How to Build a Guaranteed Income Floor as a Teacher

Stable income is the foundation of retirement security. Learn how to build it.

Teacher Retirement Withdrawal Strategy: How to Make Your Money Last Choosing the right teacher retirement withdrawal strategy can mean the difference between financial security and running out of money in your golden years. As a teacher who has dedicated decades to educating others, you deserve a retirement plan that supports your needs without causing sleepless […]

Choosing the right teacher retirement withdrawal strategy can mean the difference between financial security and running out of money in your golden years. As a teacher who has dedicated decades to educating others, you deserve a retirement plan that supports your needs without causing sleepless nights about your financial future.

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

The challenge many teachers face is navigating multiple income sources – your Teacher Retirement System (TRS) pension, 403(b) accounts, IRAs, and Social Security. Each has different rules, tax implications, and optimal timing for withdrawals. Getting this coordination wrong could cost you thousands in unnecessary taxes or, worse, leave you short on funds when you need them most.

Most teachers have multiple retirement income streams, each with unique characteristics that affect your withdrawal strategy. Understanding these sources helps you make informed decisions about when and how much to withdraw from each account.

Use the TRS calculator to estimate your pension and identify potential income gaps.

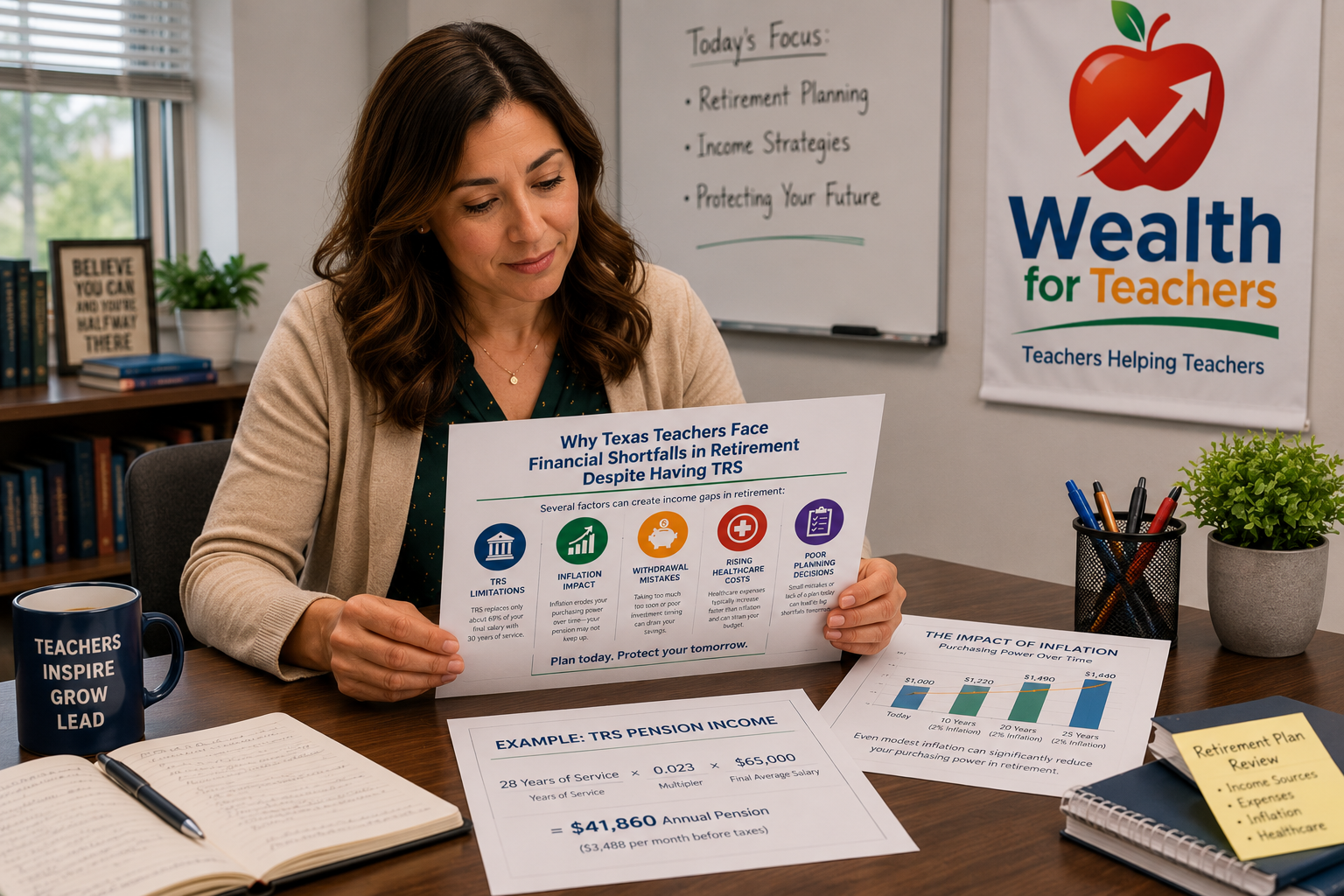

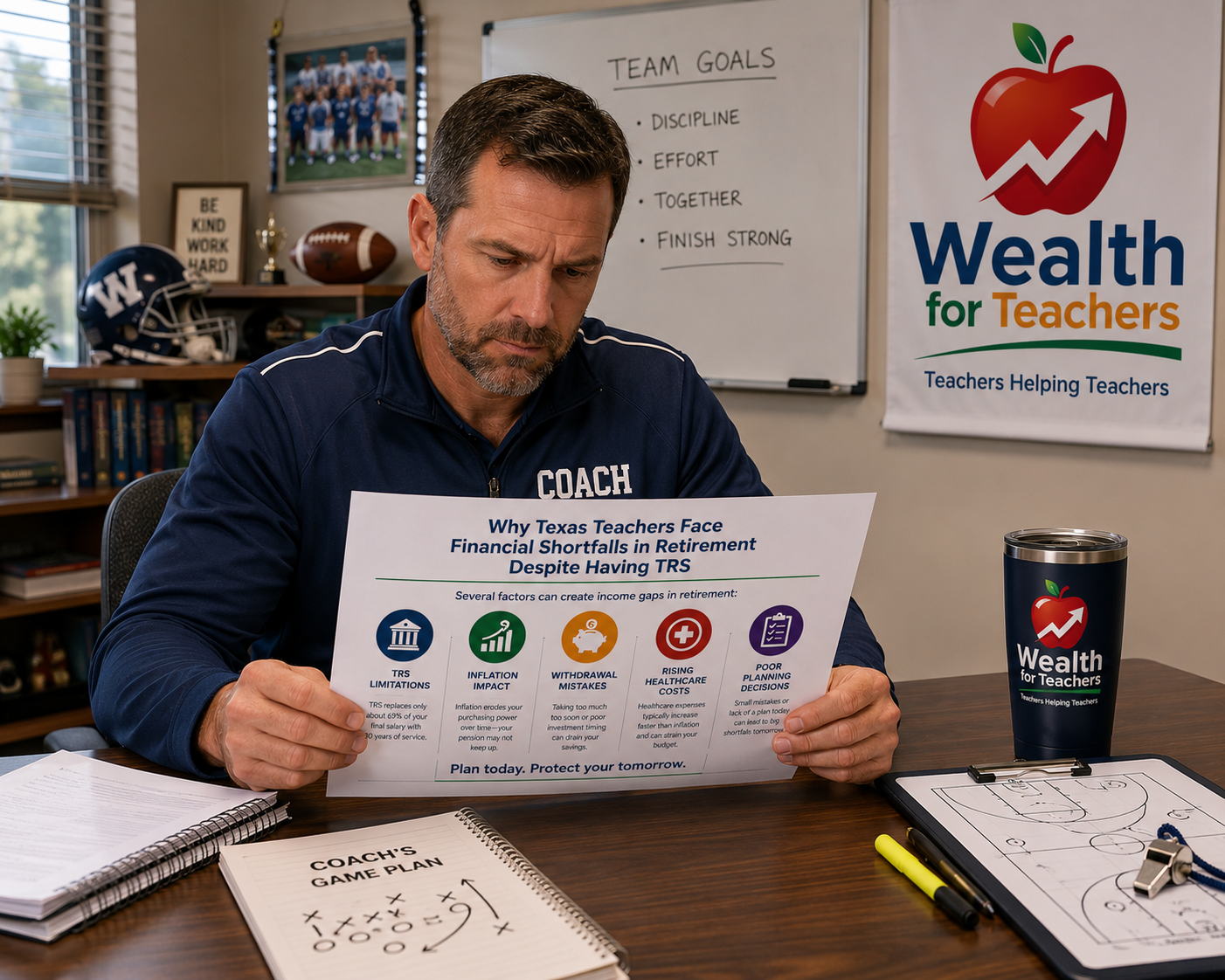

Your Teacher Retirement System pension forms the foundation of most teachers’ retirement income. In Texas, TRS calculates your pension using a straightforward formula with a flat 2.3% multiplier per year of service.

Texas TRS Pension Formula:

Annual Pension = (Years of Service × 0.023) × Final Average Salary

For example, a teacher with 25 years of service and a final average salary of $65,000 would receive:

This pension provides predictable, inflation-adjusted income for life, making it a crucial anchor in your withdrawal strategy. You should also read TRS Retirement Eligibility Explained (age and service years).

Your 403(b), 457(b), and IRA accounts represent the variable portion of your retirement income. Unlike your pension, you control the withdrawal timing and amounts from these accounts, giving you flexibility to manage taxes and cash flow needs.

These accounts typically fall into two categories:

Most teachers earn Social Security credits alongside their TRS service. Your Social Security benefit provides another layer of guaranteed income, though the timing of when you claim can significantly impact your monthly payments.

The traditional 4% withdrawal rule suggests retirees can safely withdraw 4% of their portfolio value annually, adjusted for inflation. However, teachers with pension income may need to modify this approach.

Teachers often have a more favorable retirement situation than the typical retiree because:

With pension income covering basic living expenses, teachers might safely withdraw 4.5% to 5% from their investment accounts. However, this depends on:

The key is ensuring your total income from all sources meets your retirement needs without depleting your savings too quickly.

The order in which you withdraw money from different accounts can save thousands in taxes over your retirement. This strategy, called tax-efficient withdrawal sequencing, requires careful planning.

Most financial experts recommend this sequence:

Teachers may need to adjust this sequence based on:

Smart withdrawal sequencing involves “filling up” lower tax brackets each year. If your pension income places you in the 12% tax bracket, you might withdraw additional funds from tax-deferred accounts to reach the top of that bracket before moving to tax-free sources.

This strategy prevents large tax-deferred balances from pushing you into higher brackets later when required minimum distributions begin. You should also understand How Taxes Impact Teacher Retirement Income.

The timing of when you claim your pension and Social Security benefits significantly impacts your overall withdrawal strategy. These decisions create ripple effects throughout your financial plan.

Most state teacher retirement systems offer several pension claiming options:

Your choice affects how much you need to withdraw from other accounts during early retirement years.

Social Security benefits can begin as early as age 62, but claiming early results in permanent reductions. Delaying benefits past full retirement age earns delayed retirement credits worth 8% per year until age 70.

Teachers with strong pension benefits might delay Social Security to maximize those payments, using 403(b) withdrawals to bridge the gap.

The optimal approach often involves:

Once you reach age 73, the IRS requires minimum distributions from tax-deferred retirement accounts. These Required Minimum Distributions (RMDs) can disrupt your carefully planned withdrawal strategy if not properly managed.

RMDs apply to:

RMDs do not apply to:

Large tax-deferred account balances can force unwanted taxable distributions in later retirement years. Strategies to manage this include:

Teachers who continue working past age 73 can delay RMDs from their current employer’s 403(b) plan. This exception doesn’t apply to IRA accounts or previous employers’ plans, creating planning opportunities for teachers in second careers.

Even well-intentioned teachers can make costly withdrawal mistakes that reduce their retirement security. Understanding these common pitfalls helps you avoid expensive errors. You should read The Biggest TRS Retirement Mistakes that Teachers make over 50.

Many teachers raid their 403(b) accounts before retirement, paying both income taxes and 10% early withdrawal penalties. This double taxation can cost 30-40% of the withdrawal amount.

Better alternatives include:

Teachers who contribute only to traditional tax-deferred accounts miss opportunities for tax diversification. Having all retirement savings in tax-deferred accounts limits flexibility and can push retirees into higher tax brackets.

Successful teachers build balances in:

Some teachers plan their 403(b) withdrawals without considering their pension income. This can result in:

Teachers who lose employer health insurance in early retirement often underestimate healthcare costs. Withdrawal strategies should account for:

Creating an effective teacher retirement withdrawal strategy requires a systematic approach that coordinates all your income sources while minimizing taxes and maximizing longevity of your savings.

Begin by mapping out all your retirement income sources and their timing:

This analysis reveals gaps where 403(b) or IRA withdrawals need to fill income shortfalls.

Create a detailed plan showing which accounts to tap each year from retirement until age 90 or beyond. This plan should:

Your withdrawal strategy should include regular review points to adjust for:

The complexity of coordinating multiple income sources, managing taxes, and ensuring your money lasts often warrants professional help. A financial advisor experienced with teacher retirement benefits can help optimize your strategy and avoid costly mistakes.

Look for advisors who understand:

Generally, you can withdraw from your 403(b) without the 10% early withdrawal penalty starting at age 59½. However, if you retire during or after the year you turn 55, you may be able to withdraw from your current employer’s 403(b) penalty-free under the “age 55 rule.” You’ll still owe income taxes on traditional 403(b) withdrawals regardless of your age.

Texas TRS does not offer a lump sum option – benefits are paid as monthly annuities. This actually works in your favor, as the guaranteed monthly income provides a stable foundation for your retirement. You can then coordinate your 403(b) and IRA withdrawals around this predictable pension income.

Start with your annual retirement expenses, then subtract your guaranteed income (TRS pension and Social Security). The remaining amount is what you’ll need to withdraw from retirement accounts. For example, if you need $60,000 annually and receive $35,000 from pension and Social Security, you’ll need $25,000 from your 403(b) or IRA accounts.

Since your TRS pension provides stable income, you may benefit from delaying Social Security to earn delayed retirement credits worth 8% per year until age 70. This strategy works well if you can use 403(b) withdrawals to bridge the gap. However, your health, spousal benefits, and overall financial situation should factor into this decision.

Yes, Roth conversions can be an excellent strategy for retired teachers. Convert traditional IRA or 403(b) funds to Roth accounts during years when your income is lower (such as before claiming Social Security or during market downturns). This reduces future required minimum distributions and provides tax-free income later in retirement.

With a guaranteed TRS pension, you may need less in emergency funds than typical retirees. Consider keeping 6-12 months of expenses beyond your pension income in cash or conservative investments. For example, if your pension covers $3,000 monthly and you need $4,500 total, keep emergency funds to cover 6-12 months of the $1,500 difference.

Long-term care costs can dramatically increase your withdrawal needs. Consider purchasing long-term care insurance while healthy, or build additional reserves in your plan. Your TRS pension continues during care needs, but you may need to accelerate withdrawals from other accounts or consider Roth conversions before care is needed to minimize taxes on larger withdrawals.

This depends on your mortgage interest rate, tax bracket, and cash flow needs. Many teachers benefit from paying off mortgages before retirement to reduce fixed expenses, even if it means slightly higher taxes due to loss of mortgage interest deductions. Lower fixed costs give you more flexibility in your withdrawal strategy and reduce the pressure on your retirement accounts.

Use the TRS calculator to estimate your pension and identify potential income gaps.