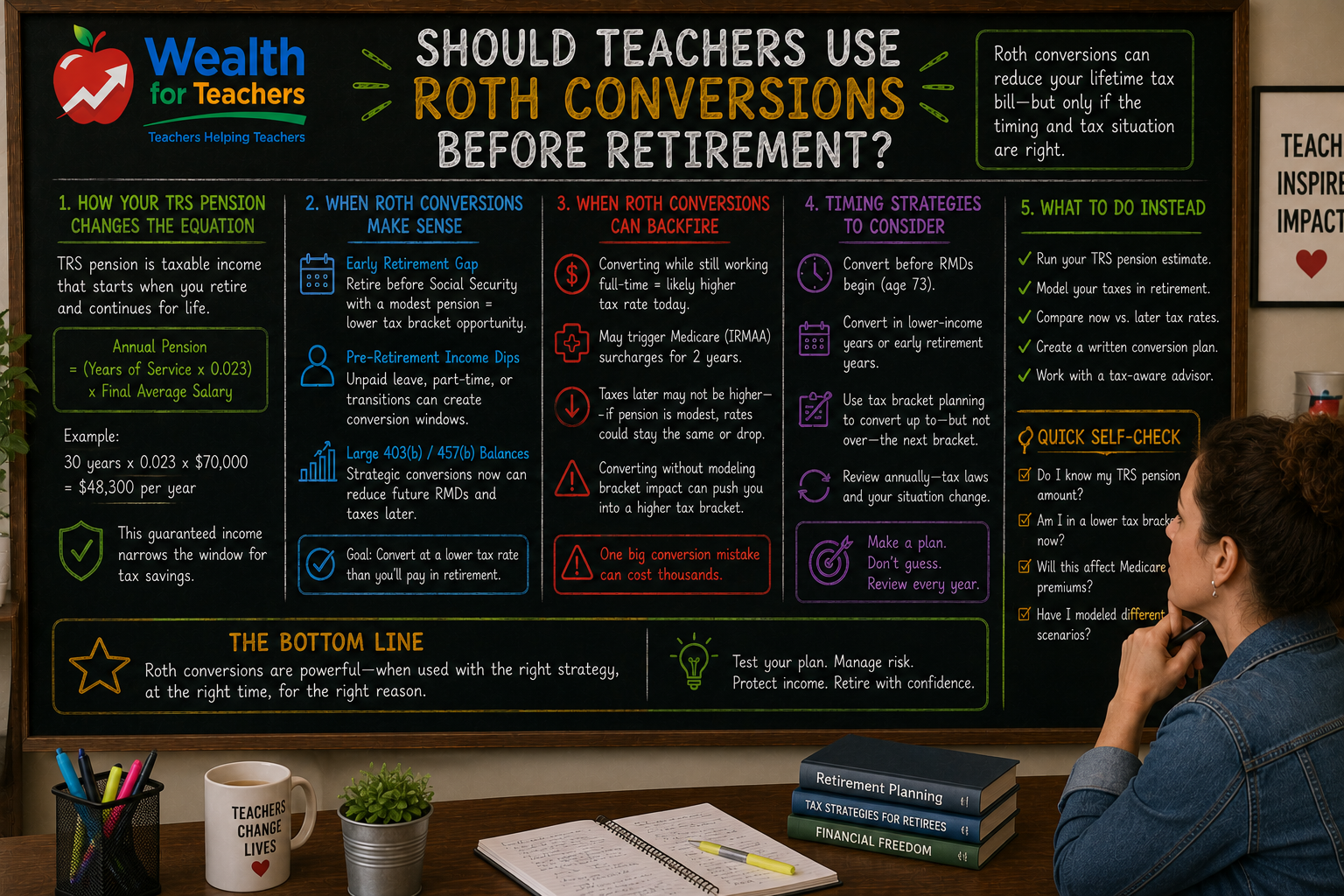

Should Teachers Use Roth Conversions Before Retirement?

Roth conversions can reduce taxes—but only if used correctly.

Teacher retirement works differently than traditional plans. Learn why.

Teacher retirement vs traditional retirement isn’t just about different account types. It’s about fundamentally different financial structures, risks, and planning requirements that most educators never fully understand until they’re facing retirement decisions.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

While traditional employees rely on 401k accounts and Social Security, Texas teachers navigate a complex web of TRS pension calculations, service credit requirements, and timing decisions that can affect their income for decades. Make the wrong choice, and you could lose thousands of dollars per year in retirement income.

The stakes are higher because teacher retirement decisions are often irreversible. Unlike a 401k worker who can adjust their withdrawal strategy, teachers who retire at the wrong time or with the wrong understanding of their benefits face consequences they cannot undo.

For comprehensive guidance on navigating these unique challenges, our Texas Teacher Retirement Planning Guide breaks down every critical decision Texas educators face.

Most retirement plans fail because they are never tested under real-world conditions. Teachers often discover gaps in their understanding only when they’re already committed to retirement timing and benefit elections they cannot change.

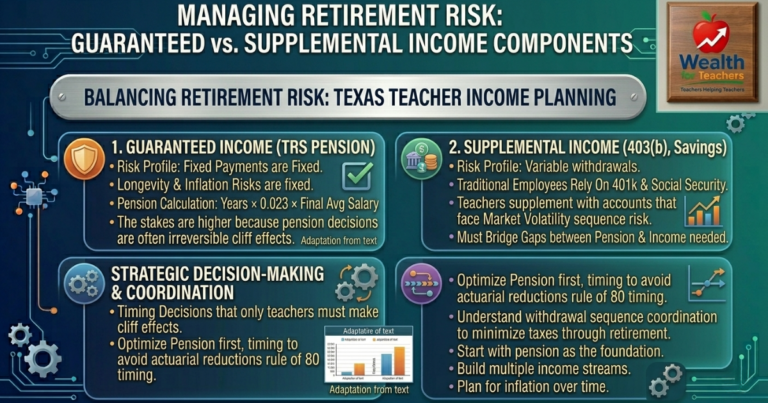

Texas teachers receive guaranteed monthly payments through TRS, not variable withdrawals from investment accounts. This creates a completely different income structure in retirement.

Use the TRS calculator to estimate your pension and identify potential income gaps.

Traditional retirement income comes from three sources: Social Security, employer-sponsored plans (like 401k), and personal savings. Teachers replace the middle component with a pension that follows strict calculation rules.

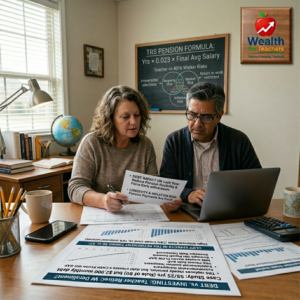

Your TRS pension equals your years of service times 2.3% times your final average salary. A teacher with 30 years of service and a $70,000 final average salary receives:

Traditional retirees with 401k accounts face market risk every year. Their withdrawal amount depends on account balance, market performance, and withdrawal strategy. Teachers with TRS pensions receive the same amount regardless of market conditions.

This fundamental difference affects every other retirement planning decision. Traditional retirees focus on accumulation and withdrawal strategies. Teachers must optimize pension calculations and supplement guaranteed income with other sources.

The “4% rule” and other traditional retirement guidelines assume you’re withdrawing from investment accounts. These rules become irrelevant when your primary income source is a guaranteed pension.

Traditional retirement planning asks: “How much do I need to save to replace my income?” Teacher retirement planning asks: “How do I maximize my pension calculation and fill the gaps?”

For example, a traditional worker earning $70,000 might aim to save $1.4 million to maintain their lifestyle (using a 5% withdrawal rate). A Texas teacher earning $70,000 with 30 years of service already has $48,300 in guaranteed annual income through TRS.

The teacher’s planning challenge becomes: “How do I bridge the $21,700 gap between my pension and my current income?” This requires different strategies than accumulating $1.4 million.

Traditional retirement planning emphasizes asset allocation and withdrawal strategies. Teacher retirement planning emphasizes service credit optimization, final salary maximization, and supplemental income planning.

Understanding these mathematical differences prevents teachers from following inappropriate advice designed for 401k-dependent retirees.

Teachers face longevity risk and inflation risk more acutely than traditional retirees because their pension payments are fixed. 401k retirees can adjust their withdrawals; teachers cannot adjust their pension amount.

Market risk affects teachers differently. While their pension is guaranteed, they still need supplemental savings for expenses beyond their pension replacement ratio. These supplemental accounts face the same market risks as traditional retirement accounts.

Teachers also face unique timing risks. Retiring too early means accepting reduced benefits permanently. Traditional workers can return to work if their 401k balance drops; teachers who elect early retirement cannot undo that decision.

The biggest risk difference is flexibility. Traditional retirees can adjust spending, change withdrawal rates, or return to work relatively easily. Teachers make irrevocable elections about benefit timing and options that affect their income for life.

For strategies on managing these risks through multiple income sources, teachers need planning approaches that account for both guaranteed and variable income components.

Traditional retirees can retire gradually, adjusting their withdrawal strategy as needed. Teachers face specific timing decisions with permanent consequences.

The rule of 80 allows Texas teachers to retire without penalty when their age plus years of service equals 80. Miss this calculation, and you face actuarial reductions that permanently lower your monthly pension.

For example, a teacher who could retire at age 58 with 25 years of service (totaling 83) receives their full pension calculation. If they retire at age 57 with 24 years of service (totaling 81), they still qualify for unreduced benefits. But retiring at age 56 with 23 years of service (totaling 79) results in permanent reductions.

Traditional workers don’t face these cliff effects. They can retire at 59.5, 60, 62, or any age they choose, adjusting their withdrawal strategy accordingly.

Teachers also must decide whether to purchase service credit to reach the rule of 80 sooner. This decision requires complex analysis of costs, benefits, and opportunity costs that traditional workers never encounter.

The timing of Roth conversions becomes more complex for teachers because they know their future pension income with certainty, unlike traditional retirees who estimate their withdrawal needs.

Do I get Social Security if I have a TRS pension?

Texas teachers do not pay into Social Security and do not receive Social Security benefits based on their teaching service. You can earn Social Security benefits through other employment, but your TRS pension and Social Security are separate systems.

Can I withdraw money from TRS like a 401k?

No. TRS is a defined benefit pension that pays monthly income for life. You cannot take lump-sum withdrawals or control the payout timing like a 401k account. You can withdraw your contributions if you leave teaching before retirement eligibility.

What happens to my TRS pension if I die?

You elect survivor benefit options when you retire. Your choices affect your monthly pension amount and determine what your beneficiary receives after your death. This election is permanent and cannot be changed after retirement.

Should I max out my 403b or pay off my house first?

This depends on your pension replacement ratio, debt interest rates, and tax situation. Since your TRS pension is guaranteed, the analysis differs from traditional retirement planning where all income sources are variable.

Can I retire from TRS and work somewhere else?

Yes, but employment restrictions apply if you want to return to TRS-covered employment. You can work in private sector jobs or non-TRS public employment without affecting your pension.

Start with your TRS pension calculation as the foundation of your retirement income plan. Calculate your expected pension using your projected years of service and final average salary, then identify the income gap you need to fill through other sources.

Focus on optimizing your pension first. This might mean purchasing service credit, maximizing your final average salary through strategic career moves, or timing your retirement to avoid actuarial reductions.

Build supplemental savings in tax-advantaged accounts like 403b or 457 plans. Since you know your future pension income, you can make more informed decisions about Roth vs. traditional contributions based on your expected tax situation in retirement.

Plan for different phases of retirement. Your pension covers basic income needs, but you might want higher spending in early retirement or need to cover healthcare costs that increase over time.

Understanding withdrawal strategies becomes crucial when coordinating pension income with supplemental account distributions to minimize taxes throughout retirement.

If you’re within 5 years of the rule of 80: Focus on final salary maximization and pension optimization. Consider whether purchasing service credit makes financial sense. Avoid major financial decisions that could jeopardize your ability to reach rule of 80 timing. Review your beneficiary elections and survivor benefit options before retiring.

If you’re 10-15 years from retirement: Build supplemental savings aggressively while optimizing your pension trajectory. This is your highest-impact period for retirement planning decisions. Consider maxing out 403b contributions and exploring 457 plans. Plan career moves that could increase your final average salary.

If you’re early in your career (under 10 years of service): Understand your pension vesting schedule and focus on staying in TRS-covered employment if you plan to retire as a teacher. Build emergency savings before

Use the TRS calculator to estimate your pension and identify potential income gaps.