How to Build a Guaranteed Income Floor as a Teacher

Stable income is the foundation of retirement security. Learn how to build it.

Learn how to stress-test your teacher retirement plan to ensure your TRS pension and savings can handle inflation, market risk, and longevity.

Texas teachers often assume their TRS pension will provide stability in retirement. But what happens when inflation outpaces your cost-of-living adjustments? What if medical expenses skyrocket beyond Medicare’s coverage? What if your spouse needs long-term care?

Texas teachers can also run a full pension estimate using the Texas Teacher Retirement Calculator to better understand their retirement outlook.

A teacher retirement stress test reveals whether your pension, savings, and income plan can handle real-world retirement challenges. Without testing these scenarios, you may discover critical gaps only after it’s too late to fix them.

This comprehensive approach to Texas Teacher Retirement Planning Guide helps you identify vulnerabilities before you retire, giving you time to make necessary adjustments.

Most retirement plans fail because they are never tested under real-world conditions. Teachers assume their TRS pension provides complete security, but pension benefits alone rarely cover all retirement expenses. A proper stress test examines how your entire retirement income strategy performs under pressure.

A teacher retirement stress test examines whether your retirement income can withstand unexpected financial pressures. Unlike basic retirement calculators that assume steady returns and predictable expenses, stress testing considers worst-case scenarios.

Use the TRS calculator to estimate your pension and identify potential income gaps.

For Texas teachers, this means testing how your TRS pension performs alongside your personal savings when faced with:

The goal is to identify weaknesses in your retirement plan while you still have time to address them.

Texas TRS provides valuable retirement benefits, but the system has specific vulnerabilities that stress testing reveals.

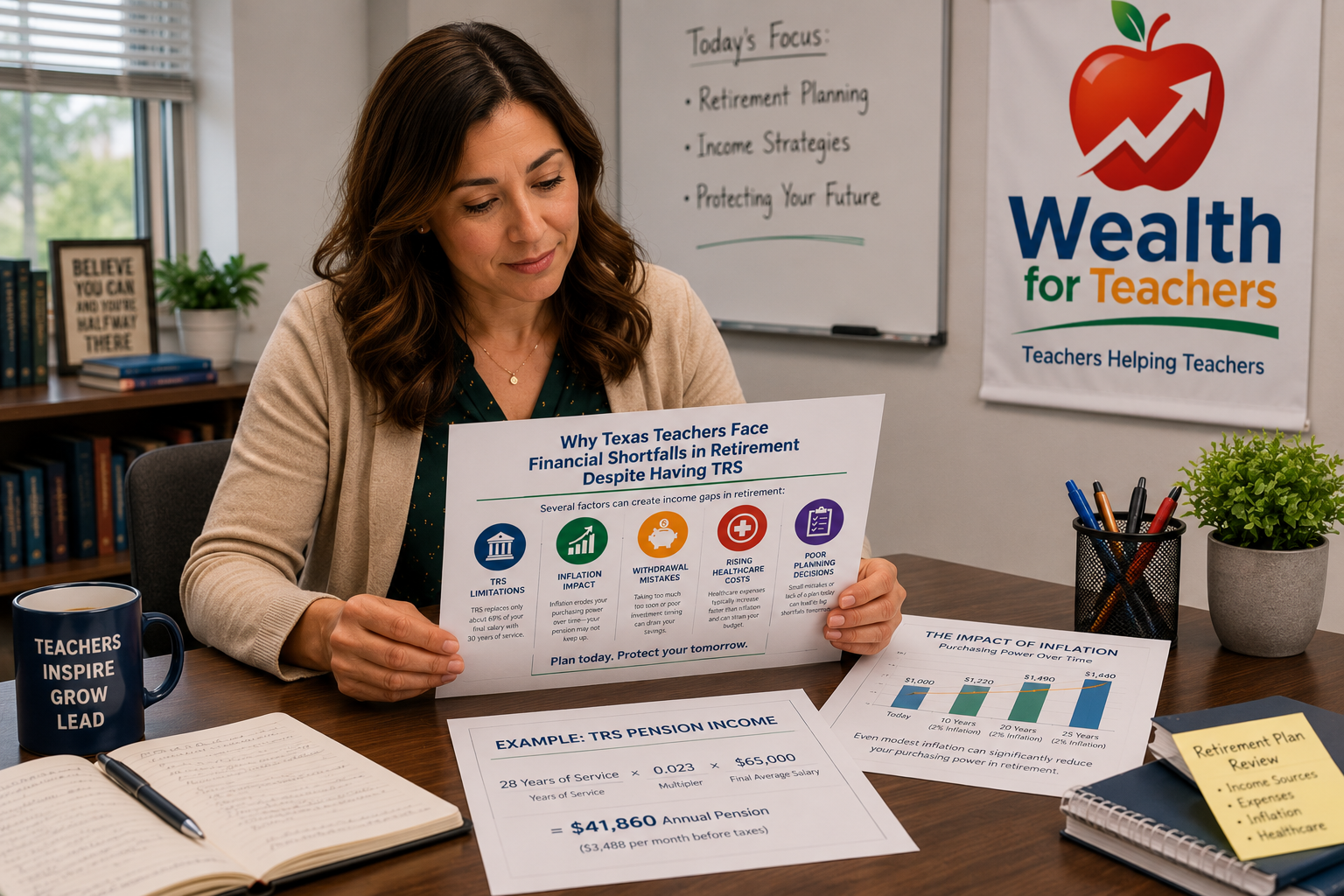

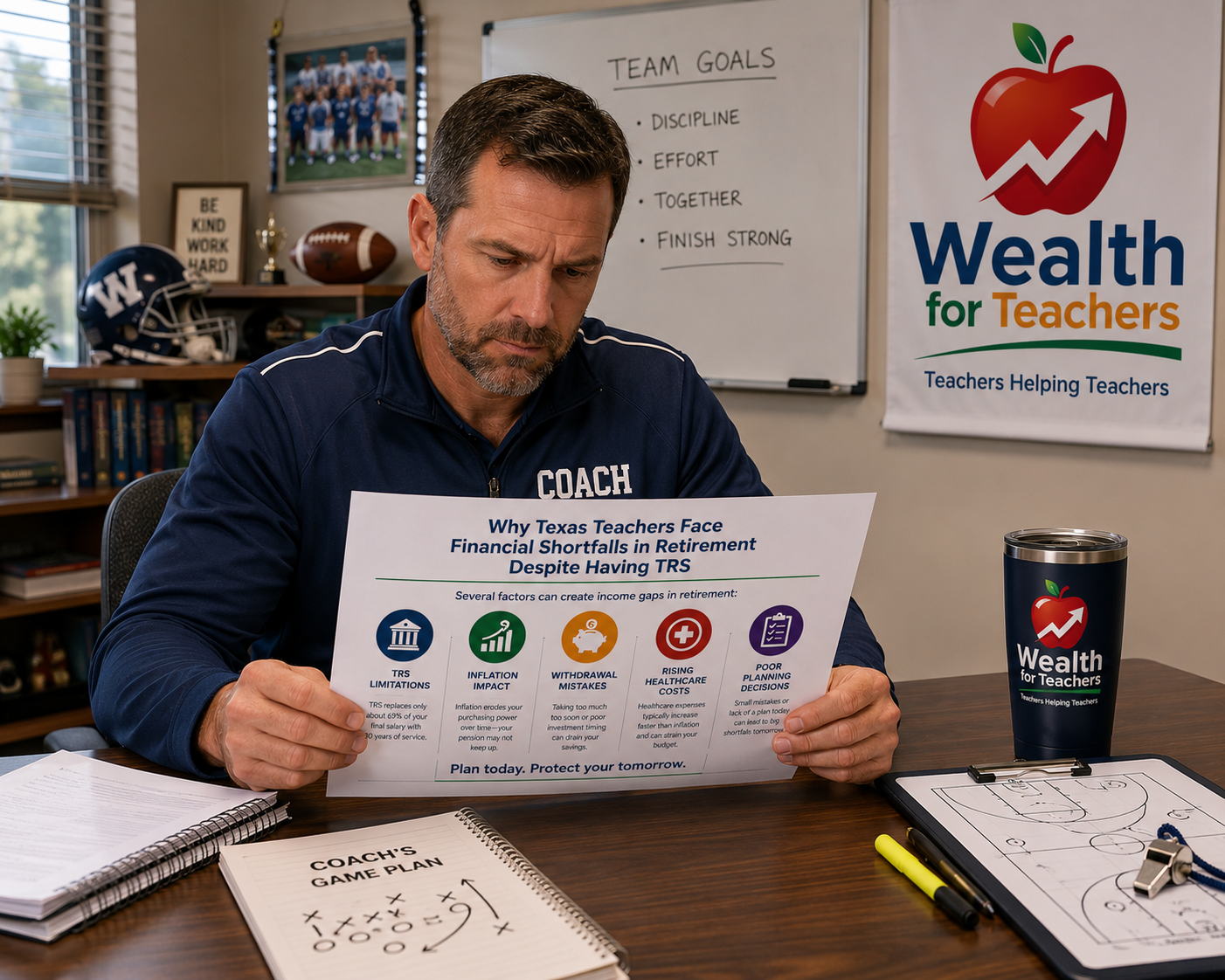

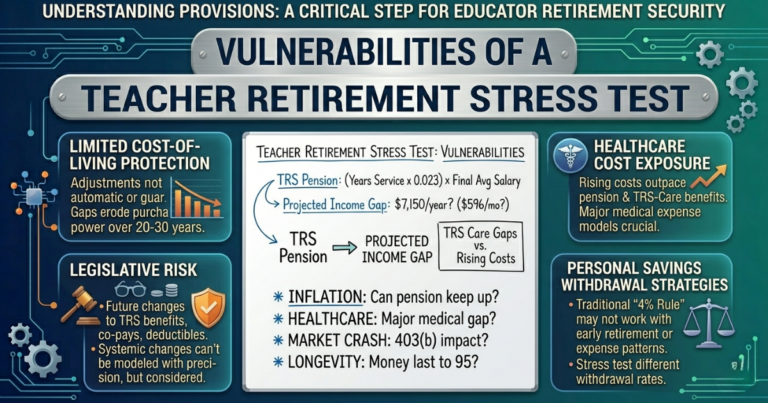

TRS cost-of-living adjustments are not automatic or guaranteed. When the legislature approves increases, they often fail to keep pace with actual inflation. Over a 20-year retirement, this gap can significantly erode your purchasing power.

For example, a teacher retiring with a $4,000 monthly TRS pension might see their real purchasing power drop to $2,400 after 20 years of 3% annual inflation without corresponding pension adjustments.

Future legislatures could modify TRS benefits, particularly for new retirees. While existing benefits have legal protections, stress testing considers how potential changes might affect your overall retirement security.

TRS-Care provides retiree health benefits, but coverage gaps exist. Stress testing examines how rising healthcare costs might outpace both your pension and TRS-Care benefits.

Start your stress test by calculating your projected retirement income gap.

Use the TRS formula: Annual Pension = (Years of Service × 0.023) × Final Average Salary

A teacher with 30 years of service and a $65,000 final average salary would receive:

(30 × 0.023) × $65,000 = $44,850 annually, or $3,738 monthly

Most financial planners suggest retirees need 70-80% of their pre-retirement income. However, teachers often need more due to healthcare costs and the desire to maintain their lifestyle.

If your final salary was $65,000, you might need $52,000 annually in retirement income.

In this example, the gap would be $52,000 – $44,850 = $7,150 annually, or about $596 monthly.

This gap must be filled by Social Security, personal savings, or other income sources. What a Teacher’s Retirement Income Plan Should Include provides detailed guidance on filling these gaps.

Test how your retirement income performs under different inflation scenarios:

Calculate how each scenario affects your purchasing power over 20-30 years of retirement. Factor in whether your TRS pension, Social Security, and other income sources adjust for inflation.

Test whether your money lasts if you live longer than expected. Many teachers retire in their early 60s and could face 30+ years of retirement.

Run scenarios for living to age 85, 90, and 95. Consider how healthcare costs typically increase with age and whether your savings can handle these expenses.

Model a major healthcare expense, such as long-term care. With nursing home costs averaging $60,000-$80,000 annually in Texas, a five-year stay could devastate retirement savings.

Test whether your retirement plan can absorb these costs while maintaining income for your surviving spouse.

If you have significant 403(b) or IRA balances, test how a major market decline early in retirement affects your overall financial security.

Model a 30-40% decline in your investment accounts and calculate how this impacts your withdrawal strategy and overall retirement income.

Many Texas teachers face Social Security reductions due to the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO). The WEP and GPO Explained for Texas Teachers details these reductions.

Your stress test must account for these reductions when calculating total retirement income.

Test different withdrawal rates from your personal savings. The traditional 4% rule may not work for teachers who retire early or face unique expense patterns.

How Much Can a Retired Teacher Safely Spend Each Year? provides specific guidance on sustainable withdrawal rates for teachers.

Many retired teachers work part-time. Test how this income fits into your overall plan, considering:

After identifying vulnerabilities through stress testing, take specific action to strengthen your retirement plan.

If your stress test reveals income gaps, increase your 403(b) contributions or explore additional savings vehicles. Even small increases can significantly impact your retirement security over time.

Working additional years provides triple benefits: more years of TRS service credit, additional years to save, and fewer years of retirement to fund.

Consider long-term care insurance or develop a specific strategy for healthcare expenses that exceed TRS-Care coverage.

Develop retirement income sources beyond your TRS pension. This might include rental property, part-time consulting, or systematic investment withdrawals.

Understand how taxes will impact your retirement income. How Taxes Impact Teacher Retirement Income explains tax-efficient withdrawal strategies for teachers.

When this applies: Teachers with 30+ years of service but minimal 403(b) savings

Use the TRS calculator to estimate your pension and identify potential income gaps.