Should Teachers Use Roth Conversions Before Retirement?

Roth conversions can reduce taxes—but only if used correctly.

Roth conversions can reduce taxes—but timing matters. Learn when to use them.

Roth conversions promise tax-free retirement income. But most Texas teachers who use them make critical timing errors that wipe out years of potential savings.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

The problem isn’t with Roth conversions themselves. The problem is converting at the wrong time, in the wrong amounts, or without understanding how your Texas TRS pension affects your tax brackets.

This comprehensive guide shows you exactly when roth conversion teachers strategies work—and when they backfire spectacularly. You’ll learn the specific decision framework Texas teachers need to time conversions correctly and avoid the most expensive mistakes.

For broader retirement planning context, start with our Texas Teacher Retirement Planning Guide to understand how Roth conversions fit into your complete retirement strategy.

Most retirement plans fail because they’re never tested under real-world conditions. Teachers often make conversion decisions based on oversimplified assumptions about future tax rates, TRS income timing, and withdrawal needs. By the time they discover the gaps, it’s too late to fix them.

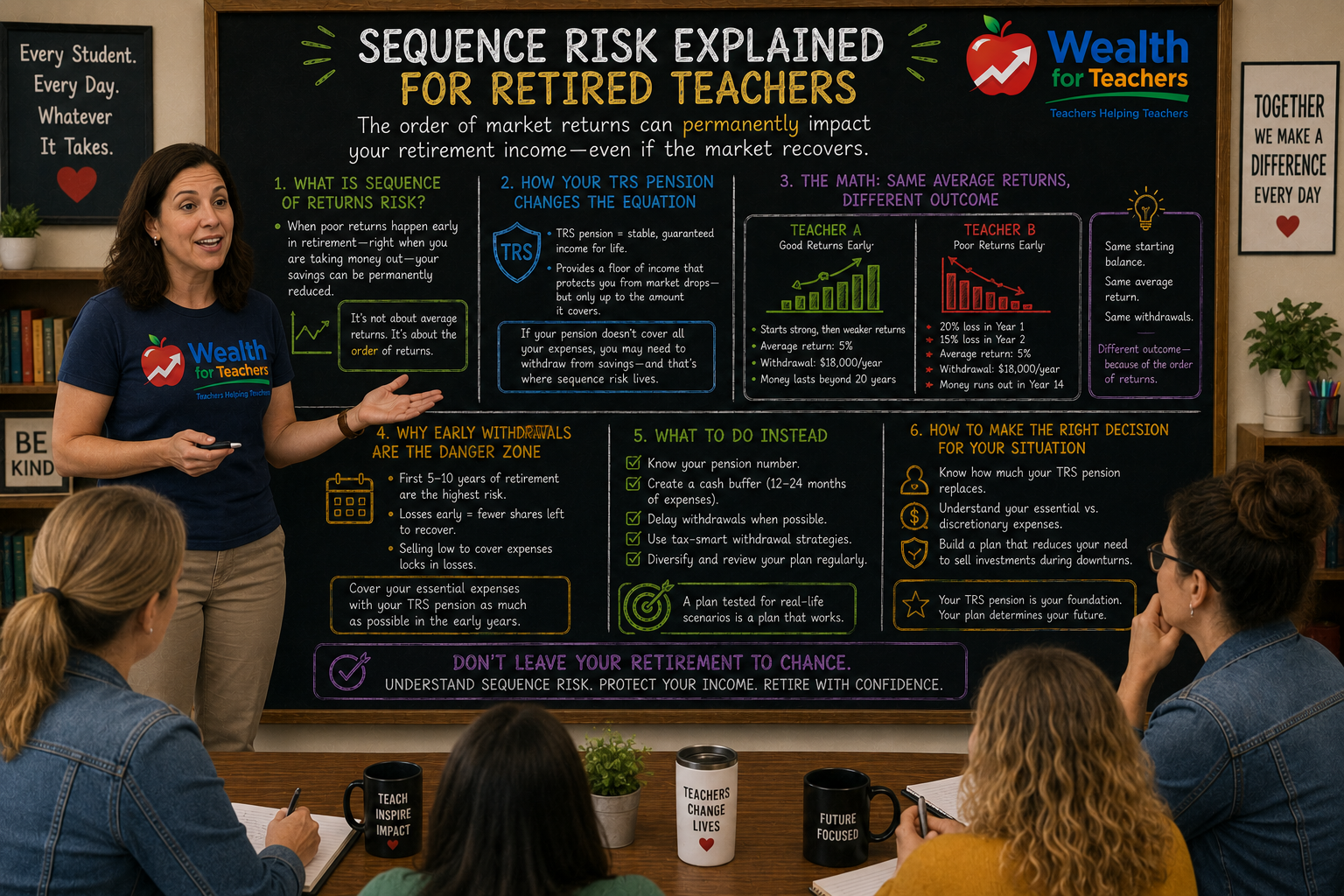

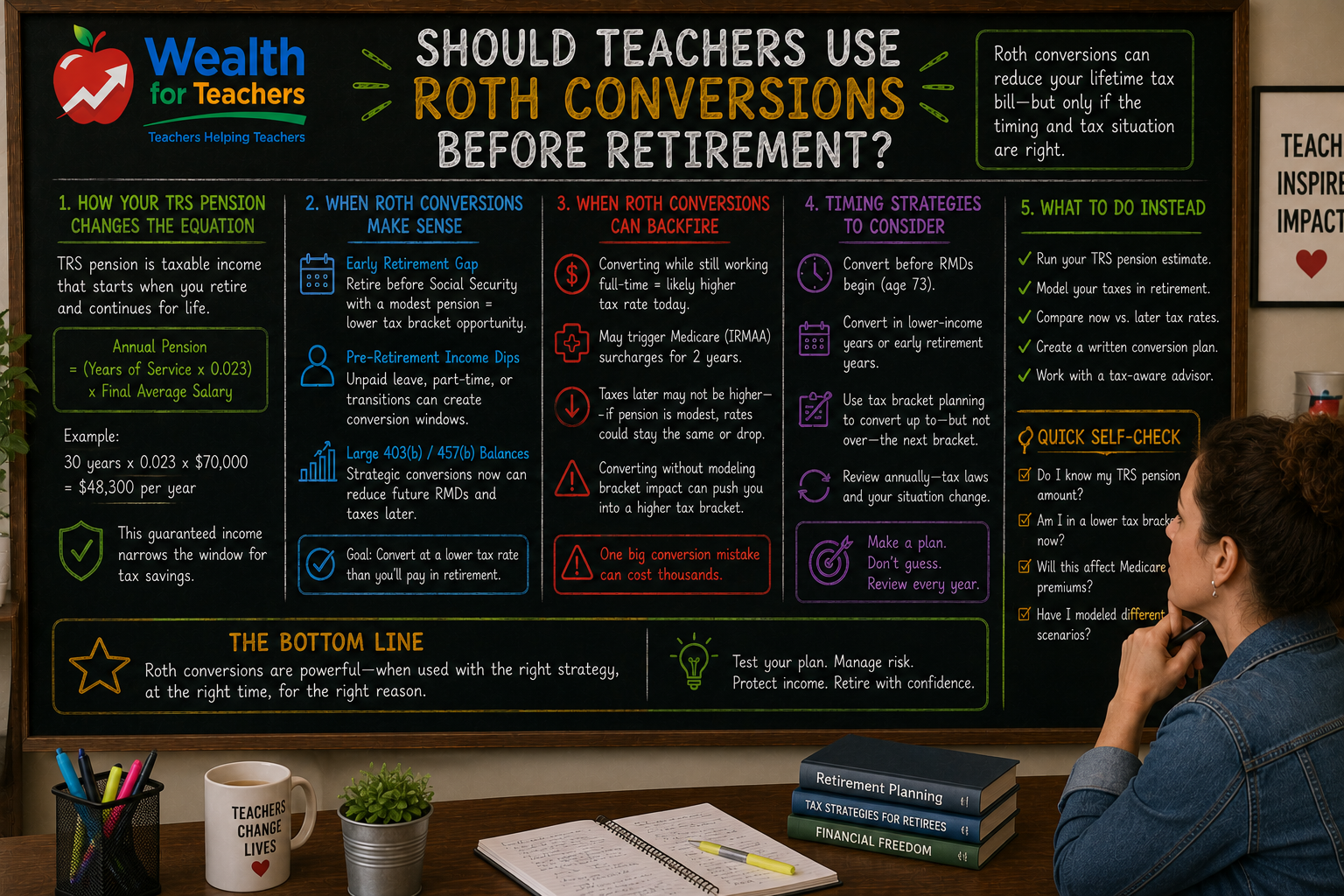

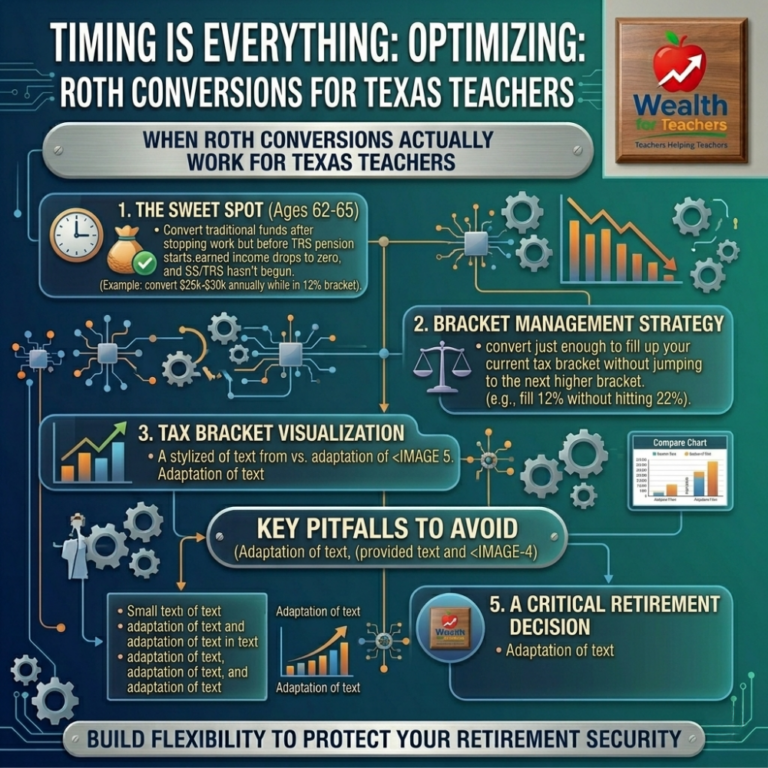

Roth conversions work best when you convert traditional IRA or 403(b) money during low-income years—before your TRS pension starts or during early retirement.

Use the TRS calculator to estimate your pension and identify potential income gaps.

The sweet spot for most Texas teachers: ages 62 to 65, after you’ve stopped working but before you start collecting TRS benefits.

Here’s why this window matters:

Consider Sarah, a Texas teacher with 30 years of service. Her TRS pension will be approximately $48,000 annually (30 years × 0.023 × $70,000 final average salary). If she retires at 62 but waits until 65 to start TRS benefits, she has three years of potentially lower tax brackets for conversions.

During those three years, Sarah could convert $25,000 to $30,000 annually from her 403(b) to a Roth IRA while staying in the 12% tax bracket, assuming she has no other significant income sources.

Most teachers underestimate how much income they’ll have in retirement. This is the biggest conversion planning mistake.

Your retirement income sources likely include:

Many Texas teachers assume they’ll be in lower tax brackets during retirement. But if your TRS pension replaces 60% to 80% of your pre-retirement income, plus you add Social Security and investment withdrawals, you might land in the same tax bracket—or higher.

This is why the timing of conversions matters more than the amount. Converting $50,000 while you’re still working and earning full salary could push you into the 24% tax bracket. Converting the same amount during a low-income window might only cost you 12% in taxes.

The difference? $6,000 in unnecessary taxes on that single conversion.

Before making any conversion decisions, project your retirement income accurately:

If this total income keeps you in higher tax brackets, conversions during working years rarely make sense. If retirement income drops you into lower brackets, you might skip conversions entirely and pay taxes on withdrawals later.

Smart conversion strategy focuses on bracket management, not conversion amounts.

The goal: convert just enough to fill up your current tax bracket without jumping to the next higher bracket.

For 2024 tax brackets (married filing jointly):

If your current income puts you at the top of the 12% bracket, you have no room for conversions without jumping to 22%. But if you’re early in the 12% bracket, you might have $20,000 to $40,000 of conversion capacity.

This is where withdrawal sequencing strategy becomes critical—the order you tap different account types affects your conversion opportunities and overall tax burden.

Don’t try to convert everything in one year. Spread conversions across multiple low-income years.

Example: Instead of converting $120,000 in one year (which could push you into higher brackets), convert $30,000 per year across four years. This keeps you in consistent, lower tax brackets and reduces the total tax bill.

This strategy works especially well for teachers who retire before TRS pension eligibility and have a few years of lower income before benefits begin.

Roth conversions backfire when teachers make these critical errors:

Converting while you’re still working full-time usually fails. You’re already in higher tax brackets from your teaching salary. Adding conversion income on top pushes you even higher.

The result: you pay 22% or 24% taxes on conversions now, only to withdraw the money tax-free later when you might have been in the 12% bracket anyway.

Texas has no state income tax, which actually makes conversions more attractive than in high-tax states. But if you plan to retire to a state with income taxes, conversions while you’re still a Texas resident could save you state taxes on the converted amounts.

Conversely, if you’re moving from a high-tax state to Texas, you might want to wait and convert after the move to avoid state taxes on the conversion income.

Conversions trigger immediate tax bills. If you don’t have cash outside retirement accounts to pay these taxes, you’ll need to withhold taxes from the conversion itself—which defeats the purpose.

Never convert unless you can pay the taxes from other sources. This often means building multiple income streams that include accessible cash reserves.

Many teachers convert assuming tax rates will skyrocket in the future. While rates might increase, your personal tax situation might not follow national trends.

If your retirement income is significantly lower than your working income—which happens for some teachers with modest savings—you might be in lower brackets regardless of future rate changes.

Probably not. Large conversions push you into higher tax brackets and create massive tax bills. Instead, consider partial conversions spread across multiple years, focusing on filling up lower tax brackets.

Yes, but it’s usually not optimal. Your teaching salary already puts you in higher brackets. Adding conversion income makes the tax cost even higher. Wait for lower-income years when possible.

Current Roth contributions while working make more sense than conversions for most teachers. You’re paying the same tax rate, but contributions don’t create additional taxable income in the year you make them.

Required minimum distributions start at age 73 and force taxable withdrawals from traditional accounts. Converting before RMDs begin can reduce the size of these accounts and lower future RMD obligations. This strategy becomes more important as you approach age 70, when conversion windows start closing. Understanding RMD planning helps you time conversions more effectively.

Maybe. Inherited Roth IRAs grow tax-free for heirs, while inherited traditional IRAs create tax bills for your beneficiaries. But this depends on your heirs’ tax situations and your own retirement income needs.

Rather than rushing into conversions, focus on building a comprehensive withdrawal plan.

Use the TRS calculator to estimate your pension and identify potential income gaps.