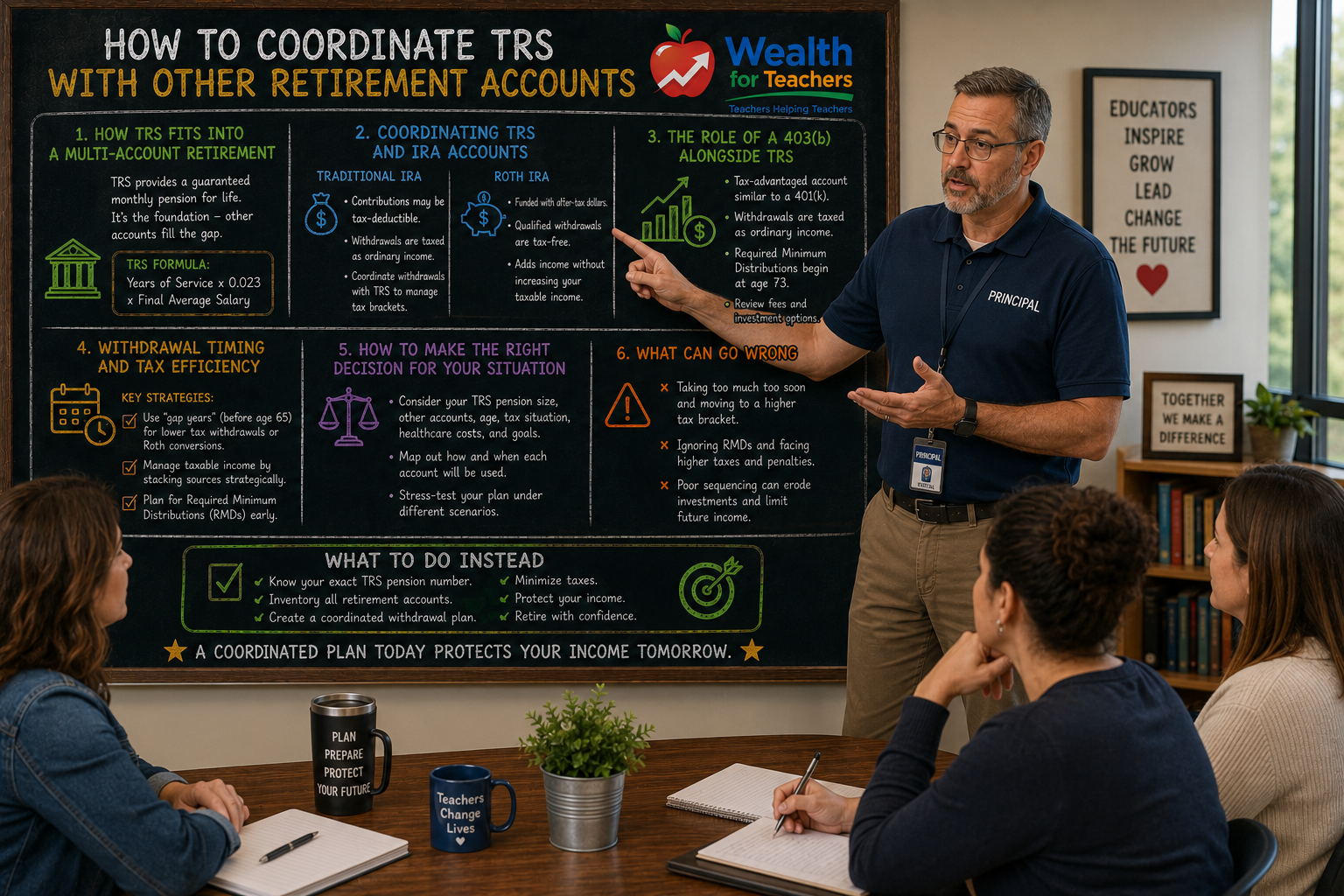

How to Coordinate TRS With IRAs, 403(b)s, and Other Accounts

TRS is only one piece of the puzzle. Learn how to align it with your other accounts.

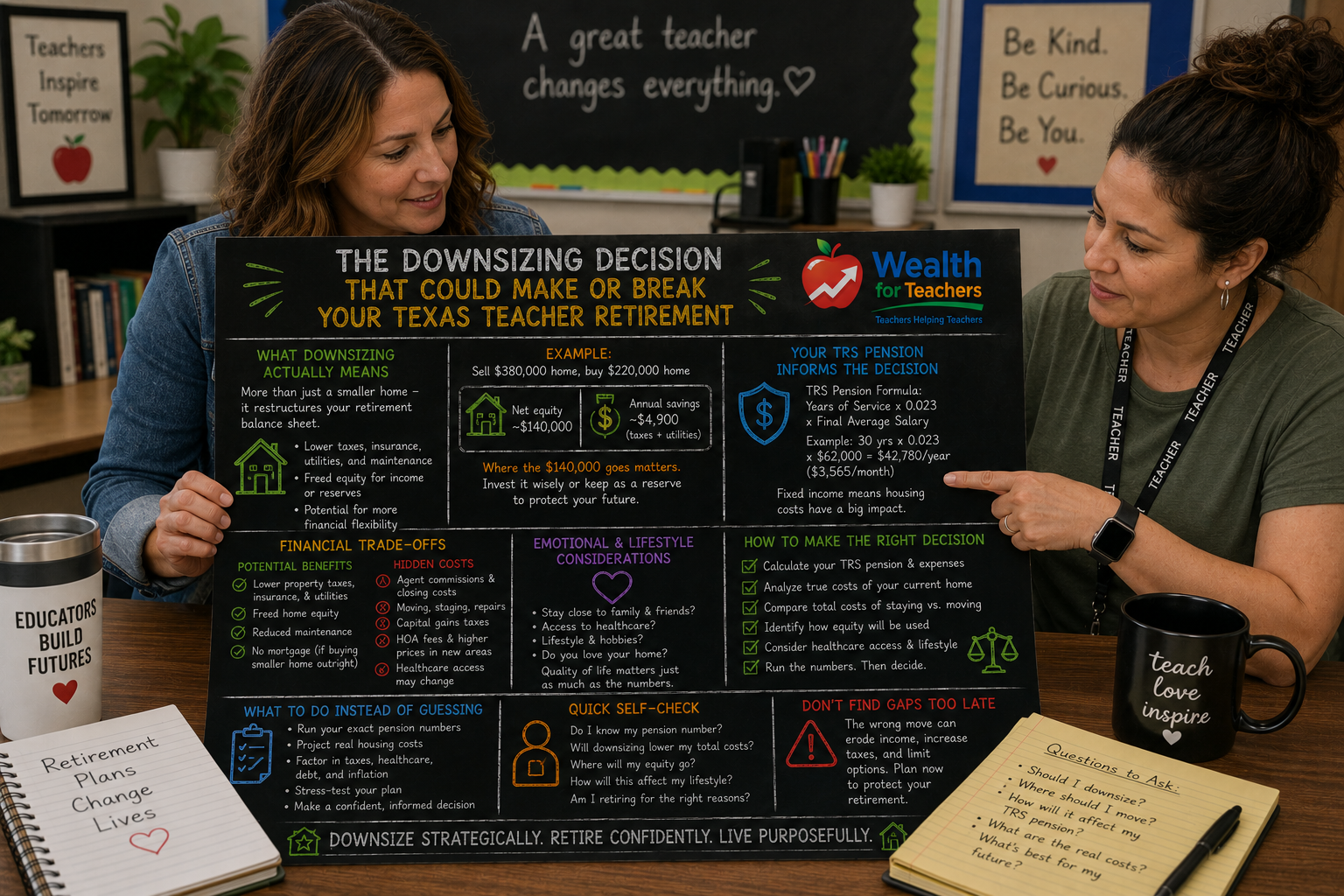

Downsizing can improve cash flow—but it’s not always the right move.

The decision to downsize in retirement feels obvious—lower expenses, less maintenance, more cash flow. But for Texas teachers who’ve spent decades building equity in their homes, downsizing can backfire spectacularly if you don’t understand how it affects your TRS pension, tax situation, and overall retirement income strategy.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

Unlike private sector retirees who might rely heavily on 401(k) withdrawals, teachers face unique considerations. Your TRS pension provides steady income, but it’s fixed. Your home equity represents decades of forced savings. The intersection of these two factors makes downsizing retirement teachers a complex decision that deserves careful analysis.

This isn’t just about square footage or mortgage payments. It’s about optimizing your entire retirement income plan—and understanding what can go wrong if you make the wrong choice at the wrong time.

For comprehensive retirement planning strategies that address all aspects of your financial future, review our Texas Teacher Retirement Planning Guide.

Most retirement plans fail because they’re never tested under real-world conditions. Teachers often assume downsizing will automatically improve their financial situation without considering tax implications, moving costs, market timing, or how the decision fits into their broader retirement income strategy.

Downsizing retirement teachers face a unique set of financial considerations that don’t apply to other retirees. Your TRS pension provides predictable income, but it’s not inflation-adjusted in the traditional sense. Texas TRS provides a 13th check when the fund performs well, but you can’t count on it for budgeting purposes.

Use the TRS calculator to estimate your pension and identify potential income gaps.

Consider a teacher with 30 years of service and a final average salary of $65,000. Their annual TRS pension equals $44,850 (30 × 0.023 × $65,000). This teacher might own a home worth $400,000 with a $150,000 mortgage balance, leaving $250,000 in equity.

If they downsize to a $250,000 home and pay cash, they eliminate their $1,200 monthly mortgage payment. That’s $14,400 annually in improved cash flow—a 32% increase over their TRS pension alone.

But this calculation ignores several critical factors:

Downsizing works best for teachers in specific situations. The decision becomes clearer when your housing costs consume more than 30% of your total retirement income, including TRS pension and other sources.

The strongest case for downsizing occurs when:

Teachers who built multiple income streams beyond TRS often have more flexibility in their downsizing decisions because they’re less dependent on home equity for financial security.

Texas teachers have an advantage many don’t realize: no state income tax. If you downsize within Texas, you maintain this benefit. But if you move to a state with income taxes, your TRS pension becomes taxable at the state level—potentially erasing much of your downsizing savings.

The biggest downsizing mistakes happen when teachers underestimate transaction costs and ongoing expenses. Real estate transactions aren’t cheap, and the “hidden” costs add up quickly.

Selling your current home and buying a new one typically costs 8-10% of your home’s value:

On a $400,000 home sale, these costs can reach $35,000-$40,000. That’s nearly three years of the mortgage payment savings you hoped to achieve.

Downsizing doesn’t always reduce all expenses proportionally:

Understanding healthcare costs in retirement becomes especially important when relocating, as provider networks and Medicare supplement options vary by location.

Teachers often underestimate the emotional impact of leaving their family home. You’ve likely hosted decades of holidays, watched children grow up in those rooms, and built deep community connections.

The emotional costs aren’t just sentimental—they’re financial. Many teachers who downsize too quickly discover they’ve traded financial flexibility for buyer’s remorse. Moving again becomes expensive, especially if you realize the smaller home doesn’t meet your needs.

Teachers thrive on community connections. Downsizing often means leaving established neighborhoods where you know neighbors, have preferred service providers, and understand local resources. Rebuilding these connections takes time and energy that many retirees underestimate.

Your TRS pension creates a financial foundation that changes how you should think about downsizing. Unlike retirees who need to generate all their income from savings, teachers have guaranteed monthly income that continues for life.

This security changes the risk-benefit calculation. You might not need to access home equity immediately, which means you can afford to wait for better market conditions or make more selective downsizing decisions.

Most teachers won’t owe capital gains taxes on their primary residence sale due to the $250,000 ($500,000 for married couples) exclusion. But if your home has appreciated significantly, or if you haven’t lived in it as your primary residence for two of the last five years, taxes could apply.

The interaction between home sale proceeds and your overall tax strategy becomes important. Large one-time gains could affect Medicare premiums or push you into higher tax brackets, especially if you’re managing required minimum distributions from retirement accounts.

No, your TRS pension amount is fixed based on your years of service and final average salary. Moving or downsizing doesn’t change your monthly benefit. However, moving out of state could subject your TRS pension to state income taxes.

This depends on your complete financial picture. Paying cash eliminates monthly payments but reduces liquidity. Keeping a mortgage preserves cash but creates ongoing payment obligations. Consider your other income sources and emergency fund needs.

The best timing depends on your specific situation, not market conditions. However, downsizing before major home repairs become necessary, or when you first start feeling financially stressed by housing costs, typically works better than waiting until you’re forced to move quickly.

Your housing costs (including mortgage, taxes, insurance, and maintenance) should represent no more than 25-30% of your total retirement income. If downsizing doesn’t achieve this ratio, you may need to consider more dramatic changes.

Moving again is expensive and disruptive. Before downsizing, consider whether your current home could work with modifications rather than relocation. Sometimes aging in place with home improvements costs less than downsizing and provides better long-term satisfaction.

Use the TRS calculator to estimate your pension and identify potential income gaps.