How to Build a Guaranteed Income Floor as a Teacher

Stable income is the foundation of retirement security. Learn how to build it.

Retiring during a downturn can impact your income long-term. Learn what to expect.

Market downturns don’t follow retirement schedules. If you’re planning to retire during market crash teachers often discover their carefully planned exit strategy can unravel quickly when portfolios lose value right before or after leaving the classroom.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

Texas teachers face unique challenges during market volatility. Your TRS pension provides stability, but the 403(b), personal savings, and other retirement accounts that supplement your pension can lose significant value just when you need them most.

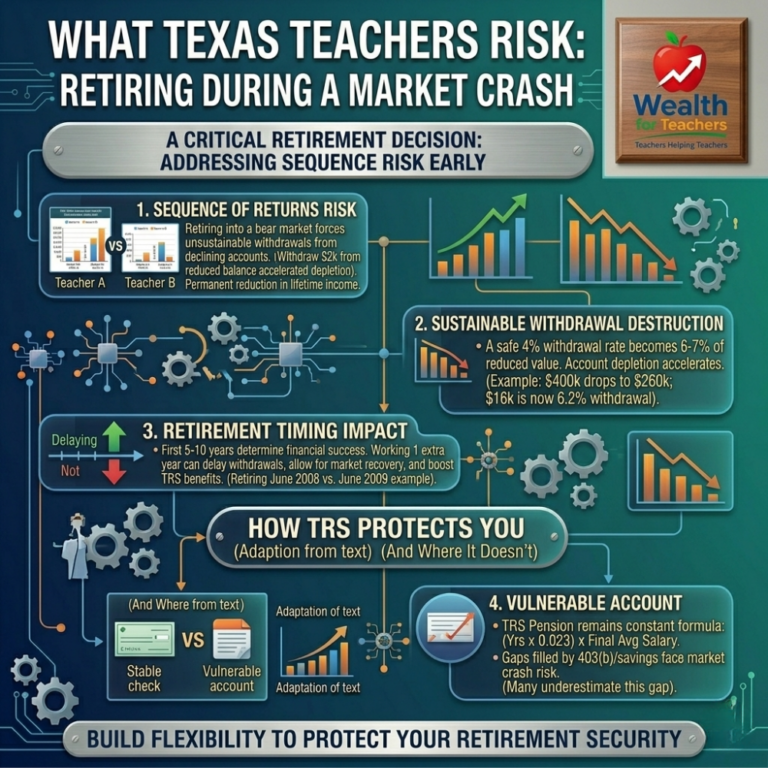

The timing of when you retire relative to market performance can impact your financial security for decades. This isn’t about short-term market fluctuations—it’s about understanding how a major downturn during your first few retirement years can permanently reduce your lifetime income.

This comprehensive Texas Teacher Retirement Planning Guide approach helps you understand what happens when retirement timing collides with market crashes and what you can do to protect yourself.

Most retirement plans look great on paper but crumble under real-world market stress. Teachers who retire with perfectly calculated spreadsheets often discover their assumptions about withdrawal rates, account balances, and income needs don’t survive contact with actual market volatility.

When markets crash during your first few retirement years, the damage goes far beyond temporary portfolio losses. You’re withdrawing money from declining accounts to pay living expenses, which means you’re selling investments at depressed prices.

Use the TRS calculator to estimate your pension and identify potential income gaps.

Here’s what happens: If your 403(b) drops 30% in value and you still need to withdraw $2,000 monthly for living expenses, you’re now taking a much larger percentage of your remaining balance. When markets recover, you have fewer shares left to participate in the rebound.

This creates a permanent reduction in your account value that never fully recovers, even when markets return to previous highs. The mathematical term for this is sequence of returns risk, and it’s one of the most dangerous threats to teacher retirement security.

Many Texas teachers plan to withdraw 4% annually from their retirement accounts to supplement their TRS pension. This seems safe based on historical data, but it assumes average market returns throughout retirement.

During a market crash, that 4% withdrawal becomes 6% or 7% of your reduced account value. You’re forced into unsustainable withdrawal rates that accelerate portfolio depletion.

Consider a teacher with $400,000 in their 403(b) planning to withdraw $16,000 annually (4%). If the market drops 35% in the first year of retirement, their account falls to $260,000. That same $16,000 withdrawal now represents 6.2% of the portfolio—well above sustainable levels.

Sequence risk affects Texas teachers differently than other retirees because of how TRS pensions interact with personal savings. Your TRS pension provides stable income, but most teachers need additional income from 403(b) accounts and personal savings to maintain their lifestyle.

The problem intensifies because many teachers retire in their late 50s or early 60s, giving them longer retirement periods where sequence risk can compound. A teacher who retires at 58 with 30 years of service could face 25-30 years of retirement—plenty of time for poor early returns to devastate long-term income.

The first 5-10 years of retirement determine your long-term financial success more than any other period. Poor returns during these critical years can reduce your lifetime income by 20-40%, even if markets perform well later.

This is especially problematic for Texas teachers who often have significant portions of their retirement savings in growth-oriented investments. The same portfolio allocation that built wealth during your working years can destroy income security if markets crash early in retirement.

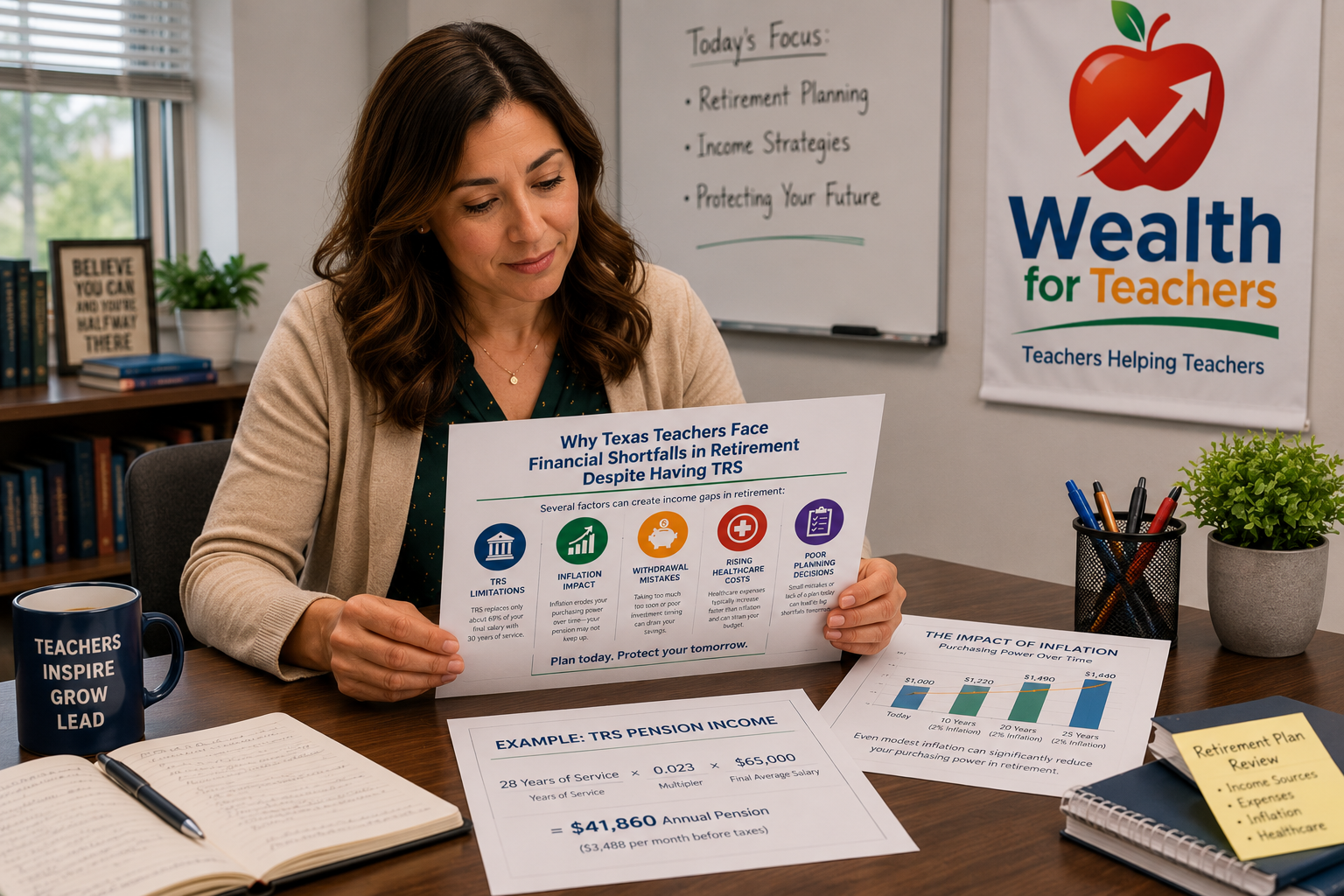

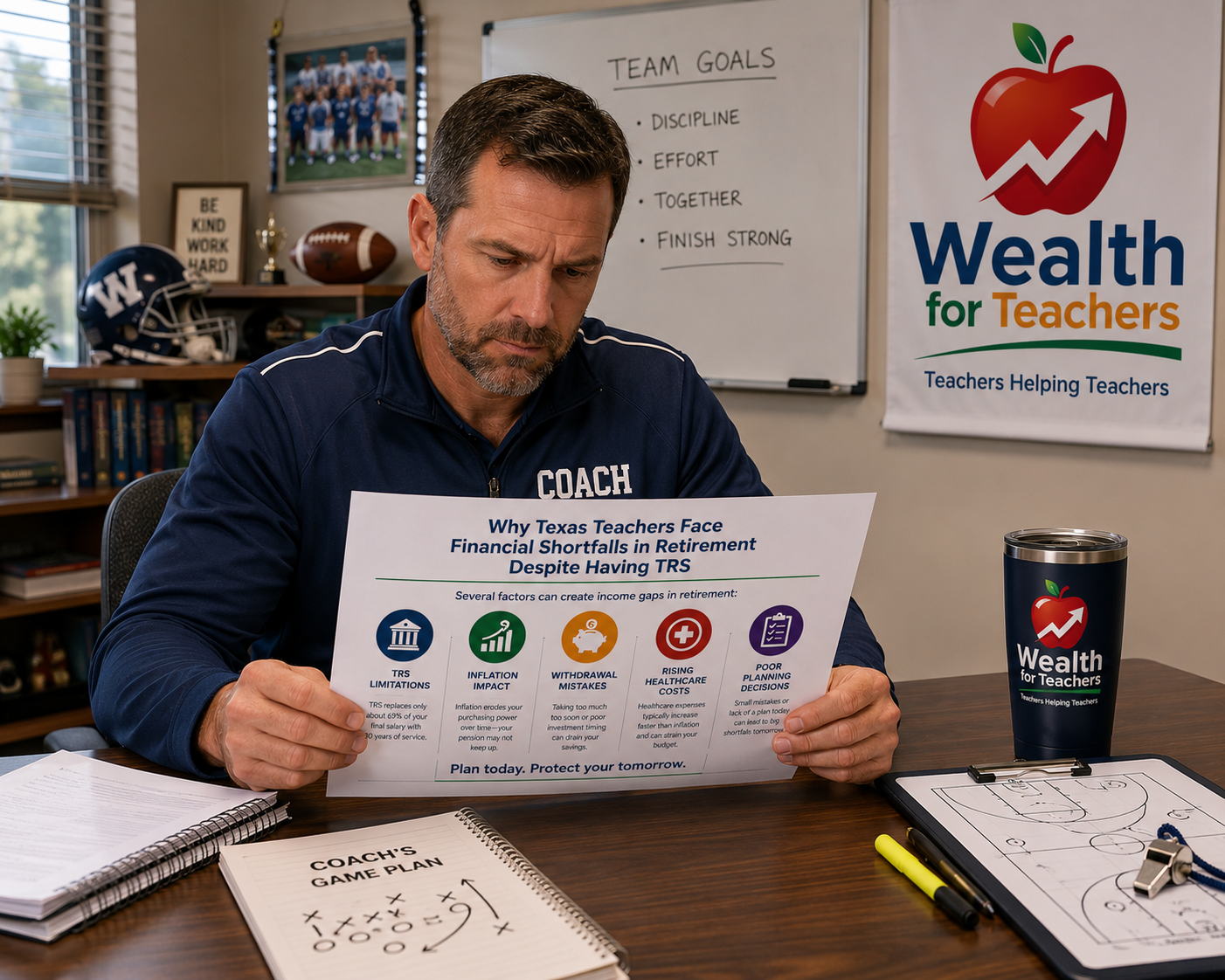

Your Texas TRS pension provides crucial protection during market downturns. The pension formula—Annual Pension = (Years of Service × 0.023) × Final Average Salary—remains constant regardless of market performance.

If you have 25 years of service and a final average salary of $65,000, your annual TRS pension equals $37,375 whether the stock market rises or falls. This stable income foundation protects you from the worst effects of market volatility.

However, TRS likely covers only 50-70% of your pre-retirement income. The TRS income replacement rate varies based on your salary level and years of service, but most teachers need additional income sources to maintain their standard of living.

The income gap between your TRS pension and your actual needs must be filled by 403(b) accounts, personal savings, Social Security, and other sources. These variable income sources are vulnerable to market crashes in ways your TRS pension is not.

Many teachers underestimate this gap until they’re already retired. They assume their pension will be sufficient, only to discover that inflation, healthcare costs, and lifestyle needs require more income than TRS provides.

The 2008 financial crisis provides a clear example of sequence risk in action. Two identical Texas teachers with similar savings faced dramatically different outcomes based solely on their retirement timing.

This teacher retired just before the market crash with $350,000 in their 403(b). They planned to withdraw $14,000 annually (4%) to supplement their TRS pension. The market dropped 37% during their first year of retirement, reducing their account to $220,500 after withdrawals.

Even though markets recovered over the following years, this teacher’s portfolio never fully caught up. By taking withdrawals during the downturn, they had fewer shares to participate in the recovery. Their account balance remained permanently impacted.

This teacher delayed retirement by one year, continuing to contribute to their 403(b) while markets were depressed. They purchased shares at low prices and retired after the worst of the crash had passed. Their portfolio had more time to recover before they began systematic withdrawals.

The one-year delay in retirement timing resulted in significantly higher lifetime income—potentially $200,000 or more over a 25-year retirement period.

The key to surviving retirement during a market crash is building flexibility into your retirement plan before you need it. This means creating multiple layers of protection and having specific strategies for different market scenarios.

Maintain 2-3 years of living expenses in cash or conservative investments before retiring. This allows you to avoid selling growth investments during market downturns. You can live off cash reserves while waiting for markets to recover.

For Texas teachers, this might mean keeping $50,000-75,000 in money market accounts or CDs to supplement your TRS pension during market volatility. The exact amount depends on the gap between your pension and total income needs.

Diversify beyond your TRS pension and 403(b) by developing retirement income streams that aren’t tied to market performance. This might include rental property, part-time work, or other investments that provide steady cash flow.

The goal is reducing your dependence on portfolio withdrawals during the critical early years of retirement. Even small additional income sources can dramatically reduce sequence risk.

If possible, build flexibility into your retirement date. This doesn’t mean trying to time the market perfectly, but rather having the option to delay retirement by 6-12 months if markets crash right before your planned exit.

Working one additional year during a market downturn can provide multiple benefits: continued contributions to your 403(b), delayed withdrawals, higher TRS benefits, and more time for market recovery.

Every Texas teacher’s situation is different, but there are common decision paths that can help you determine the best approach for your circumstances.

If your TRS pension replaces 70% or more of your pre-retirement income, you have more flexibility to weather market downturns. You can afford to be more conservative with personal savings since you’re less dependent on portfolio withdrawals.

Consider: Focus on capital preservation over growth in the years leading up to retirement. Build a modest cash reserve and consider more conservative asset allocation.

Risk: Don’t assume your pension is enough. Inflation and healthcare costs can erode purchasing power over time.

Most Texas teachers fall into this category. Your TRS pension provides a solid foundation, but you need significant additional income from personal savings. This makes you vulnerable to sequence risk.

Consider: Build substantial cash reserves and plan for flexible withdrawal strategies. Consider delaying Social Security to increase future revenue.

Use the TRS calculator to estimate your pension and identify potential income gaps.