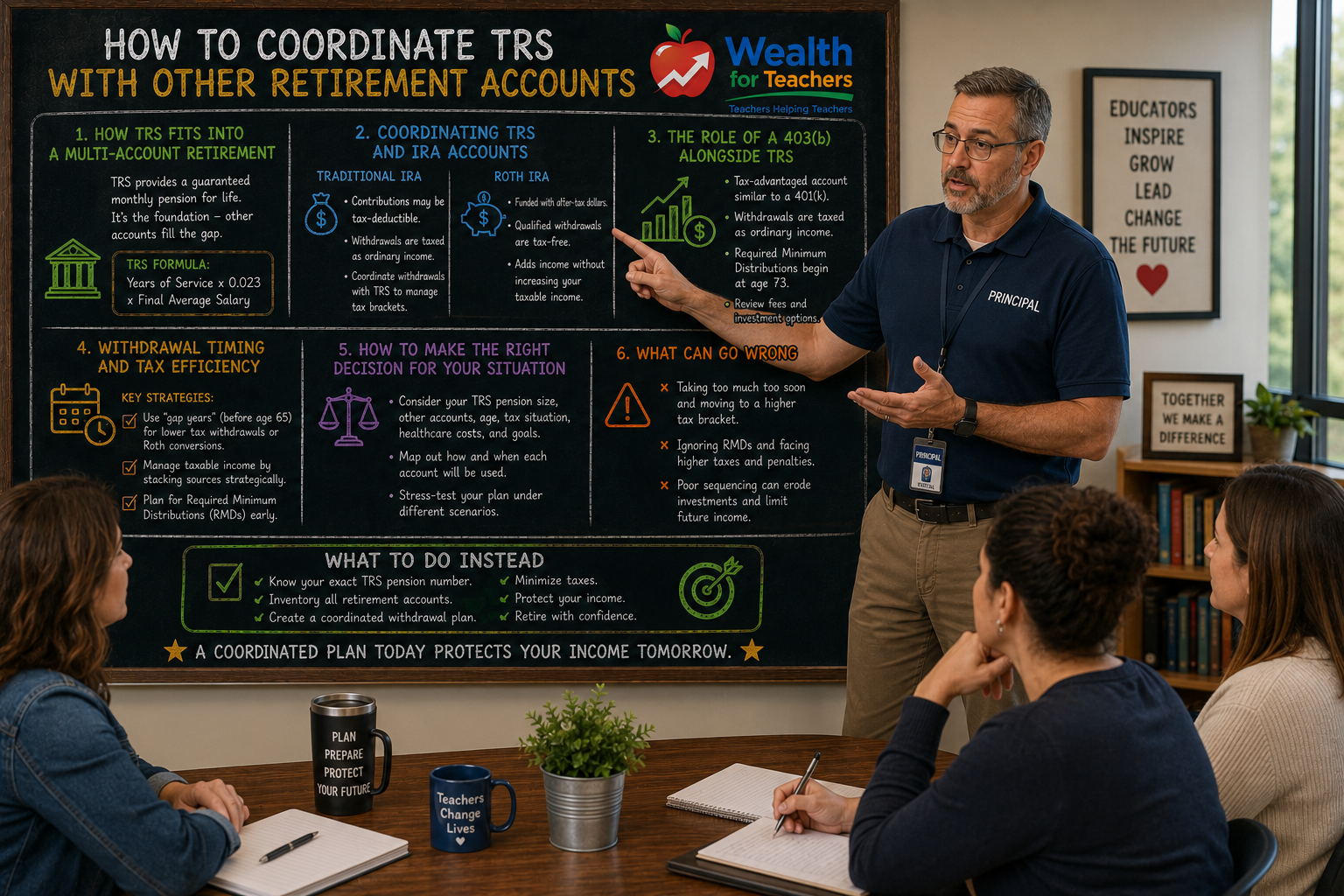

How to Coordinate TRS With IRAs, 403(b)s, and Other Accounts

TRS is only one piece of the puzzle. Learn how to align it with your other accounts.

Debt vs investing decisions can impact retirement security. Learn what to prioritize.

Teachers approaching retirement face a critical decision that can impact their financial security for decades: should you prioritize paying off debt or investing more in retirement accounts?

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

This decision becomes even more complex for Texas teachers because TRS provides a defined benefit pension, but it may not replace enough income to cover debt payments in retirement. Making the wrong choice can force you to work longer, reduce your standard of living, or tap retirement savings earlier than planned.

The math behind this decision depends on interest rates, your TRS pension amount, tax implications, and your personal risk tolerance. But the psychology of debt versus the reality of retirement cash flow often tells a different story than simple calculations suggest.

For comprehensive retirement planning strategies, see our Texas Teacher Retirement Planning Guide.

Most retirement plans fail because they are never tested under real-world conditions like market volatility, unexpected expenses, or changes in health. Teachers who understand how debt impacts their TRS retirement timeline and cash flow make better decisions than those who rely on generic financial advice.

The mathematical comparison between paying off debt and investing depends on guaranteed versus potential returns.

Use the TRS calculator to estimate your pension and identify potential income gaps.

When you pay off debt, you earn a guaranteed return equal to the interest rate you avoid. Credit card debt at 18% APR means paying it off gives you an immediate 18% return on your money.

Investment returns are never guaranteed. Historical stock market averages of 10% mean nothing if you retire during a bear market or need to withdraw funds when values are down.

Here’s how to calculate your personal break-even point:

But this math ignores a critical factor for Texas teachers: how debt payments affect your ability to reach TRS retirement eligibility and maintain cash flow in early retirement.

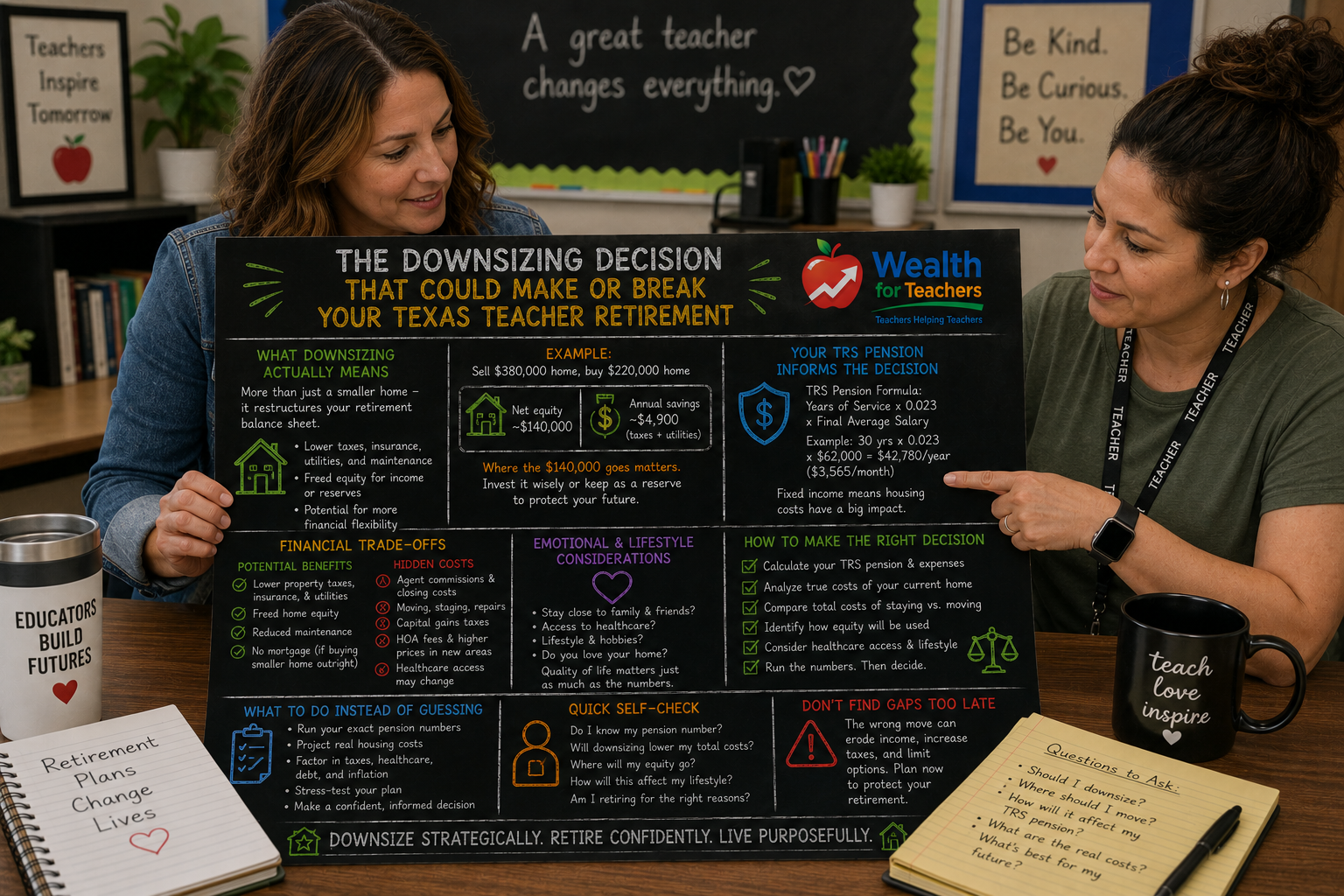

Texas TRS allows retirement with full benefits at age 65 with five years of service, or earlier with the Rule of 80 (age plus service years equals 80). Debt payments can force you to work longer than your ideal retirement timeline.

Consider this example: A 55-year-old teacher with 25 years of TRS service earns $65,000 annually. Her projected TRS pension would be $37,375 per year (25 × 0.023 × $65,000). However, she has $2,000 monthly debt payments totaling $24,000 annually.

Her net retirement income after debt payments would drop to just $13,375 annually – clearly insufficient. This forces her to either work longer, withdraw from retirement accounts early, or continue debt payments that consume most of her pension.

Debt payments in retirement create multiple problems:

Understanding how much income TRS really replaces helps you calculate whether debt payments will fit within your retirement budget.

TRS provides steady pension income, but it doesn’t start until you actually retire. This creates a cash flow gap that debt payments can make worse.

Many Texas teachers also rely on summer income from teaching summer school or other work. In retirement, this supplemental income disappears, making fixed debt payments harder to manage.

Here’s what happens to monthly cash flow for a typical Texas teacher retiring with debt:

Pre-retirement monthly income: $5,400

TRS pension monthly income: $3,115

Monthly debt payments: $800

Available spending money: $2,315

This represents a 57% reduction in available monthly cash flow – often requiring major lifestyle adjustments or additional income sources.

Teachers who eliminate debt before retirement maintain more flexibility and can focus on building multiple retirement income streams beyond TRS.

The emotional benefits of debt elimination often outweigh pure mathematical optimization for many teachers.

Debt creates psychological stress that can affect your enjoyment of retirement. Teachers who enter retirement debt-free report higher satisfaction and less financial anxiety, even when the math might have favored investing instead.

Your risk tolerance typically decreases as you approach and enter retirement. Having debt payments forces you to maintain higher investment risk to generate returns needed to service that debt.

Teachers nearing retirement often prefer the guaranteed “return” of debt elimination over the uncertainty of market-based investments, especially when considering sequence of returns risk in early retirement years.

The optimal debt payoff strategy depends on your specific situation, but here’s a framework that works for most Texas teachers:

Start with $1,000-$2,000 emergency fund before aggressive debt payoff. Teachers face unique risks like potential school budget cuts or extended summer breaks without pay.

If your district offers 403(b) matching, contribute enough to get the full match before paying extra on debt. This represents an immediate 100% return.

Pay off credit cards, personal loans, and other high-interest debt (above 8% APR) before increasing retirement investments.

For moderate-interest debt (4-8%), consider your timeline to TRS retirement eligibility and your risk tolerance.

Certain situations favor investing over aggressive debt payoff:

Teachers in their 40s or early 50s with stable employment and low-interest debt often benefit more from maximizing retirement contributions and taking advantage of compound growth.

Contributing to traditional 403(b) or 457 plans reduces your current taxable income while building retirement savings. If you’re in a higher tax bracket now than you expect in retirement, this tax deferral can be more valuable than paying off moderate-interest debt.

Understanding how to coordinate TRS with other retirement accounts helps optimize your overall tax strategy.

This depends on your interest rate, remaining balance, and other debt. If your mortgage payment fits comfortably within your projected TRS pension income and you have no other high-interest debt, keeping the mortgage might make sense. However, many teachers prefer the psychological benefit and cash flow improvement of entering retirement mortgage-free.

Student loan interest rates and forgiveness options affect this decision. Teachers with high-rate private loans should prioritize payoff. Those with low-rate federal loans might benefit more from income-driven repayment plans and focusing on retirement savings, especially if pursuing Public Service Loan Forgiveness.

Debt payments reduce your effective retirement income and can prevent early retirement. If you’re planning to retire before age 65, calculate whether your reduced TRS pension (if applicable) plus other income sources can cover debt payments plus living expenses.

Generally no. Early withdrawals from retirement accounts trigger taxes and penalties that often exceed the benefits of debt elimination. Focus on budgeting and increasing income to pay off debt while preserving retirement savings.

Use the TRS calculator to estimate your pension and identify potential income gaps.