 years to maintain the same lifestyle.

While TRS pensions provide excellent base income, they rarely cover 100% of pre-retirement expenses. Teachers who assume their pension alone will fund retirement face shortfalls that compound as longevity risk increases.

Medicare doesn’t cover all healthcare expenses, and costs tend to accelerate with age. Long-term care expenses can quickly deplete savings that were meant to last decades.

When teachers exhaust their retirement savings while still living, the consequences extend beyond financial stress.

Teachers who outlive their savings must drastically cut expenses, often moving to smaller homes, eliminating discretionary spending, or relying on family support.

Without adequate savings, retired teachers may delay medical care, skip medications, or choose less comprehensive insurance coverage, potentially worsening health outcomes.

Teachers who run out of money often become financially dependent on adult children or other family members, creating stress and guilt that impacts relationships.

Unlike working years when financial setbacks can be overcome through increased income or career changes, retirement offers few opportunities to rebuild wealth or increase income substantially.

While Texas TRS provides valuable retirement benefits, certain limitations create vulnerability to longevity risk.

Texas TRS pensions don’t automatically adjust for inflation. The state legislature can approve cost-of-living adjustments, but these are discretionary and infrequent. This means your pension’s purchasing power declines every year.

Teachers who elect reduced benefits to provide survivor protection receive lower monthly payments during their lifetime, potentially increasing longevity risk if they live longer than expected while their spouse predeceases them.

Teachers who retire before meeting the Rule of 80 face actuarial reductions that permanently lower their pension payments. These reduced benefits provide less protection against longevity risk.

Unlike personal retirement accounts, TRS pensions can’t be adjusted based on changing circumstances. You can’t access additional funds during emergencies or modify payment amounts to address longevity concerns.

Healthcare expenses represent one of the largest and least predictable costs in retirement, significantly increasing longevity risk for Texas teachers.

Medicare doesn’t cover dental, vision, or hearing aids. Long-term care coverage is extremely limited. These gaps require additional insurance or out-of-pocket spending that increases over time.

Many teachers require multiple medications as they age. Even with Medicare Part D coverage, co-pays and deductibles can consume significant portions of fixed pension income.

The average cost of nursing home care in Texas exceeds $4,000 monthly. Even home health services can cost $3,000 to $5,000 per month. These expenses can quickly exhaust retirement savings intended to last decades.

TRS provides health insurance for retirees, but premium costs have increased over time. Future increases could strain retirement budgets and increase longevity risk.

Protecting against teacher longevity risk requires proactive planning that goes beyond simply maximizing your TRS pension.

Use the TRS calculator to estimate your pension and identify potential income gaps.