How to Build a Guaranteed Income Floor as a Teacher

Stable income is the foundation of retirement security. Learn how to build it.

Fiduciary for Teachers: Understanding Your Rights and Protections in Retirement Planning When planning for retirement as an educator, understanding the role of a fiduciary becomes crucial to protecting your financial future. A fiduciary for teachers serves as a legally bound advocate who must put your best interests first when providing financial advice or managing your […]

When planning for retirement as an educator, understanding the role of a fiduciary becomes crucial to protecting your financial future. A fiduciary for teachers serves as a legally bound advocate who must put your best interests first when providing financial advice or managing your retirement assets.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

As a teacher, you’ve dedicated your career to serving others. Now, when it comes to your retirement planning, you deserve the same level of dedication from financial professionals. The fiduciary standard ensures that anyone advising you on retirement matters must act with the highest level of care, loyalty, and transparency.

This comprehensive guide will help you understand what fiduciary responsibility means, how it protects you as an educator, and why it’s essential for your retirement planning success.

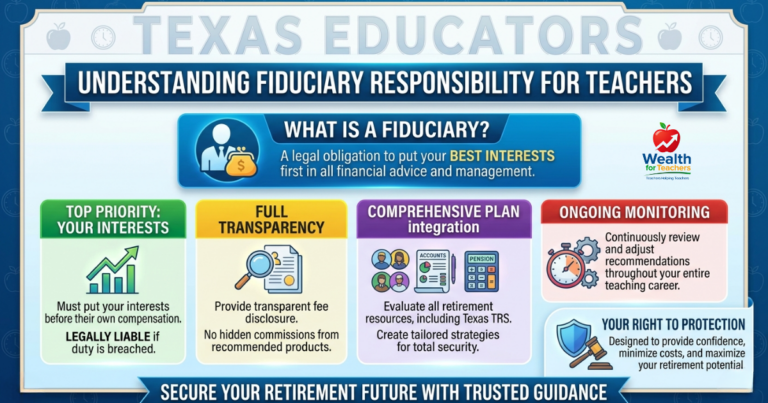

A fiduciary is a person or organization legally required to act in your best interest when managing your money or providing financial advice. This legal obligation creates the highest standard of care in financial relationships.

Use the TRS calculator to estimate your pension and identify potential income gaps.

For teachers, working with a fiduciary means having a financial professional who:

The fiduciary standard originated from trust law, where trustees were required to manage assets for beneficiaries with complete loyalty. Today, this standard applies to various financial professionals, including registered investment advisors, pension plan managers, and fee-only financial planners.

Understanding this distinction becomes especially important for teachers because educator retirement planning involves unique considerations that require specialized knowledge and undivided loyalty.

Many teachers don’t realize that not all financial professionals are held to the same standard of care. The difference between fiduciary and suitability standards can significantly impact your retirement planning outcomes.

Under the fiduciary standard, financial advisors must:

Under the suitability standard, financial professionals only need to:

The key difference is that suitability allows professionals to recommend higher-commission products as long as they’re not unsuitable. A fiduciary must recommend the best available option for your specific needs.

For teachers with limited income during their careers and complex retirement benefit systems, this distinction can mean thousands of dollars in additional costs or suboptimal investment choices over a career.

Teachers face unique financial challenges that make fiduciary protection especially valuable. Understanding these challenges helps explain why the highest standard of care is essential for educator retirement planning.

Most teachers earn modest salaries compared to other professionals with similar education levels. This income limitation means every dollar saved for retirement carries extra importance. You cannot afford to lose money to unnecessary fees or poor investment advice.

A fiduciary must consider your income constraints when making recommendations, ensuring that investment costs don’t erode your limited retirement savings capacity.

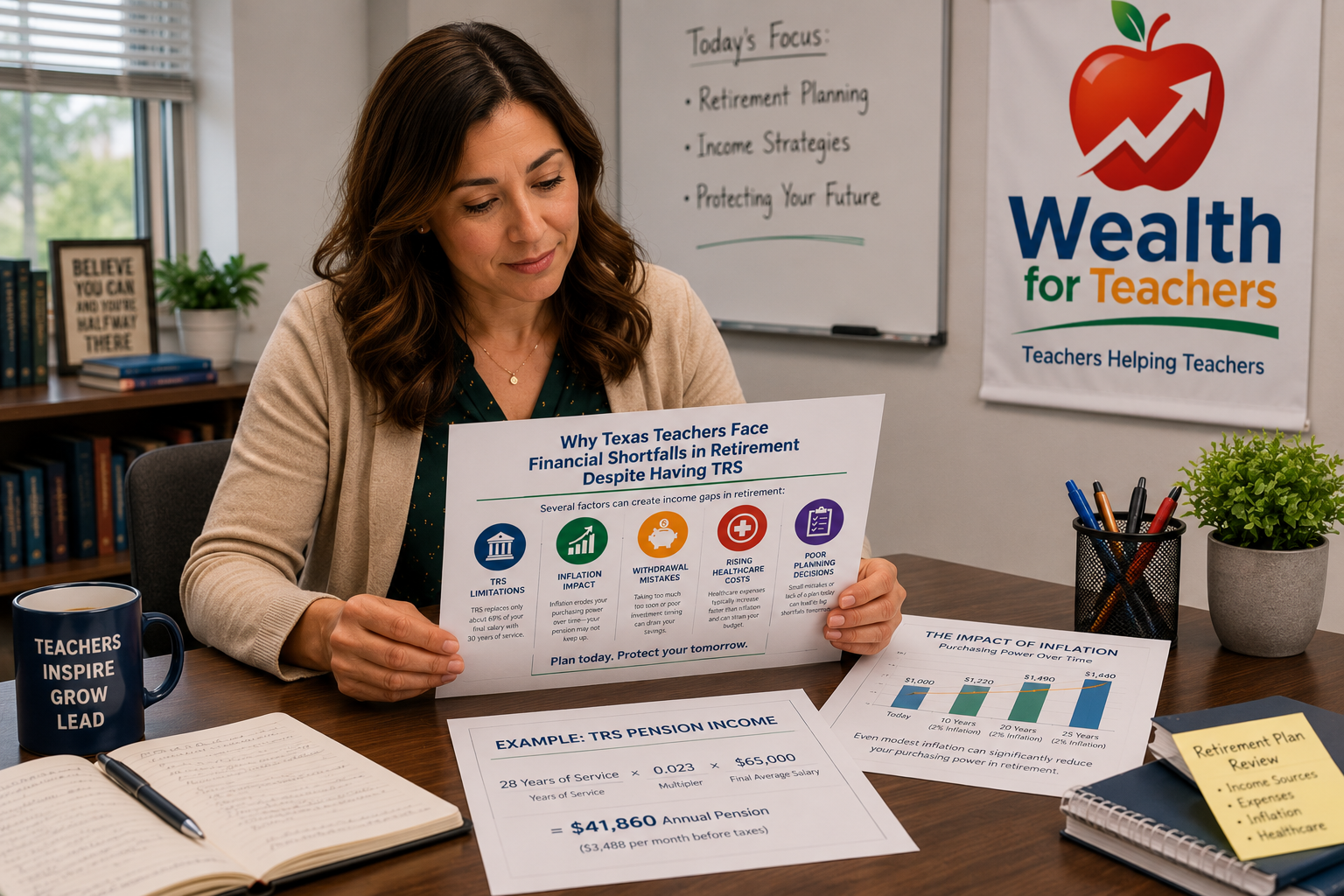

Teacher retirement systems involve intricate rules for pension calculations, vesting schedules, and benefit options. Texas TRS, for example, uses a flat 2.3% multiplier per year of service to calculate pension benefits.

For a teacher with 25 years of service and a final average salary of $60,000:

Understanding how supplemental savings interact with pension benefits requires specialized knowledge that a fiduciary must possess to provide proper guidance. Learn more about your TRS retirement eligibility explained.

Teaching careers often span 25-30 years, requiring long-term financial strategies that adapt to changing circumstances. A fiduciary’s ongoing duty of care ensures your retirement plan evolves appropriately throughout your career.

Many teachers enter the profession focused on education rather than financial planning. School districts often provide limited retirement planning resources, leaving teachers vulnerable to poor advice or unsuitable products.

A fiduciary fills this knowledge gap by providing education-specific financial guidance based on your best interests rather than product sales.

Several types of financial professionals can serve as fiduciaries for teachers. Understanding these options helps you choose the right type of fiduciary relationship for your needs.

RIAs are regulated by the SEC or state securities regulators and must act as fiduciaries at all times. They typically charge fees based on assets under management or hourly rates rather than commissions.

Benefits for teachers:

These planners only accept fees from clients, never commissions from product sales. This structure eliminates conflicts of interest and ensures fiduciary-level advice.

Advantages include:

CFPs must act as fiduciaries when providing financial planning services, though they may operate under different standards when selling products. Look for CFPs who operate as fee-only advisors for consistent fiduciary protection.

Your school district’s 403(b) plan administrator serves as a fiduciary for plan management. However, individual vendors within the plan may not be held to fiduciary standards when providing advice.

This creates a potential gap where teachers receive plan access through fiduciary oversight but individual guidance through suitability standards.

Not all financial professionals who claim to act in your best interest are actual fiduciaries. Learning to identify true fiduciary relationships protects you from misleading marketing claims.

When meeting with financial professionals, ask these specific questions:

Registered Investment Advisors must provide Form ADV, which discloses:

Review this document carefully before engaging any advisor’s services.

Check advisor credentials through:

Be cautious of professionals who:

A fiduciary working with teachers must understand the unique aspects of educator compensation and retirement benefits. This specialized knowledge ensures recommendations align with your specific career circumstances.

Your fiduciary should understand how supplemental retirement savings integrate with your pension benefits. This includes:

Teachers have access to 403(b) plans, which offer higher contribution limits but may have limited investment options. A fiduciary must evaluate:

Also, read on should teachers use annuities in retirement.

Many teachers face reduced summer income, requiring specialized budgeting and cash flow strategies. Your fiduciary should help you:

Teachers may change districts or states during their careers, affecting pension benefits and retirement accounts. A fiduciary must understand:

Yes, even with TRS pension benefits, you likely need additional retirement savings to maintain your lifestyle. A fiduciary helps optimize supplemental savings strategies, understand how different account types interact with your pension, and plan for healthcare costs in retirement. TRS provides a foundation, but most teachers need additional planning to achieve comfortable retirement.

Fiduciary advisors typically charge in one of three ways: assets under management fees (usually 0.5-1.5% annually), hourly rates ($150-400 per hour), or fixed project fees ($1,000-5,000 for comprehensive plans). For teachers with smaller portfolios, hourly or project-based fees often provide better value than percentage-based fees.

Most 403(b) vendors are not fiduciaries when providing individual investment advice, even though the plan itself has fiduciary oversight. They typically operate under suitability standards and may earn commissions from recommended products. If you want fiduciary advice, look for fee-only advisors or RIAs who specialize in teacher retirement planning.

District retirement counselors provide valuable information about your pension benefits but typically cannot give personalized investment advice. They focus on explaining TRS rules and benefit calculations. A fiduciary provides comprehensive retirement planning that integrates your pension with other savings strategies and considers your complete financial picture.

Absolutely. Teacher retirement planning involves unique considerations like pension systems, 403(b) plans, and educator-specific challenges. A fiduciary who understands these complexities can provide much more valuable guidance than a generalist. Look for advisors who regularly work with teachers and understand your state’s retirement system.

Ask directly: “Are you serving as my fiduciary?” Request this commitment in writing. Check their Form ADV if they’re an RIA, or their firm’s disclosure documents. If they receive commissions from recommended products or can’t clearly confirm fiduciary status, they’re likely operating under suitability standards.

Don’t panic, but do evaluate your situation. Review all recommendations and fees you’ve been charged. Consider whether the advice and products truly serve your best interests. If you’re concerned about conflicts of interest or high fees, start researching fee-only fiduciary advisors who specialize in teacher retirement planning.

Yes, fiduciary breaches can result in legal action and regulatory complaints. You can file complaints with the SEC (for RIAs), state securities regulators, or relevant professional organizations. Fiduciaries can be held liable for losses resulting from breach of their fiduciary duty, which provides stronger protection than suitability standards.

If you’ve been working with non-fiduciary advisors or haven’t established any retirement planning relationship, here’s your action plan for securing proper fiduciary protection.

Start by reviewing any existing financial relationships. Gather documentation on fees paid, products purchased, and advice received. Calculate the total costs of your current arrangements and assess whether recommendations truly serve your best interests.

For Texas teachers, pay special attention to 403(b) plan fees and investment options. Many teacher-targeted products carry high fees that erode retirement savings over time.

Use these resources to find qualified fiduciary advisors:

Focus on advisors who specifically mention teacher retirement planning or public sector benefits in their marketing materials.

Schedule consultations with 2-3 potential advisors. During these meetings:

If you’re unsure about ongoing advisory relationships, consider starting with project-based fiduciary advice. Common projects for teachers include:

While working toward a fiduciary relationship, apply fiduciary principles to your own decisions:

The more you understand about retirement planning, the better you can evaluate fiduciary advice. Focus on learning about:

This knowledge helps you ask better questions and recognize quality fiduciary advice when you receive it.

Remember, securing fiduciary protection for your retirement planning is an investment in your future financial security. The time and effort you spend finding the right advisor can result in significantly better retirement outcomes and greater peace of mind throughout your teaching career.

By understanding what fiduciary protection means and how to secure it, you’re taking a crucial step toward the retirement security you deserve after dedicating your career to educating others. A true fiduciary will help ensure your financial future receives the same level of care and attention you’ve given to your students throughout your teaching career.

Use the TRS calculator to estimate your pension and identify potential income gaps.