How to Build a Guaranteed Income Floor as a Teacher

Stable income is the foundation of retirement security. Learn how to build it.

TRS Survivor Benefits: Essential Protection for Texas Teachers’ Families When you dedicate your career to educating Texas students, protecting your family’s financial future becomes just as important as shaping young minds. The Teacher Retirement System of Texas (TRS) recognizes this responsibility and provides survivor benefits designed to support your loved ones if something happens to […]

When you dedicate your career to educating Texas students, protecting your family’s financial future becomes just as important as shaping young minds. The Teacher Retirement System of Texas (TRS) recognizes this responsibility and provides survivor benefits designed to support your loved ones if something happens to you.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

These benefits serve as a crucial safety net, ensuring your spouse and dependents maintain financial stability even after you’re gone. Understanding how TRS survivor benefits work helps you make informed decisions about your retirement planning and gives you peace of mind knowing your family is protected.

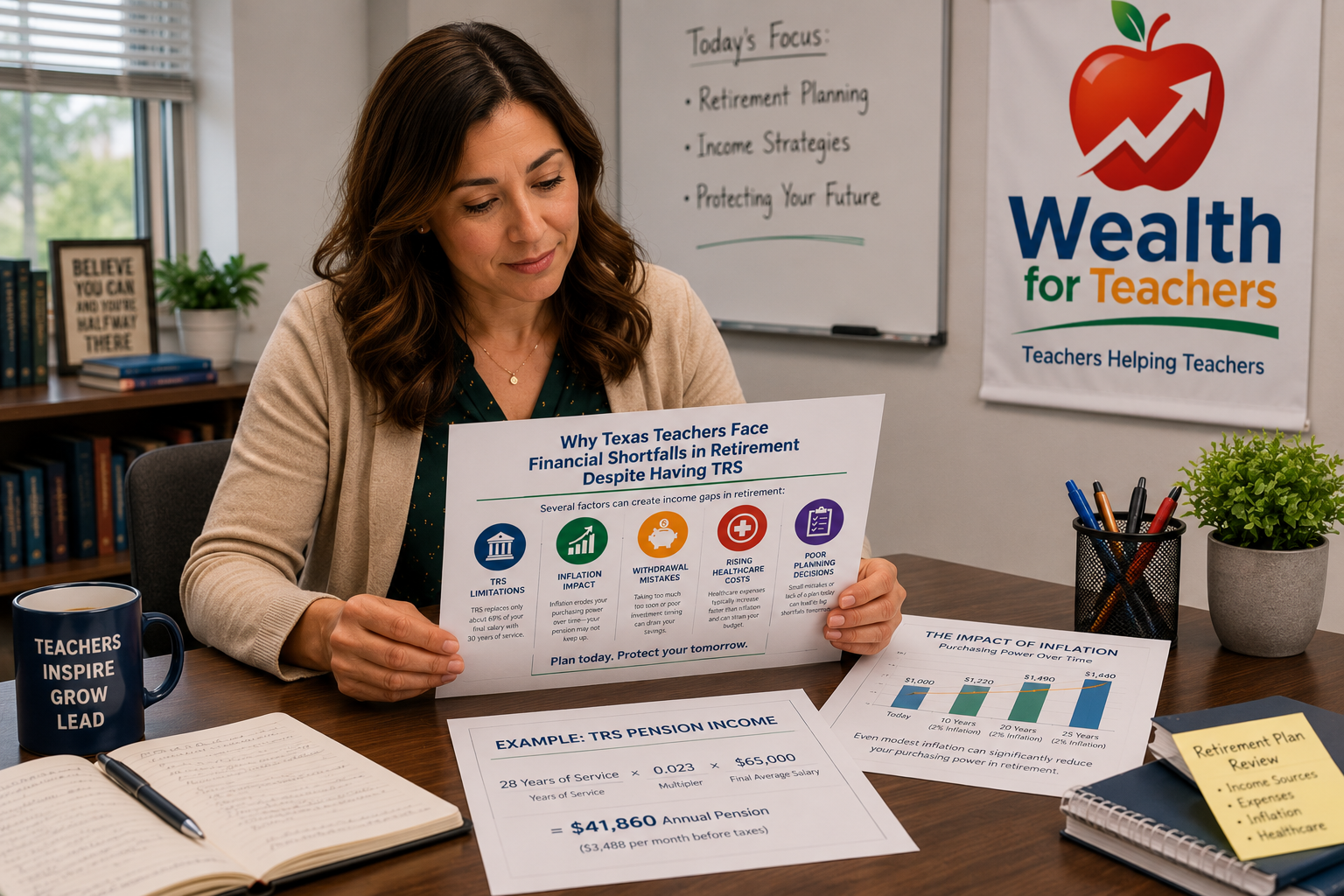

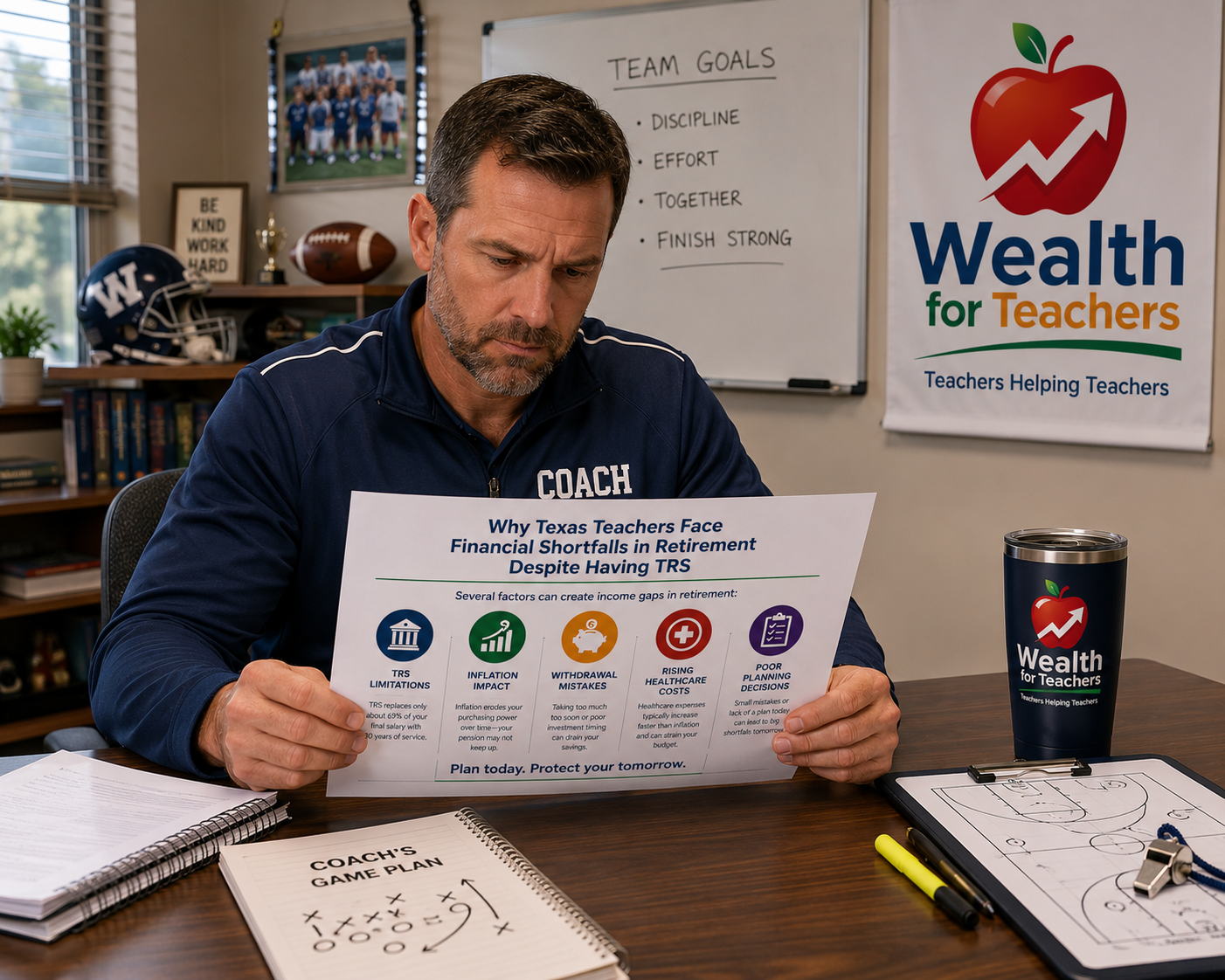

TRS survivor benefits provide monthly payments to eligible family members when an active or retired TRS member passes away. These benefits replace a portion of the income your family would have lost, helping them maintain their standard of living during a difficult time.

Use the TRS calculator to estimate your pension and identify potential income gaps.

The system recognizes that teachers often serve as primary or significant income earners in their households. Without proper protection, families could face financial hardship on top of their emotional grief.

Survivor benefits through TRS operate differently depending on your status at the time of death:

Each situation has specific rules and benefit amounts, making it essential to understand where you currently stand in the TRS system.

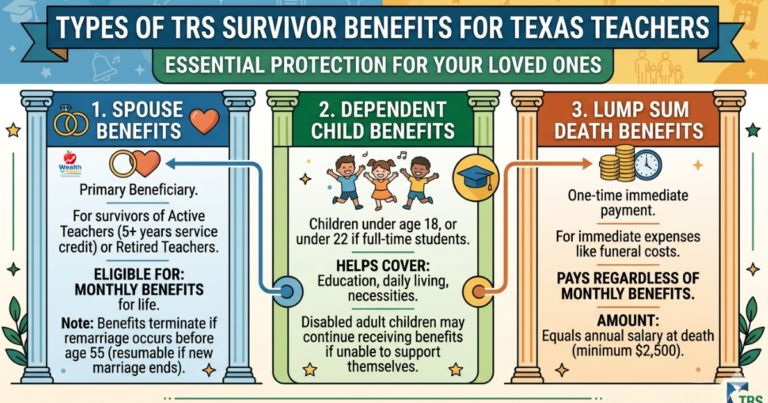

Your surviving spouse represents the primary beneficiary for TRS survivor benefits. If you pass away as an active teacher with at least five years of service credit, your spouse becomes eligible for monthly benefits.

The spouse benefit continues for life, providing ongoing financial support. However, remarriage before age 55 will terminate these benefits, though they can resume if the new marriage ends.

Children under age 18 (or under 22 if full-time students) may receive survivor benefits. These payments help cover education expenses, daily living costs, and other necessities during their formative years.

Disabled adult children may continue receiving benefits beyond the typical age limits if their disability prevents them from supporting themselves.

TRS also provides a one-time lump sum payment to help families cover immediate expenses like funeral costs. This benefit pays regardless of whether monthly survivor benefits are available.

The lump sum amount equals your annual salary at the time of death, with a minimum of $2,500. This immediate payment helps families handle urgent financial needs while waiting for monthly benefits to begin.

If you’re currently teaching and contributing to TRS, your survivors become eligible for benefits when you have:

The five-year service requirement ensures you’ve made sufficient contributions to the system before survivor benefits activate.

Retired teachers receiving TRS benefits automatically provide survivor protection to their families. The benefit amount depends on the retirement option you selected when you first retired.

Teachers who chose joint-and-survivor retirement options provide higher survivor benefits than those who selected single-life options for maximum personal benefits.

TRS requires marriages to have lasted at least one year before death for survivor benefits to apply. This prevents last-minute marriages solely for benefit purposes while protecting legitimate spouses.

Common-law marriages recognized under Texas law also qualify, provided you can document the relationship’s validity and duration.

When an active teacher with adequate service credit passes away, TRS calculates survivor benefits based on what the teacher would have received if they had retired with a disability.

Using the standard TRS formula, the calculation works as follows:

Example calculation for active teacher survivor benefits:

This example shows how families receive approximately half of what the teacher’s retirement benefit would have been. You can read more from TRS Retirement Eligibility.

Retired teachers’ survivor benefits depend entirely on the retirement option selected at retirement:

Teachers who selected joint-and-survivor options typically provide 50% to 100% of their monthly benefit to surviving spouses, depending on the specific option chosen.

TRS survivor benefits may receive periodic cost-of-living adjustments, similar to active retirement benefits. These increases help maintain purchasing power over time, though they’re not guaranteed and depend on legislative approval and system funding.

Applying for TRS survivor benefits requires comprehensive documentation to verify eligibility and relationship status:

Gathering these documents during grief can be challenging, so many families benefit from assistance from TRS representatives or trusted advisors.

TRS encourages families to apply for survivor benefits as soon as possible after a member’s death. While there’s no strict deadline, delays can complicate the process and potentially delay benefit payments.

Most applications receive processing within 30-60 days, depending on the complexity of the situation and completeness of submitted documentation.

TRS employs dedicated staff members who specialize in helping families navigate the survivor benefit process. These representatives understand the emotional difficulty of the situation and work to make the process as smooth as possible.

Don’t hesitate to contact TRS directly for personalized assistance with your specific situation.

Survivor benefits typically begin the month following the member’s death, provided all paperwork is submitted promptly. TRS cannot make retroactive payments for months before the application is received.

The lump sum death benefit usually processes more quickly than monthly survivor benefits, providing immediate financial relief to families.

Spouse benefits generally continue for the survivor’s lifetime, with specific exceptions:

Child benefits end when the child reaches age 18, unless they’re full-time students (benefits continue to age 22) or disabled adults who cannot support themselves.

Divorced spouses generally do not qualify for TRS survivor benefits unless specific court orders established such rights during divorce proceedings. This makes understanding your divorce decree’s language crucial for financial planning.

Current spouses at the time of death receive priority for survivor benefits over former spouses, even with court orders in place.

When multiple children qualify for survivor benefits, TRS typically divides the available benefit amount among all eligible dependents. This ensures fair distribution but may result in smaller individual payments.

As children age out of eligibility, their portions may be redistributed to remaining eligible dependents or increase the surviving spouse’s benefit amount.

TRS survivor benefits coordinate with Social Security survivor benefits, though both systems operate independently. Families often receive benefits from both sources, providing more comprehensive protection.

Understanding how these benefits work together helps families maximize their total survivor income and plan appropriately for their needs.

Texas TRS recognizes marriages and common-law marriages under Texas law. Domestic partnerships without legal marriage status typically do not qualify for survivor benefits. Consider legal marriage or other financial planning strategies to protect your partner.

If you have less than five years of service credit, your beneficiaries receive your account contributions plus interest. With five or more years, they can choose between the account refund or monthly survivor benefits, typically choosing whichever provides greater long-term value.

Yes, TRS survivor benefits are generally taxable income to the recipient. However, the lump sum death benefit may receive different tax treatment. Consult with a tax professional about your specific situation for proper planning and withholding.

You cannot change your retirement option after retirement begins, which locks in survivor benefit arrangements. However, you can update beneficiaries for your TRS account and lump sum death benefit at any time by filing the appropriate forms with TRS.

Survivor benefits may receive the same cost-of-living adjustments as active retiree benefits when the Texas Legislature approves such increases. These adjustments help maintain purchasing power over time but are not automatic or guaranteed.

Survivor benefits only flow from the TRS member to their survivors, not between spouses. If your non-TRS spouse dies first, you won’t receive survivor benefits from TRS. Consider life insurance and other protection for this scenario.

Each state retirement system operates independently. Your survivors may be eligible for benefits from each system where you earned sufficient service credit. Contact each system separately to understand their specific survivor benefit provisions.

Eligible dependent children can receive survivor benefits regardless of their living arrangements or custody status. The benefits belong to the children, though the custodial parent typically manages the payments on their behalf.

If you’re unsure whether retiring early is worth it, read our guide on

Is Early TRS Retirement Ever a Smart Move?

You may also want to understand the differences between TRS Tier 1 vs Tier 2 vs Tier 3.

For a full overview of how Texas teacher retirement works, see the Texas Teacher Retirement Planning Guide.

While TRS survivor benefits provide valuable protection, they may not fully replace your income or meet your family’s complete financial needs. Term life insurance offers affordable additional protection during your working years.

Consider purchasing coverage equal to 8-10 times your annual salary to supplement TRS benefits and ensure comprehensive family protection.

Even with survivor benefits, families face immediate expenses and potential gaps in coverage. An emergency fund containing 6-12 months of living expenses provides crucial breathing room during the transition period.

Automate savings contributions to build this fund gradually without impacting your current lifestyle significantly.

Proper estate planning documents ensure your wishes are carried out and help your family navigate complex situations. Essential documents include:

Building additional retirement savings through 403(b) plans, IRAs, or other vehicles creates more options for survivor protection. These accounts often provide more flexible beneficiary options and can supplement TRS survivor benefits.

Life changes require updates to your survivor benefit planning. Review your situation annually and after major life events like:

Regular reviews ensure your protection keeps pace with your evolving circumstances and provides appropriate security for your loved ones.

TRS survivor benefits form an important foundation for protecting Texas teachers’ families, but they work best as part of a comprehensive financial protection strategy. Understanding these benefits helps you make informed decisions and take appropriate additional steps to ensure your family’s complete financial security.

Use the TRS calculator to estimate your pension and identify potential income gaps.