How to Build a Guaranteed Income Floor as a Teacher

Stable income is the foundation of retirement security. Learn how to build it.

Withdrawal order matters more than most teachers realize. Learn how to optimize taxes.

Most Texas teachers focus on accumulating retirement savings but give little thought to how they’ll withdraw those funds. This oversight can cost you thousands of dollars in unnecessary taxes over your retirement years.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

The order in which you tap different retirement accounts – your TRS pension, 403(b), Roth IRA, and taxable investments – directly impacts your tax bill. Getting this withdrawal strategy taxes teachers approach wrong means you could pay 20% to 30% more in taxes than necessary.

Your Texas Teacher Retirement Planning Guide should include a clear withdrawal sequence that minimizes your lifetime tax burden while maximizing your income security.

Most retirement plans fail because they focus solely on accumulation without testing how the withdrawal phase will actually work under real market conditions, changing tax laws, and unexpected life events.

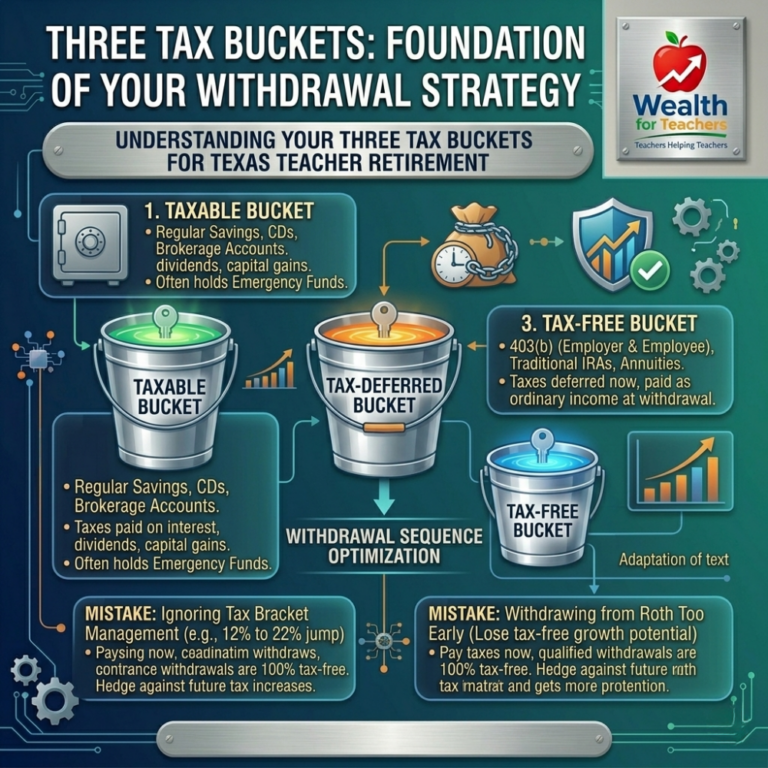

Every retirement dollar you own falls into one of three tax categories, or “buckets.” Understanding these buckets is fundamental to creating an effective withdrawal strategy taxes teachers can actually implement.

Use the TRS calculator to estimate your pension and identify potential income gaps.

This includes regular savings accounts, CDs, brokerage accounts, and any investments held outside of retirement accounts. You’ve already paid taxes on the money going in, but you’ll pay taxes on any interest, dividends, or capital gains.

For teachers, this bucket often includes:

These accounts let you defer taxes until withdrawal. You get a tax deduction now but pay ordinary income tax rates when you withdraw.

Texas teachers typically have:

You pay taxes on money going into these accounts, but qualified withdrawals come out completely tax-free.

This includes:

The conventional wisdom suggests withdrawing from accounts in this order: taxable first, tax-deferred second, and tax-free last. This approach aims to let your tax-free accounts grow as long as possible while managing your current tax burden.

Start with your taxable investments. These accounts don’t have required minimum distributions, and you can often manage the tax impact by choosing which investments to sell and when.

If you have $50,000 in taxable investments earning 6% annually, withdrawing $4,000 per year means you’re only paying taxes on a small portion (the gains), not the full withdrawal amount.

Once your taxable accounts are depleted, move to your 403(b) and traditional IRA accounts. Every dollar withdrawn counts as ordinary income, but you’ve delayed these taxes for decades.

Save your Roth accounts for last. Since withdrawals are tax-free, these accounts provide the most flexibility and can serve as a hedge against future tax increases.

Your TRS pension adds complexity to the standard withdrawal sequence because it’s not a bucket you control. Once you start your TRS pension, you receive monthly payments whether you need them or not.

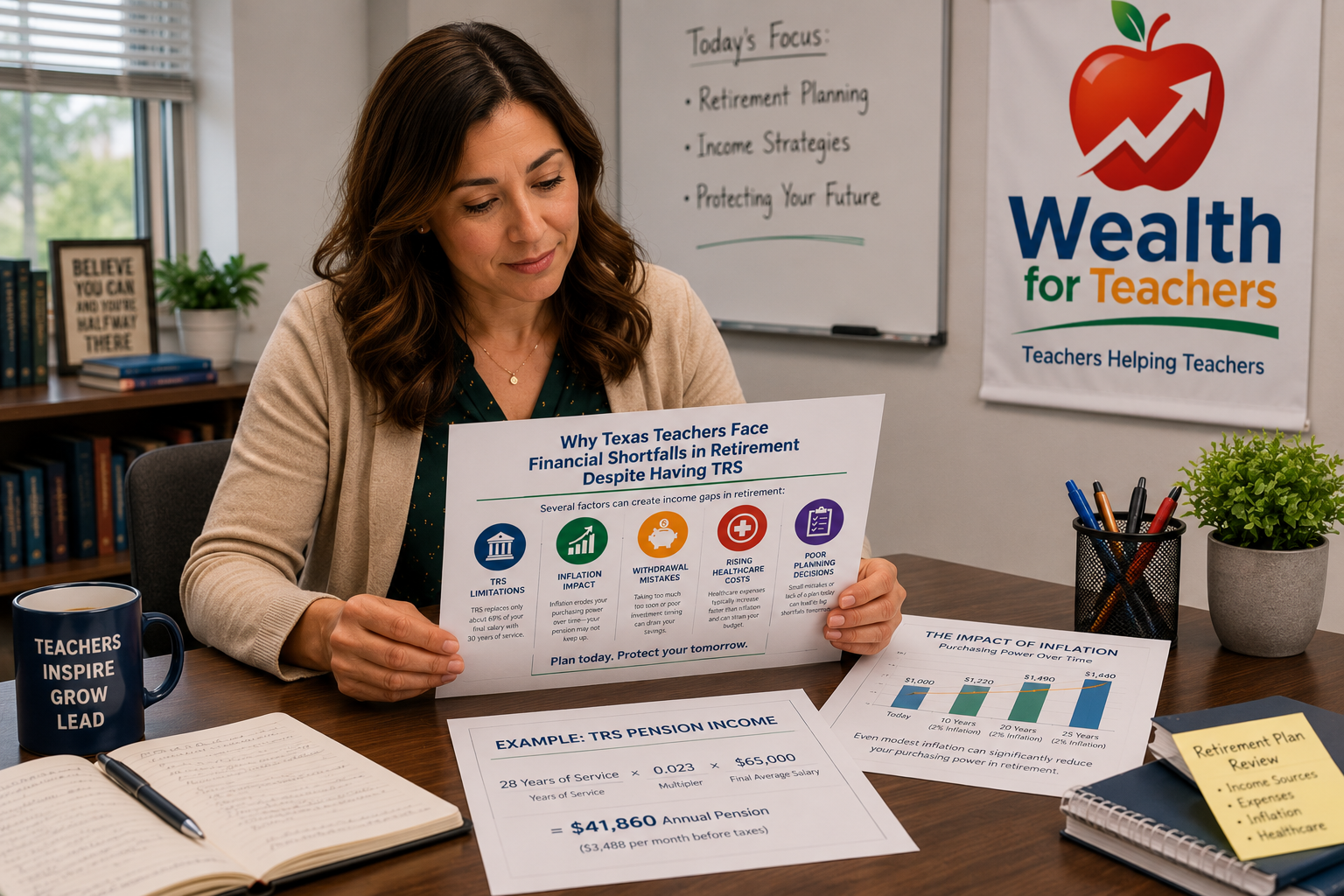

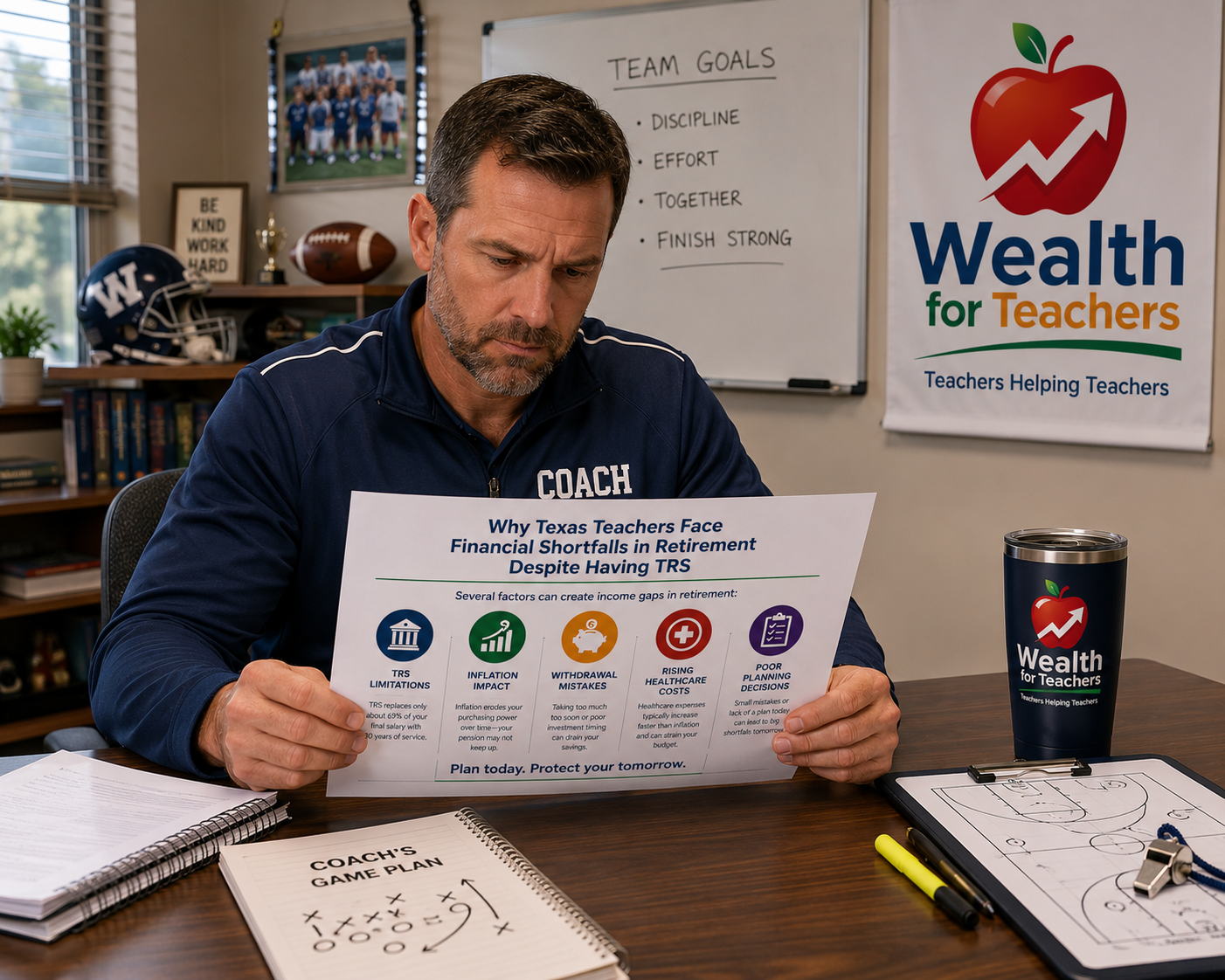

A Texas teacher with 25 years of service and a final average salary of $60,000 receives an annual TRS pension of $34,500 (25 × 0.023 × $60,000). This pension income affects which tax bracket you’re in and how much room you have for additional withdrawals.

Many teachers need income between their retirement date and when they start their TRS pension. If you retire at 58 but don’t start TRS until 65, you need seven years of bridge income.

During this bridge period, you might withdraw from taxable accounts first, then consider Roth conversions from your 403(b) to take advantage of potentially lower tax brackets before your pension begins.

Once your TRS pension begins, your retirement income streams become more complex. You’re receiving guaranteed pension income while also needing to manage withdrawals from other accounts for additional expenses.

Texas teachers have an advantage other teachers don’t: no state income tax. This affects your withdrawal strategy because you only need to consider federal tax implications.

A teacher moving from a high-tax state to Texas in retirement might want to accelerate withdrawals from tax-deferred accounts to take advantage of the state tax savings.

Unlike teachers in some states, Texas teachers don’t participate in Social Security for their teaching service. Your TRS pension needs to replace both the traditional pension and Social Security benefits that other retirees receive.

This means your supplemental retirement accounts (403(b), Roth IRA) play a larger role in your overall retirement security, making your withdrawal strategy even more critical.

Your RMD strategy becomes crucial when you turn 73. These mandatory withdrawals from tax-deferred accounts can push you into higher tax brackets, especially when combined with your TRS pension.

Many teachers withdraw retirement funds without considering their marginal tax rate. Taking a large withdrawal that pushes you from the 12% bracket to the 22% bracket means you pay an extra 10% on every dollar above the threshold.

Teachers often accumulate large 403(b) balances without considering how RMDs will affect their tax situation. A teacher with $500,000 in their 403(b) at age 73 faces an RMD of approximately $18,800 in their first year.

Some teachers tap their Roth accounts first because the withdrawals are tax-free. This strategy wastes the tax-free growth potential and leaves you with higher-taxed accounts for later years.

Healthcare expenses often increase in retirement, but many teachers don’t coordinate their withdrawal strategy with medical needs. Higher income from poor withdrawal timing can affect Medicare premiums and other income-based healthcare costs.

Create a year-by-year withdrawal plan that considers your expected tax brackets, required minimum distributions, and major expense timing.

Calculate your expected tax bracket each year of retirement, including your TRS pension, Social Security (if applicable), and any part-time work income. Look for opportunities to fill up lower tax brackets with strategic withdrawals.

In years when you’re in lower tax brackets (often the early retirement years before TRS and Social Security begin), consider converting some traditional 403(b) funds to Roth accounts. You pay taxes now but eliminate future RMDs and create tax-free income for later years.

If you know you’ll need $30,000 for a new roof or major medical expense, plan which accounts to use and spread the withdrawal over multiple years if it helps manage tax brackets.

During market downturns, you might adjust your withdrawal sequence to avoid selling investments at losses while maintaining your required cash flow. Understanding sequence of returns risk helps you make these tactical adjustments.

Your optimal withdrawal strategy depends on your specific circumstances. Here are the most common situations Texas teachers face:

When this applies: You retire before age 65 and need income before starting your TRS pension.

What to consider: Use taxable accounts first to bridge the gap, but consider Roth conversions if you’re in a low tax bracket. Avoid early 403(b penalties.

Use the TRS calculator to estimate your pension and identify potential income gaps.